{kind=link}

As part of a another current project, which I will have more to say about…

The consolidated government – treasury and central bank

In yesterday’s blog – If only the citizens knew what was going on! – I noted that it makes very little sense from a flow of funds perspective to consider the central bank not to be part of a consolidated government sector along with the treasury. The notion of a consolidated government sector is a basic Modern Monetary Theory starting point and allows us to demonstrate the essential relationship between the government and non-government sectors whereby net financial assets enter and exit the economy without complicating the analysis unduly. This simplicity leads to many insights all of which remain valid as operational options when we add more detail to the model. However, it still seems that readers are confused by this and somehow think that the consolidation is misleading. So for today’s blog I aim to explain in more detail what this consolidation is about. It should disabuse you of the notion that the mainstream macroeconomics obsession with central bank independence is nothing more than an ideological attack on the capacity of government to produce full employment which also undermines our democratic rights.

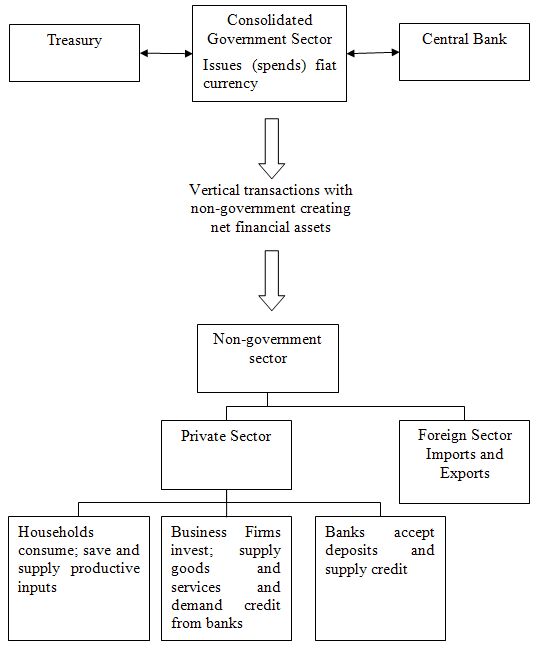

Regular readers will have seen this diagram which appeared along with discussion in the blog – Deficits 101 Part 3 – but was originally presented in my book Full Employment Abandoned: Shifting sands and policy failures which was published in 2008.

You should also read the blog – Deficits 101 Part 1 – to refresh your memory of the vertical relationship between the government and non-government sectors whereby net financial assets enter and exit the economy.

The diagram sought to elaborate on the vertical transactions between the government and non-government sectors and to explain the importance of them for understanding how the economy works? It was intended as a vehicle to help people connect the pieces of the monetary system in an orderly fashion and to re-educate those who have been poisoned by mainstream macroeconomics textbooks.

You will see that this diagram adds more detail to the diagram presented in Deficits 101 Part 1 – which showed the essential relationship between the government and non-government sectors arranged in a vertical fashion.

Focusing on the vertical train first, you will see that the tax liability lies at the bottom of the vertical, exogenous, component of the currency. The consolidated government sector (the treasury and central bank) is at the top of the vertical chain because it is the sole issuer of currency and the transactions that the treasury and the central bank make with the non-government are able to alter the net system balance (which I will explain presently).

The middle section of the graph is occupied by the private (non-government) sector. It exchanges goods and services for the currency units of the state, pays taxes, and accumulates the residual (which is in an accounting sense the federal deficit spending) in the form of cash in circulation, reserves (bank balances held by the commercial banks at the central bank) or government (Treasury) bonds or securities (deposits; offered by the central bank).

The currency units used for the payment of taxes are consumed (destroyed) in the process of payment. Given the national government can issue paper currency units or accounting information at the central bank at will, tax payments do not provide the state with any additional capacity (reflux) to spend.

The reason we take a consolidated approach to government in the first instance is because the two arms of government (treasury and central bank) have an impact on the stock of accumulated financial assets in the non-government sector and the composition of the assets.

The government deficit (treasury operation) determines the cumulative stock of financial assets in the private sector. Central bank decisions then determine the composition of this stock in terms of notes and coins (cash), bank reserves (clearing balances) and government bonds with one exception (foreign exchange transactions).

The diagram also shows how the cumulative stock is held in what we term the non-government Tin Shed which stores fiat currency stocks, bank reserves and government bonds.

I invented this Tin Shed analogy to disabuse the Australian public of the notion that somewhere down in Canberra (our national capital) there was a storage area where the national government was putting all those surpluses away for later use. This is a constant misperception that pervades the policy debate. Even the mainstream macroeconomics textbooks call budget surpluses “national saving”.

The reality is that there is no storage because when a surplus is run, the purchasing power embodied in the net outflow of financial assets from the non-government sector to the government sector is destroyed forever. However, the non-government sector certainly does have a Tin Shed within the banking system and elsewhere.

Any payment flows from the government sector to the non-government sector that do not finance the taxation liabilities remain in the non-government sector as cash, reserves or bonds. So we can understand any storage of financial assets in the Tin Shed as being the reflection of the cumulative budget deficits.

Taxes are at the bottom of the exogenous vertical chain and go to rubbish, which emphasises that they do not finance anything. While taxes reduce balances in private sector bank accounts, the government doesn’t actually get anything – the reductions are accounted for but go nowhere.

Thus the concept of a fiat-issuing Government saving in its own currency has no meaning. Governments may use its net spending to purchase stored assets (spending the surpluses for instance on gold or in sovereign funds) but that is not the same as saying when governments run surpluses (taxes in excess of spending) the funds are stored and can be spent in the future. This concept is erroneous. Please read my blog – The Futures Fund scandal – for more discussion on this point.

Finally, payments for bond sales are also accounted for as a drain on liquidity but then also scrapped.

What are the implications of all this?

You will have heard of the term the monetary base which appears in most macroecoomics text-books as the precursor to outlining the erroneous concept of the money multiplier. Please read my blogs – Money multiplier and other myths and Money multiplier – missing feared dead – for more discussion about why there is no money multiplier.

The concept of the monetary base is a very narrow concept of what economists misleadingly call money. We will use the term net financial assets because it is less problematic.

The monetary base is comprised of:

- The currency (notes and coins) held by the public and issued by the government);

- The deposits that the commercial banks have with the central bank – the so-called reserves;

- The liabilities the central bank has to the non-bank financial intermediaries.

The term “base” is loaded (excuse pun) because it is seen by the mainstream as the base on which banks lend from. Of-course bank lending is not reserve constrained so the term lacks meaning in this context. Please read the following blogs – Building bank reserves will not expand credit and Building bank reserves is not inflationary – for further discussion on this point.

The following table captures the relationship between the monetary aggregates but in no way supports a money multiplier interpretation of the linkages.

![]()

The Table helps to sort the vertical transactions (1 to 4) from the horizontal (6 and 8).

National government budget impacts

In isolation, a national government budget deficit, which results from the government spending more (via crediting bank accounts and/or posting cheques) than it drains via taxation revenue from the non-government sector, results in an overall injection of net financial assets to the monetary system. This boosts the monetary base.

Conversely a national government budget surplus, which results from the government spending less than it drains via taxation revenue from the non-government sector, results in an overall withdrawal of net financial assets from the monetary system. This reduces the monetary base.

However, if the government also issues debt $-for-$ to match its deficit then the impact on the monetary base is neutralised. Mainstream textbooks think this is a “funding” operation, whereas from a MMT perspective it is a bank reserve operation which allows the central bank to effective conduct its liquidity management tasks.

Please read my blog – Understanding central bank operations – for more discussion on this point.

Foreign exchange transactions

The external position of a nation impacts on the monetary base if there is official central bank foreign exchange transactions.

A nation’s currency is demanded in foreign exchange markets to facilitate the purchase of its exports by foreigners; to pay interest, profits and dividends to residents who have foreign investments; and to faciliate foreign direct investment in local companies.

Conversely, a nation’s currency is supplied to foreign exchange markets to facilitate the purchase of imports from other countries; to pay interest, profits and dividends to foreign investors; and to faciliate lending to foreign companies.

Ordinarily, where there is a balance of payments deficit the demand for a nation’s currency in foreign exchange markets will be less than the supply of that currency and there will be downward pressure on the exchange parities.

When there is a balance of payments surplus the demand for a nation’s currency in foreign exchange markets will be greater than the supply of that currency and there will be updward pressure on the exchange parities.

So exchange rate movements can arise from the real sector and the financial sectors with the latter increasingly dominating in the era of financialisation. That situation is one thing that needs to be changed if we are to restore stable growth with full employment but that is the topic of another blog.

A floating exchange rate system allows these supply and demand imbalances in currencies to resolve themselves via exchange rate movements with no impact on the monetary base.

However, under a fixed exchange rate system, a country with an external deficit (supply of currency greater than demand) would face downward pressure on its parity and the central bank was committed to easing that quantity imbalance by conducting official foreign exchange transactions. So in this case it would buy its own currency in the foreign exchange markets by selling foreign currencies until the demand and supply of the local currency was equal and consistent with the fixed exchange rate being targetted.

These transactions would drain the local currency from the economy (the foreign exchange market is considered part of the monetary system) and so the monetary base would shrink.

If the nation had an external surplus (supply of currency less than demand) it would face upward pressure on its parity and the central bank had to sell its own currency in the foreign exchange markets by buying foreign currencies until the demand and supply of the local currency was equal and consistent with the fixed exchange rate being targetted.

These transactions would inject the local currency from the economy (the foreign exchange market is considered part of the monetary system) and so the monetary base would increase.

In a pure floating regime with no official central bank intervention, there is no change in the volume of a nation’s currency as a result of the foreign exchange transactions. As an example, assume an exporting firm in Australia earns $USDs and seeks to convert them into $AUDs. It will sell them to a foreign exchange dealer who brokers a deal with a counterparty who desires to hold $USDs and already has $AUDs (perhaps an importing firm).

The exporting firm’s holdings of $AUDs rises as the counterparty’s holds fall. There is no change in the volume of AUDs on issue.

Clearly, things are different in a pure fixed exchange rate system as noted above. A floating exchange rate system thus does no hamper monetary or fiscal policy in the same way that monetary policy is forced to defend the parity in a fixed exchange rate system.

In reality, the central bank still conducts official foreign exchange transactions even if the currency mostly floats. So when the currency is weak (and the central bank fears an inflationary spike coming via increased import prices), it may intervene and buy foreign currency and vice versa when the currency is strong (and there is a fear that the competitiveness of the trading sector is compromised).

The following graphs show the scale of that intervention in Australia since 1973. The data is available from the Reserve Bank of Australia. The left-panel shows the total official FX transactions in $A millions (which include gold and foreign exchange less net overseas borrowing of the national government), the middle panel shows the change in reserve assets due to valuation in $A millions, while the right-panel shows the total change in reserve assets.

You can see the scale of the transactions has increased over time and there are huge swings in short periods of time.

I plan to write some more about the capacity of foreign exchange markets to wreak havoc on a nation, a point that some commentators seem to have become stuck on recently. I would note that Australia is an extremely open economy with litle industrial base. Our export sector is largely based on primary commodities and agriculture.

We have huge swings in our exchange rate. For example in September 2001, the $AUD was selling for 0.4923 $USD and all my US mates were laughing about how we were now the half-price country. By March 2007, it was back over 80 cents. In 1987, we lost about 10 per cent of our nominal GDP in valuation effects due to currency depreciation and terms of trade swings in two quarters! These are huge swings. Our standard of living was barely impacted.

![]()

Government bond sales

The impact of national budget outcomes and central bank official intervention on the monetary base can be offset by government bond sales/purchases. Why would the government desire this offset?

The fundamental principles that arise in a fiat monetary system are as follows.

- The central bank sets the short-term interest rate based on its policy aspirations.

- Government spending is independent of borrowing which the latter best thought of as coming after spending.

- Government spending provides the net financial assets (bank reserves) which ultimately represent the funds used by the non-government agents to purchase the debt.

- Budget deficits (and official foreign intervention which adds to the monetary base) put downward pressure on interest rates contrary to the myths that appear in macroeconomic textbooks about ‘crowding out’.

- The “penalty for not borrowing” is that the interest rate will fall to the bottom of the “corridor” prevailing in the country which may be zero if the central bank does not offer a return on reserves.

- Government debt-issuance is thus a “monetary policy” operation rather than being intrinsic to fiscal policy, although in a modern monetary paradigm the distinctions between monetary and fiscal policy as traditionally defined are moot.

To understand these points we need to understand the concept of a system balance which relates to the daily liquidity in the banking system. The system balance is another term for the monetary base. It is important to understand it because it impacts on the ability of the central bank to maintain its desired monetary policy stance – which involves setting a particular overnight interest rate.

Every day, official transactions are occurring (Items 1 to 3 in the Table above) and they impact on the system balance or the money market cash position.

Governmments spend and tax continuously and the central bank regularly conducts official foreign exchange transactions. Further public debt matures regularly and the central bank may conduct repos and rediscount treasury notes before their maturity date is reached.

When the flow of funds that accompany the vertical transactions is in favour of the government sector, we say the system balance is in deficit (or the system is “undersquare”) and vice versa (surplus or oversquare).

You can thus appreciate the particular transactions and balances that will deliver a system surplus or a system deficit.

A budget deficit, for example, will result in a system surplus or oversquare position. There will be excess reserves in the accounts held by the banks with the central bank.

If there is no support rate paid by the central bank on these excess reserves then the commercial banks will try to lend then on the interbank market. The possible borrowers will be other banks who lack reserves at the end of the day. But these horizontal transactions are incapable of clearing the overall system overall. All they do is shuffle which banks are carrying the excess.

In trying to chase a return on the excess reserves, the competition in the interbank market drives the overnight rate down to whatever support rate is in place (which might be zero). Effectively, if there was no central bank reaction, the official policy rate being maintained by the central bank would become irrelevant as the interbank rate fell.

The central bank can drain the excess reserves simply by selling government debt. Accordingly, debt is issued as an interest-maintenance strategy by the central bank. It has no correspondence with any need to fund government spending.

The analysis should be easily understood in the case of the impacts of budget surpluses and the impact of official foreign exchange transactions that add reserves and those that drain reserves.

Further, the idea that governments would simply get the central bank to “monetise” treasury debt (which is seen orthodox economists as the alternative “financing” method for government spending) is highly misleading. Debt monetisation is usually referred to as a process whereby the central bank buys government bonds directly from the treasury.

In other words, the federal government borrows money from the central bank rather than the public. Debt monetisation is the process usually implied when a government is said to be printing money. Debt monetisation, all else equal, is said to increase the money supply and can lead to severe inflation.

However, as long as the central bank has a mandate to maintain a target short-term interest rate and does not pay a support rate on excess reserves, the size of its purchases and sales of government debt are not discretionary. Once the central bank sets a short-term interest rate target, its portfolio of government securities changes only because of the transactions that are required to support the target interest rate.

The central bank’s lack of control over the quantity of reserves underscores the impossibility of debt monetisation. The central bank is unable to monetise the federal debt by purchasing government securities at will because to do so would cause the short-term target rate to fall to zero or to the support rate. If the central bank purchased securities directly from the treasury and the treasury then spent the money, its expenditures would be excess reserves in the banking system. The central bank would be forced to sell an equal amount of securities to support the target interest rate.

The central bank would act only as an intermediary. The central bank would be buying securities from the treasury and selling them to the public. No monetisation would occur.

However, the central bank may agree to pay the short-term interest rate to banks who hold excess overnight reserves. This would eliminate the need by the commercial banks to access the interbank market to get rid of any excess reserves and would allow the central bank to maintain its target interest rate without issuing debt.

From a MMT perspective it is far preferable to eliminate the debt-issuance machinery altogether and pay a support rate on reserves if the central bank wants to target a non-zero short-term interest rate. But even more preferable is to allow the short-term interest rate to drop to zero by not issuing public debt or paying a support rate on excess reserves. Then the interbank market will compete the rate down to zero each day and fiscal policy would become the principle counter-stabilisation tool and the most effective means of disciplining price pressures in specific asset classes.

Please read the following blogs – Operational design arising from modern monetary theory – Asset bubbles and the conduct of banks and The natural rate of interest is zero! for further discussion of the preferred MMT position.

Conclusion

The vertical transactions which add to or drain the monetary base that I have outlined here are transactions between the government and the non-government sector. I note some people think the distinction between government and non-government is confusing but you should see it as an essential starting point to understanding the nature of the vertical transactions.

These transactions are thus unique – they change net financial assets in the economy.

All the transactions between private sector entities have no effect on the net financial assets in the economy at any point in time.

Anyway, we have now explicitly considered the impact of official foreign exchange transactions (which might include gold sales and purchases as well as straightforward currency deals).

Australian Federal Election

Tomorrow is our national election.

We are forced to vote here. Some democracy. The choices between the major parties are either bad or very bad. The Greens who are the third main party have no understanding of macroeconomics. Some democracy.

The Government may change tomorrow given the polls and Julia Gillard our first female prime minister will then have the record of the shortest prime minister in history. The Government should have kept the stimulus going and taken some hard decisions on climate change and stopped locking refugees up in prisons (including their children). They did not take any major progressive decisions in their term of office and were beguiled by their neo-liberal pretensions.

They deserve to be tossed out. But that is not to say that the conservatives deserve to be voted in. They are a disgrace and will seek to implement pernicious policies on the disadvantaged just like they did when they were in power last time (1996-2007). They deny climate change and want to make it even harder for refugees. They never deserve to be in government of a progressive forward-thinking nation.

The only policy that is separating them is on the construction of the national broadband network. The Government is promising to continue building a technology that will serve us well into the future whereas the conservatives want to keep us back in the past. All discussions about “costs” in that regard are irrelevant because the only costs that matter are the real resources being used and the Government’s plan is probably not much more “costly” than the status quo.

Most importantly, both major parties want to run surpluses without knowing what that means. They do not understand that at this stage of the business cycle even larger deficits are required. They will both run a macroeconomic strategy that will be detrimental to the unemployed and their families and then they will both turn on these same people and introduce punishing welfare-to-work changes that will just make the lives of the miserable even worse.

There is not much choice down here! I am not allowed under existing electoral law to encourage voters that instead of voting they should write essays on their ballot papers outlining why all major parties have lost the plot.

Saturday Quiz

The Saturday Quiz will be back sometime tomorrow. It national election day in Australia so I might have some questions relevant to that event! Our democracy is in a sad state.

That is enough for today!

I could agree with being forced to vote, but only if there is a ‘none of the above’ option (or RON – reopen nominations, leading to the ‘vote for RON’ campaign slogan).

good post as always. a month or so ago i was at a talk steve keen gave here in nyc. i pushed him on his position of chartalism. while he said that he hadn’t gotten around to doing a formal critique, he thinks a fiscal policy like the one we suggest would lead to a “currency collapse”. i was wondering if you would respond to this critique and provide an alternative analysis of what determines the balance of trade

“taken some hard decisions on climate change”

Though to be fair, the conservatives blocked their policy proposal twice in a row in the senate, leaving taking the country to a double dissolution the only possible way to pass any such policy. I seem to recall that the last time government called such a move was in 1974 and it ended very badly for them.

While making such a move would have shown true courage of conviction and leadership, I suspect they felt it too risky – we Australians are a pretty apathetic bunch and the indignation of being forced to get off our arses and go to the polls early over a single issue could easily have seen a lethal protest backlash. After more than a decade in the political wilderness they did not want to risk losing in the middle of their first term.

Did I mention I saw a coalition flyer the other day emphasising the governments failure to take action on climate change – while conveniently forgetting to mention that it was them who blocked it in the senate!

Dear Bill,

I am sorry but I have to disagree with the statement that urging to vote informally is an offence in Australia. There had been initial media comments suggesting that triggered by Mark Latham’s remarks but the issue was then settled by the AEC itself.

This is what is banned:

“A person shall not, during the relevant period in relation to an election under this Act, print, publish or distribute, or cause, permit or authorize to be printed, published or distributed, any matter or thing that is likely to mislead or deceive an elector in relation to the casting of a vote.”

REFERENCE_http://www.austlii.edu.au/au/legis/cth/consol_act/cea1918233/s329.html

The following ABC article explains the controversy:

“The Australian Electoral Commission (AEC) says there is no law which prohibits the public from voicing an opinion on how people should vote, including casting an informal vote.”

REFERENCE_http://www.abc.net.au/news/stories/2010/08/16/2983675.htm

I agree that all the 3 major parties either lie about or do not (fully) understand the economic issues. But in my opinion there is a difference between abstaining and allowing for the Coalition supporters to elect the “3 illegal boats per year” Tony Abbott or voting for the Greens and leaking the preferences to the ALP, possibly leading to a coalition government which could make first baby steps to address the climate change issue.

This is not that I am endorsing the ALP or if that really matters, the Greens. But knowing how the system works in Australia and having the following options: an informal vote, Coalition, ALP, Greens, other minnow parties or the independents I am going to vote for the Greens and then for ALP for both the House of Representatives and the Senate as I do have children and I don’t want them to see the effects of our global ignorance and negligence in regards to the environment.

This is what really matters to me not saving the United States of America from themselves.

Speaking of baby steps, here is footage of Tony “great big debt” Abbot being presented with Sean Carmody’s chart highlighting the difference between government debt and household debt in Australia. It isn’t an explanation of MMT but does reinforce how silly all the debt and deficit hysteria are, while making Abbot look like a prize goose at the same time.

And this is a pretty popular show – perhaps enough people saw it to tone down their fears of “great big debt and deficit”.

I for one, enjoyed watching Abbot squirm.

http://petermartin.blogspot.com/2010/08/tonys-debt.html

If the Fed can indeed set AND meet a target interest rate though the purchase/sale of bonds, does that also mean that it can set an inflation rate in the case of unconstrained real goods? Doesn’t the issuance/repurchase of long bonds attempt to control inflation by changing the cash supply for 30 years?

Bill:

“Government spending is independent of borrowing which the latter best thought of as coming after spending.”

According to the existing US law (Federal Reserve Act), for the government(Treasury) there is no mechanism to borrow from the FRB directly. In other words, the USG does not have a Zimbabwe line of credit with the Feds. As a consequence of not having a ZLOC, the USG can finance its deficit only through selling T-paper on the primary market, aka borrowing. The Feds cannot, by the same law, participate in the primary auctions, but rather buy the treasuries on the secondary markets, the prohibition prevents bypassing the absence of ZLOC. So, the correct temporal sequence under the current law is for the government to borrow first and spend second.

Article 123 TEC (Treaty establishing the European Community) explicitly prohibits a Central bank ZLOC:

”

Overdraft facilities or any other type of credit facility with the European Central Bank or with

the central banks of the Member States (hereinafter referred to as ‘national central banks’) in favour of

Union institutions, bodies, offices or agencies, central governments, regional, local or other public

authorities, other bodies governed by public law, or public undertakings of Member States shall be

prohibited, as shall the purchase directly from them by the European Central Bank or national central

banks of debt instruments.

”

The Bank of Canada offers a very limited and controlled line of credit for emergencies only, not for normal operations. I am not sure about details since I’ve been out of of touch with Canadian CB regulations for more than 10 years but I guess one can easily find laws/regulations applicable to BoC operations on-line if one is so motivated.

To re-iterate, US/Canada/EZ Government spending is *dependent* on borrowing with the latter coming *before spending*. Of course, you may have some other ‘Government’ in mind for which the no-overdraft restriction does not apply.

VJK,

Agree with you. However note that for sovereign nations, these rules can be easily broken. Also note that the US Treasury still has seigniorage powers – the Treasury can mint coins of any denomination and has to be acceptable by the Federal Reserve. If this operation needs to be done, the Fed will record the coin as an asset and credit the Treasury General Account. The Treasury can then continue to spend.

Also, the Fed can participate in auctions: “…. as a consequence, at most the Desk’s acquisition at Treasury auctions can equal maturing holdings.” Understanding Open Market Operations, MA Akthar, p37 (Fed paper)

The argument that “spending necessarily comes first” or an equivalent should NOT be interpreted as suggesting that the Tsy doesn’t need to sell bonds under current law.

Spending or an overdraft to a bank’s CB account (loan from the consolidated Tsy/CB) is necessary to provide the RBs to the banking system that then settle tax liabilities or primary bond auctions with the Tsy. This is the case whether or not the Tsy receives an overdraft at the CB. But, this DOES NOT mean that the Tsy itself doesn’t have to sell bonds or otherwise obtain credits to its account at the CB in order to spend if the govt has imposed this constraint on itself (i.e., the govt forbids itself from receiving overdrafts from the CB). Both can be (and currently are) true without any inconsistency–the govt can and currently does require itself to obtain credits from bank reserve accounts that were created via previous spending or CB lending before it spends again.

So what is the MMT terminology “net financial assets”. Reading this post, leads me to believe that the monetary base is “net financial assets”

If that is the case, Canadian banks end up with zero settlement balances every day. So only currency in circulation is NFA ?

If net financial assets is the sum of currency in circulation, settlement balances and government debt, what about assets denominated in foreign currencies but held by citizens/institutions of a nation ?

When a government, or “Federal Government” in the Z.1 – US Flow of Funds language spends by instructing the central bank to transfer funds from its account at the central bank, banks’ clearing balances increase. However not all increases of settlement balances can be thought of as increasing financial assets. (A implies B does not mean B implies A). One example – the US Treasury purchases foreign currency from JP Morgan, it increases JP Morgan’s settlement balances at the Federal Reserve. The Fed just owes less to the Treasury and more to JPM. On the other hand, the increase in settlement balances does not increase the private sector’s net financial assets. (Whatever happens to fluctuations in the exchange rate comes later. Thats a small change.)

VJK,

Also note that government deficits tend to increase demand and national income. Higher saving and wealth created by government deficits lead to chasing government bonds and higher demand for them – causing no “crowding out”

Ramanan:

(1)”However note that for sovereign nations, these rules can be easily broken.”

Since here ‘rules’ = ‘law’, are you saying that the law can easily be broken ? I am sure that’s not what you have in mind, surely !

(2) Coin production is irrelevant. As I wrote elsewhere, “Banks *buy* cash from the Fed by having their reserve accounts debited – there is no money creation here.” The Fed pays the Treasury only the minute cost of coin production , not of course the cash face value.

(3) The full quote is as follows:

”

The Federal Reserve is prohibited by law from adding to its net position by direct purchases of securities from the Treasury-that is, the Federal Reserve

has no authority for direct lending to the Treasury. As a consequence, at most the Desk’s acquisition at Treasury auctions can equal maturing holdings.

”

What it says is that primary market operations are limited to rolling over maturing bills and coupons — the net result is that the Treasury account cash holding is unchanged, therefore (c.p.), amount of reserves in the system would remain the same. Hadthe Feds ‘desired’ to decrease liquidity, they would let the securities expire.

(3)

I do not think this is so straightforward. The Australian banks’ settlement balances at RBA do not change of course but other monetary aggregates can. There are many examples I can give. The simplest is when an international bank happens to be the broker itself e.g., Citibank in Australia and the US. Assume the exporter has two accounts. One in AUD and one in USD. Citibank Australia will credit the exporter’s AUD account and debit his USD account. Citibank Australia has an asset “Due from Citibank US” and Citibank US has a liability “Due to Citibank Australia”. Citibank may either get rid of these entries or decide not to. Ref: Fed’s H.8

The M2 or M3 or whatever it is called in Australia has increased.

Another example. Start afresh. When the exporter gets paid in AUD, he reduces his indebtedness to the Australian banking system. Its automatic. The money supply in Australia has gone down.

VJK,

There have been various instances when the Treasury has had overdraft facilities at the Fed and also direct purchases of US Treasuries have been allowed in many periods.

Whatever the Fed pays the Treasury, if the Treasury hands the coin to the Fed, it has to accept it at the value inscribed on the coin. You may be talking of Fed picking up the bill on the production or something. You may be interested in reading “How the Costs and Earnings Associated with Producing Coins and Currency Are Budgeted and Accounted For” and Chicago Fed’s “Modern Money Mechanics.” The latter is nice but falls prey to the money multiplier.

Agree with you on Fed direct purchases. My point was just to get into geeky little things.

Some points on foreign currency purchases and fixed versus floating.

Many (most?) institutional setups have a big item on the central bank’s balance sheet “Claims on Banks”. If the central bank purchases foreign currency, – the central banks’ assets increase by the amount of foreign currency and the item “claims on banks” reduces by an equivalent amount. No change in the settlement balances occurs. Doesn’t matter fixed or floating.

Ramanan:

Right you are:

“Whatever the Fed pays the Treasury, if the Treasury hands the coin to the Fed, it has to accept it at the value inscribed on the coin.”

Let me correct my sloppiness:

“(2) Coin production is irrelevant. As I wrote elsewhere, “Banks *buy* currency from the Fed by having their reserve accounts debited – there is no money creation here.” The Fed pays the Treasury only the minute cost of currency production , not of course the currency face value.

”

Coins are FRB assets(bought at the face value) or Treasury liabilities, but currency (federal reserve notes) is FRB liability painted by Treasury/Mint and bought at the production cost.

So, yes, technically Treasury can finance its spending through coin issuance — are you hinting at a return to the gold standard ?

Ramanan:

“There have been various instances when the Treasury has had overdraft facilities at the Fed”

Article 14 of FRA contained an emergency loan provision between 1942 and 1980. It was removed, and I am not aware of any overdraft occurrence since.

”

and also direct purchases of US Treasuries have been allowed in many periods.

”

Could you provide a reference ? I am not aware of any such purchase.

VJK,

No, I am not hinting at a return to Gold Standard!

Just pointing out a technicality which can be used. Its like a bazooka in your pocket. If others know it, you don’t have to use it. Unfortunately others think that the Fed or the Treasury can “print money” etc. They are right in some sense. Some people knowledgeable know about the seigniorage powers. However, they are wrong because they think that money is printed regularly on supply whereas currency notes are printed on demand. When banks face some pressure with cash, they ask the central bank. Its fully dependent on the demand of the household sector.

These two articles are nice

link_http://www.gao.gov/new.items/d071105.pdf

link_http://www.gao.gov/new.items/d061007.pdf

Has details on these arrangements you are looking for such as “Cash and securities draw authority”. Also during the WWII, the Fed set the yield curve for the Treasury.

Coming back to the Gold Standard, there was no mechanism for adjustment of the balance of payments problems. In my view its still problematic. MMTers keep talking of “net saving desire” and that its no problem. Formal Post Keynesian theorists know its an issue.

A deficit hawk can use the same argument “Our standard of living has barely impacted” etc. Its important to realize that the rest of the world is Australia’ creditor. The net claims of foreigners is 60% of GDP ? The cost of servicing this debt is high. I know the usual MMT argument “simply credit bank accounts”. Its important to realize that fiscal policy is restrictive because of current account deficits whereas MMTers think “its even better”.

Ramanan,

Making any progress?

🙂

anon,

You mean all my efforts are going in vain ? 🙂

“The middle section of the graph is occupied by the private (non-government) sector. It exchanges goods and services for the currency units of the state, pays taxes, and accumulates the residual (which is in an accounting sense the federal deficit spending) in the form of cash in circulation, reserves (bank balances held by the commercial banks at the central bank) or government (Treasury) bonds or securities (deposits; offered by the central bank).”

Maybe I’m not reading that correctly, but where are the demand deposits created from debt? For example, I get a mortgage from a bank. I give the check from the bank to the builder. The builder then deposits it at the same bank in a checking account.

Bill,

I would like to ask about what actually govt tax is paid from? does tax only paid by money received via vertical transaction i.e monetary base?

How about the monetary expansion from the non-goverment sectors economic activity (horizontal transaction)? although these horizontal transactions is net to zero, but if I assume correctly, it means that the broader the expansion is also an indiaction of non govt sectors are making more profit and govt would recieved larger amount of tax on that.

Cheers

@ Fed Up

By balance sheet expansion at the bank when you ‘create’ the mortgage. All banks can do this trick but they are capital constrained and can only create so many mortgages before they need further working capital. The only bank that is not capital constrained is the central bank/government and effectively it only has political limits not financial ones.

It goes like this

Debit bank assets, credit reserves creates the mortgage and expands the balance sheet (leverage magic that actually expands money), Debit reserves, credit your checking account – then gives you the ability to withdraw something (the deposit is created). When the builder deposits it is debit reserves, credit their checking account (just a normal transaction and creates nothing).

AIUI

In reality, monetary policy and fiscal policy are also is an indication of a government’s stance on the exchange rate. A central bank cannot set the rates to zero and neither can the ministry of finance choose its policy without keeping the foreign exchange rate in mind. Its quite a nice problem for game theorists to look into.

“But even more preferable is to allow the short-term interest rate to drop to zero by not issuing public debt or paying a support rate on excess reserves. Then the interbank market will compete the rate down to zero each day and fiscal policy would become the principle counter-stabilisation tool and the most effective means of disciplining price pressures in specific asset classes.”

Interesting. What would happen if the RBA permanently set the cash rate target to 0%? What would happen to interest rates in other parts of the economy?

All government bonds would then yield 0%, so there would be no effective difference between cash deposits at the RBA and government bonds.

Would this not hold the entire yield curves for all credits much lower than they would otherwise be? Why isn’t this a recipe for asset bubbles?

Thanks for putting all this together in one post, Bill. It is a very handy reference, and I’m sure it will be getting a lot of hits over time.

For Gamma:

With no new bonds being issued new government deficits accumulate as excess settlement balances (excess reserves) in the banking system. Outstanding government bonds continue to be traded at market rates – short term bonds being heavily affected by the 0 interest rate on the overnight rate and longer term bonds affected by the zero rate and inflation expectations.

Bill has discussed house price bubbles, recommending they be controlled by restrictions on the availability of credit for mortgages. This was done to some extent in Canada, in part at the behest of the banks. More generally asset bubbles could be controlled by counter cyclical capital requirements for banks (see an earlier blog on this).

Keith, I think that all government bonds would be driven towards 0% yield. If the market (in particular the banks) truly believed that the central bank was going to keep the overnight cash rate of 0% indefinitely, then any yield would be preferable to the 0% on offer in the cash settlement accounts, hence banks would rather hold a bond that yielded something (even 20bps) to cash balances which yield nothing.

The reason that inflation expectations can effect long-term government yields in the market as it works at the moment is partly because the RBA has developed the credibility with investors that it will respond to inflation with higher rates.

The way I look at, you can think of 2 types of investors in the bond market:

1) Real money investors who actually have cash to invest – these people are concerned about inflation

2) Banks who borrow money from the RBA to invest – these people don’t care about inflation, they only care about what the cash rate will be for the life of the bond

With a 0% cash rate, the price of bonds would be determined by investor type 2, and type 1 would be driven out of the bond market and into real assets.

So with the possibility that this sort of policy could (potentially) cause such instability, why would we do it? What is the benefit of having 0% interest rates? What does it achieve?

Gamma,

I take your point about inflation and the bank rate, i.e. the long bond rate is actually a reflection of what investors believe the future bank rate will be – presumably influenced by expectations of future growth and inflation, for instance.

But I think your type 2 buyer of bonds will be out of luck. If the treasury no longer issues bonds there simply will be no additonal ones to buy. I suppose your point is the banks will try to buy all the remaining outstanding government bonds and bid the price down to zero. Nonetheless, collectively, the banking system will still be stuck with excess settlement balances paying zero interest. This will in fact be a burden on the banking system as it accumulates zero interest assets for which it has no outlet and so depress its profits. In effect the banks would carry all future government deficits with no compensation. I imagine the banks would then increase various charges, suppress wages, reduce interest on deposits, etc, to make up the shortfall. I guess I’m not entirely convinced this is necessary. Why not pay some small interest rate on excess settlement balances if you don’t want to issue bonds?

In any event I think Bill and Warren have made the point somewhere, in a presentation to a Parliamentary committee perhaps, that the issuance of bonds is a subsidy to the banks and is unnecessary. They note that while treasury securities are the risk free asset on which the banks base their rates, I believe they say the banks should develop their own debt instruments independently and not sponge off the State.

Why do you say the end of government bond issuance would lead to instability? There would still be a positive interest rate in the private bond market.

Keith, I think we agree that the commonwealth government bond market would no longer exist, and there would be little or no distinction between cash balances and government bonds – both would yield 0% irrespective of what inflation was, and was expected to be.

The problem is that these 0% rates across all government maturies would be likely to bias all other credit curves downwards.

For example, consider that you were a bank sitting on a large portfolio of federal government issued assets yielding 0% (cash balances and govvie bonds). You look over into another part of the market and see bonds issued by the Queensland State government trading at a non-zero yield. Queensland is considered a semi-government issuer, they have some powers of taxation and many people believe they possess an implicit guarantee from the federal government. They are a very strong credit, and you would definitely buy those bonds and pick up some yield, rather than sit on your portfolio that yields nothing.

And likewise out the credit spectrum, a similar effect would probably ensure all interest rates would be lower than they would have otherwise been.

What happens if interest rates are less than the rate of inflation? Why would anyone want to hold cash balances which yield nothing, or private-sector bond issues which yield something less than the rate of inflation?

Eventually everyone would be scrambling to get into real assets like real estate or financial assets without fixed interest and principal payments (ie equity/shares). This sounds like a highly unstable situation to me.

Gamma . . . if everyone goes into non-bond assets, then that by itself would raise the yield on non-govt bonds.

I think the consolidation of the central bank and treasury and the concept that taxes revenues are trashed tends to mask an important aspect of the monetary system. The economy runs on credit money which is sensitive to the interest rate on bank loans. The central bank therefore cannot choose not to set a target for the interest rate on interbank loans of reserves and control it through open its market operations. The alternative of controlling the quantity of banking system reserves and leaving the interest rate as a residual is impractical. Firms and households cannot plan efficiently unless they know the cost of credit going forward, at least for the relatively near term.

In reality the treasury can only spend what it has previously acquired through taxes and the sale of securities to the public. A more realistic representation would show a balanced circular flow of funds between the treasury and the private sector in which the treasury recaptures its deficit spending on average through the sale of securities to the public, and maintains its account at the central bank at a nominally fixed level to enable the central bank to control of the short term interest rate. Ultimately the government must ensure the value of its currency by widely enforcing tax collection and acting to maintain a modest rate of inflation through its control of the cost of credit money. I think this a fundamental constraint on any modern economy and should therefore be reflected in the flow funds model.

William Hummel

In reality the treasury can only spend what it has previously acquired through taxes and the sale of securities to the public. No, this the reverse of the truth, and logically impossible. Where did the first dollar come from? The public can only buy securities or pay taxes with what it has previously acquired from the treasury spending.

the treasury recaptures its deficit spending on average through the sale of securities to the public Yes, that is what reserve draining is about, which is a focus of MMT operational description.

“In reality the treasury can only spend what it has previously acquired through taxes and the sale of securities to the public.”

“No, this the reverse of the truth, and logically impossible. Where did the first dollar come from?”

Answer: The first dollar was created long before the modern fiat money system came into existence. Thus the MMT model of a fiat money system being initially funded out of Treasury spending has no basis in reality.

In normal times the Treasury (1) balances its inflows against outflows on average to avoid affecting the money supply; (2) targets a constant balance in its account at the central bank to minimize the effect on aggregate reserves in the banking system; (3) which enables the central bank to maintain control of the short-term interest rate by adding or draining reserves as required. This is entirely consistent with MMT, but I think it provides a more realistic and useful picture of flows in the “vertical” component.

Willilam Hi,

“the MMT model of a fiat money system being initially funded out of Treasury spending has no basis”

If you look at this archeological find, you can see that the Romans were using 250 year old coins (denarius from 200 BC) in Brittannia

after they first arrived there around 64 AD.

Link here.

They had to have brought these coins with them and initially spent them into circulation as I doubt the native residents of Brittannia could have acquired them otherwise before the arrival of the Romans in the first place. Or could the Romans demand payment of poll tax from the Brittans in 64 AD payable in 200 BC Roman denarius without ever having been there before? Ancient Brittans from 200 BC trading goods for an external currency for 250 years?

Resp,

“If you look at this archeological find, you can see that the Romans were using 250 year old coins (denarius from 200 BC) in Brittannia after they first arrived there around 64 AD.”

What do Roman coins have to do with a modern monetary system based on FIAT money that began in 1934?

William

Sorry William,

I thought you were writing about the sequence of events “in general” for a ‘fiat’ type currency, not the specific sequence of events wrt the US monetary system in the 20th century.

Resp,

Matt,

The balanced circular flow of funds model applies equally to many other fiat money systems, not just the current US monetary system. It derives from the need to manage the short term interest rate. The flow from government spending to its recapture through taxes and the sale of bonds can be easily traced. The consolidated government model (Treasury and central bank) showing a one way flow ending with the destruction of tax revenues gives no hint of that constraint.

William

William,

” The flow from government spending to its recapture through taxes and the sale of bonds can be easily traced.”

I follow this if I look back for instance at the Romans in Brittannia as seen through my link above to the archeological record. The Romans had to recycle the physical 250 year old tokens as these coins “did not grow on trees”, so they of course had to get them back (physically) to be able to spend them again, they literally had to collect the coins back as taxes to be able to spend, I think this is clear.

But why do we have to look at it the same way now, 2,000 years later when we have modern information technology and “money” can exist on computers?

It seems to me that Prof Mitchell here (MMT) looks at things in the context of our present society’s contemporary information technology. Is it not possible to look at it the way Bill does here and still manage the interest rate if you think that is necessary? Do we have to pretend that we are still back in the BC days to manage interest rates?

Resp,

Matt,

It can be useful at times to consolidate the Treasury and the central bank (CB) in understanding MMT. However consolidation can also mask important aspects of the monetary system, and is not essential to understanding MMT.

Only the central bank can create deposits of fiat money out of thin air. The Treasury cannot pay for its spending by simply creating deposits at the CB for the seller’s bank. Every dollar it spends means a debit to its own account at the CB. The Treasury must acquire its fiat money through taxes and the sale of debt securities. In the US system, the Treasury deposits its tax and loan receipts in the banking system and then transfers what it needs to cover its spending to its account at the CB. This is the reflux part of the balanced circular flow that I previously alluded to. The notion that payments to the government, e.g. tax receipts, are shredded by the Treasury must be viewed as a metaphor, not as reality.

The horizontal component of the MMT model is a function of the short-term interest rate which is controlled by the vertical component. That sets a constraint on the vertical component which is economically important in terms of policy. However that constraint is not apparent in the consolidated government model, although I have seen it mentioned briefly in the text of some MMT articles. In my view it deserves more than that.

William

William,

I believe I understand the current process as you descibe it, I am aware how the different balances can effect monetary policy, etc.. but please let’s remember that this is all just an accounting, and should take a back seat to outcomes imo.

The “shredding” ok it is a metaphor, but could you not consider the ‘netting’ that goes on in the various Treasury and CB accounts the modern IT system equivalent of ‘shredding’, your use of the word “flow” is a metaphor also, these ‘funds’ do not actually “flow” now do they? Also, do you view these procedures any differently now the the US CB can pay interest on reserve balances, does this not give the US the ability to cease bond issuance as now bonds are not needed to maintain a non-zero monetary policy?

You may be comfortable with your view of this process, but then tell me, how do we disabuse the general public of their perception that the Treasury is “borrowing from our grandchildren” by issuing a Treasury security? Do you agree that the current mainstream framework is easier to use to deceive the public perhaps to the advantage of a select few? Or if you wont go that far, do you agree that most if not all of our US policymakers do not have the correct level of understanding of these procedures that would be appropriate for them to successfully run fiscal and oversee monetary policies?

How do you view these non-operational issues?

Resp,

Matt,

“I believe I understand the current process as you describe it, I am aware how the different balances can effect monetary policy, etc.. but please let’s remember that this is all just an accounting, and should take a back seat to outcomes imo.”

I don’t know what balances you are referring to, or what you mean by “this is all just an accounting”. In the US today, monetary policy is about the only government tool available for managing credit money. Fiscal policy is now virtually non-existent. Congress has become a captive of moneyed interests, primarily the mega-banks.

——————

“The “shredding” ok it is a metaphor, but could you not consider the ‘netting’ that goes on in the various Treasury and CB accounts the modern IT system equivalent of ‘shredding’, your use of the word “flow” is a metaphor also, these ‘funds’ do not actually “flow” now do they?”

I don’t see any relation between “netting” and “shredding”. The latter implies that the Treasury creates the money it spends, which is untrue in normal times. Only in extremis (as in WW2) when it borrowed directly from the CB would it be fair to say that it created the money it spent.

You could consider the term “flow” as a metaphor for the movement of money, but it is widely used and understood. It certainly doesn’t carry the baggage of “shredding” as a metaphor.

——————

“Also, do you view these procedures any differently now that the US CB can pay interest on reserve balances, does this not give the US the ability to cease bond issuance as now bonds are not needed to maintain a non-zero monetary policy?”

No, the paying of interest on excess reserve balances is a free lunch for banks just for being depositories. I don’t consider that to be an acceptable alternative to the Treasury issuing interest-earning bonds to the public. The size of the budget deficit is far too large on average. Without selling bonds to the public, the free lunch for banks would quickly grow to outlandish proportions. It’s OK to pay interest on reserves at a rate somewhat below the target rate, as is done in Australia and Canada for example. Banks would then have no incentive to sit on reserves as an alternative to lending to the public in normal times.

———————

“Do you agree that most if not all of our US policymakers do not have the correct level of understanding of these procedures that would be appropriate for them to successfully run fiscal and oversee monetary policies?

I agree that very few in government understand a fiat monetary system, and economic issues that it affects. However the term “fiscal policy” is an oxymoron. It almost always works to the exclusive advantage of the moneyed interests, at the expense of the general public. Consequently we cannot depend on it on a continuing basis. That appears to leave monetary policy as the only potentially effective policy tool.

William

William –

Why would paying interest on reserves give banks no incentive to lend to the public in normal times? Bill has many blogs on the fact that lending is not reserve constrained.

I can understand your frustration with the current US political system vis-a-vis its fiscal policy, but I think you are confusing artificial constraints placed on the US Treasury with the true operational reality.

Rob,

“Why would paying interest on reserves give banks no incentive to lend to the public in normal times? Bill has many blogs on the fact that lending is not reserve constrained.”

Bank lending is capital-constrained, not reserve-constrained, as I’m sure Bill would acknowledge. But you appear to have misunderstood what I said: It’s OK to pay interest on reserves at a rate somewhat below the target rate, as is done in Australia and Canada for example. Banks would then have no incentive to sit on reserves as an alternative to lending to the public in normal times.

Of course these are not normal times. Large US banks currently hold a huge excess of reserves, and they receive interest on those reserves. That inclines them to hold a sizable fraction of the excess simply to draw interest rather than risk losses through bad loans, especially when the economy is in recession and there are relatively few creditworthy borrowers.

—————-

“I can understand your frustration with the current US political system vis-a-vis its fiscal policy, but I think you are confusing artificial constraints placed on the US Treasury with the true operational reality.”

I’d like to know what artificial constraints on the Treasury you think I am assuming. Surely you don’t mean to imply the Treasury can spend by simply crediting sellers accounts without covering them with its own funds. Indeed there is no need to do so because it can acquire what it needs through the sale of its own securities, which is exactly what it does when tax revenues fall short. In extremis it could borrow directly from the Fed, but that hasn’t happened since 1951.

William

William

The “interest on reserves is an opportunity cost to lending” argument is simply wrong. Interest paid is 0.25%. At best, offsetting liabilities are 0%, probably more, especially when you factor in non-interest costs of liabilities. IOR hurts bank asset turnover, and probably (at least now) profit margins. If a creditworthy customer comes in the doors, the bank will make the loan, but for reasons unrelated to IOR banks have increased their standards for creditworthiness (as they always do in recessions/slowdowns) and there are many fewer who see reason to borrow at this time. IOR isn’t the problem.

Even if IOR were higher, it’s still the equivalent of interest earned on a Tbill, basically, and I almost never hear anyone say “why are all these Tbills floating around . . . banks won’t lend since they can just hold Tbills!” Any loan, with or without IOR, has to be a better investment than the risk-free rate. IOR doesn’t change that.

Best,

Scott

William:

”

That inclines them to hold a sizable fraction of the excess simply to draw interest rather than risk losses through bad loans,

”

The banks simply cannot get rid of the excess reserves on their own without outside Fed’s help. That means that they do not have a choice but to sit on the reserves and collect the free lunch. Therefore, it is hardly fair to blame the banks for the existing extra reserves situation even though they may deserve plenty of blame elsewhere.

”

In extremis it could borrow directly from the Fed, but that hasn’t happened since 1951

”

No, it could not because it would be illegal in the current operational reality. Although, it could in 1951 when a special provision existed to let the Treasury do that.

Also, there were excellent comments by JKH on this issue several months ago at http://macromarketmusings.blogspot.com/2010/02/feds-exit-strategy.html

David,

Excess reserves are risk free assets. Risk free assets earn the risk free rate of interest.

Risky assets earn the risk free rate plus an expected spread. The purpose of capital is to underpin the risk around the expected spread.

Banks must allocate capital to risk. Therefore, the decision to take risk depends on the availability of capital.

A bank with adequate capital is itself an acceptable credit risk. That means it does not have a problem in attracting reserves required for settlement purposes. It can do this in the normal course by selling liquid assets or attracting new liabilities.

Therefore, the risk taking exercise does not depend on the availability of a stock of reserves. Any bank that formulates a strategy of risk taking based on reserves is simply being irrational and reckless. The textbook multiplier theory is an outrage in terms of its ignorance of risk and capital issues.

The Fed controls the supply of aggregate system reserves. When individual banks do engage in new lending, the best they can do is push the aggregate reserve distribution in the direction of other banks as a result. That is simply the result of the settlement mechanism. It does not reflect a process of “using” reserves.

Any bank CEO that would formulate a strategy of risk taking primarily in an effort to “use” reserves would be foolish. The best the bank could do is contribute in a minor way to the conversion of system excess reserves to system required reserves. The effective reserve ratio of the system prior to the crisis was less than one per cent, due to the preponderance of non-reservable time deposits in the total checking/savings/time deposit mix. Based on that mix tendency, the US banking system would have to create more than $ 100 trillion in new loans and deposits in order to “use up” excess reserves. This line of thinking is just preposterous, and those who pursue it should spend more time on their numbers. Moreover, any strategy of risk taking designed simply to push existing system reserves over to the competition, regardless of normal risk analysis and capital considerations, is just outrageously reckless.

The proper strategy has to be risk and capital based on a loan by loan basis. So yes, I do expect those banks to behave in the same way.

And JKH later in the thread writes:

There is no opportunity cost associated with excess reserves provided that excess reserves are earning the risk free rate. This is because excess reserves are zero risk weighted for capital allocation purposes. Accordingly, they require no capital allocation on a risk weighted basis.

It is irrational for any bank risk/capital manager to allocate capital to risk simply on the basis of perceiving a nominal opportunity cost when earning the risk free rate on a risk free asset. It is wrong to view earning a higher risk adjusted return on risky assets as a substitute for lower earning risk free assets, without reference to capital requirements. A higher compensation for risk is a requirement with or without the alternative presence of risk free assets. So the presence of risk free assets is a red herring in terms of opportunity cost.

In terms of deposit costs, I referenced the fact that in this environment banks will be careful to review the interest rate structure (and the fee structure) on deposit accounts to ensure that net interest margins and related costs are reasonable compared to the risk free rate.

Scott,

Excess bank reserves now total about $1 trillion. Those reserves are mainly the result of Fed purchases of MBS and Treasurys from the non-bank sector. Banks were simply the beneficiaries as depositories.

Eventually the Fed will have to recapture most of those reserves. However that cannot be done quickly because of its impact on the market and the economy. If the Fed raised its target rate on Fed funds to say 4% before it recaptured those reserves, it would have to pay about $40 billion per year in interest on them, most of which would be a free lunch for banks. I would call that a problem.

I don’t understand your comment: “The “interest on reserves is an opportunity cost to lending” argument is simply wrong.” I didn’t say anything related to that.

William

William,

“fiscal policy” is an oxymoron. It almost always works to the exclusive advantage of the moneyed interests”

It doesn’t have to. In fact, I believe that perpetuation of modern day myths about the US monetary system act to deceive the public into believing that our options wrt fiscal are much more limited than they are in reality, or many folks, looks like yourself included, have sadly led themselves to believe that there are no fiscal options, William your comment in this regard sounds defeatist. This is a shame as monetary policy alone can never deliver continuous full employment/output , today’s zero rates and 10% unemployment being a prime empirical example.

I’d like you to consider: The US CB system (The Fed) only acts as the ‘fiscal agent’ of the US Treasury by the leave of that same US Treasury. It is not correct to believe that the US Treasury has to borrow it’s own ‘money’, in the same way, did the Roman govt borrow the coins that appear in the pictures in the article I linked to above, or just spend them into existence?

Resp,

“The banks simply cannot get rid of the excess reserves on their own without outside Fed’s help. That means that they do not have a choice but to sit on the reserves and collect the free lunch. Therefore, it is hardly fair to blame the banks for the existing extra reserves situation even though they may deserve plenty of blame elsewhere.”

I don’t blame the banks for collecting that free lunch. I blame the Fed for monetizing all those securities, thus loading up the banks with the reserves, and then paying interest on the reserves. The Fed had fought a long time for authority to pay interest on reserves and finally got it in Oct 2008, but the timing was bad. The original intent was to pay interest at a lower rate than the target Fed funds rate. That would have cost the Fed a trivial amount because banks would not hold much in excess reserves when they could lend them at the target rate. The QE1 program started at about the same time, and I think the Fed would have felt embarrassed to turn off IOR then. At an interest rate of .25%, the amount it has to pay is pretty small. However comes the day that the Fed wants to raise the target rate back to its historical level of 3 to 5 percent, the cost of the free lunch could be significant if there is still a very large amount of excess reserves outstanding.

—————

In extremis it could borrow directly from the Fed, but that hasn’t happened since 1951.

“No, it could not because it would be illegal in the current operational reality. Although, it could in 1951 when a special provision existed to let the Treasury do that.”

Of course that assumes that Congress would ignore extremis conditions and deny the Treasury that authority.

William,

Agree with you at 11:44. Regarding IOR as an increased opportunity cost of lending, you said interest on reserves “inclines them to hold a sizable fraction of the excess simply to draw interest rather than risk losses through bad loans”–that means they are less likely to lend than without IOR, and IOR is thus an increase in the opportunity cost of lending. Yes, true with long-term Treasuries where the return can be significantly higher than cost of funds (such as the early 1990s, but not true now), but not with Tbills or reserves earning interest.

Best,

Scott

Matt,

I agree that monetary policy alone cannot achieve the goal of continuous full employment. But don’t blame the Fed’s monetary policy itself for the 10% unemployment problem. Much more blameworthy was Greenspan’s laissez faire attitude regarding the products the financial system was creating. Too bad Warren Buffett wasn’t in charge.

—————-

“I’d like you to consider: The US CB system (The Fed) only acts as the ‘fiscal agent’ of the US Treasury by the leave of that same US Treasury. It is not correct to believe that the US Treasury has to borrow it’s own ‘money’, in the same way, did the Roman govt borrow the coins that appear in the pictures in the article I linked to above, or just spend them into existence?”

The US Treasury reports to the President and therefore has a political agenda as well as being a financial manager. I would never support the merger of the central bank with the Treasury. In spite of its sometimes dismal record, the central bank is one of the few bulwarks of our system. With its independence from the administration and its quasi-independence from an unruly and incompetent Congress, at least we know who is in charge.

The real problem with our government is Congress which has been thoroughly compromised by the money that members need to get reelected. The amount of money spent on lobbying Congressmen by megabanks and large corporations makes it obvious how serious the problem has become. How can one expect a coherent fiscal policy being generated under such conditions?

William

William:

”

However comes the day that the Fed wants to raise the target rate back to its historical level of 3 to 5 percent, the cost of the free lunch could be significant if there is still a very large amount of excess reserves outstanding.

”

When such a day finally arrives, the Feds can as easily stop paying any interest on reserves. I do not really see why they cannot do that today.

In any case, to stop paying that interest is fully within the existing Feds’s powers as opposed to the hypothetical with the Feds lending directly to the Treasury which would have required a legislative action.

However comes the day that the Fed wants to raise the target rate back to its historical level of 3 to 5 percent, the cost of the free lunch could be significant if there is still a very large amount of excess reserves outstanding.

—————

“When such a day finally arrives, the Feds can as easily stop paying any interest on reserves. I do not really see why they cannot do that today. In any case, to stop paying that interest is fully within the existing Feds’s powers as opposed to the hypothetical with the Feds lending directly to the Treasury which would have required a legislative action.”

If there is a substantial supply of excess reserves in the banking system, and the Fed pays no interest on them, the Fed funds rate will fall to zero. The only way the Fed could get the interbank lending rate up to say 4% is to offer 4% on the excess reserves. That sets a floor under the interbank lending rate.

Absolutely agree with VJK.

The purpose of paying interest on reserves is to raise the cost of funds for banks, so that credit growth it limited.

Well, I just got a parking ticket.

It seems absolutely crazy to assume that paying banks money is the only way that the government can raise the cost of funds for the banking system.

Have we been so captured by finance that this is the only thing we can think of doing? How about imposing a 3% asset tax on all non reserve assets held by the banking system. Wouldn’t that raise their cost of funds by 3%? And wouldn’t this be disiniflationary as well? Isn’t this the simple, direct, and the obvious thing to do?

Why is no one thinking rationally about this, and instead proposing paying interest as a way of imposing costs on banks?

William,

Based on some of your comments here, to me you have a handle on how this stuff works which puts you ahead of 99.9% of the voters here in the US. I submit, if this was the level of the general knowledge of the electorate, we would elect a better government.

The people would demand a government that delivered a fiscal policy that would result in full employment/output and the highest quality of life. Sure there would still be bribes/patronage/sweetheart deals/depravity, etc.. in govt, resulting out of a robust fiscal policy, but William we already have that with the raw deal we are currently suffering under.

Dont let the perfect be the enemy of the good here. With the right education/information/understanding, the voters will do the right thing politically. Fiscal policy is the power of the people, monetary policy is the power of the elites.

Resp,

“With the right education/information/understanding, the voters will do the right thing politically. Fiscal policy is the power of the people, monetary policy is the power of the elites.”

Regardless of their education/information/understanding, the first priority of most voters is their own perceived well-being. However that often conflicts with the social and economic welfare of the nation as a whole. Furthermore voters seldom vote directly on the issues; rather they vote on personalities to represent them in government. One can only hope that elected officials act in the broad interests of the nation rather than their own personal interests. Unfortunately, under the influence of moneyed interests, the record has been pretty dismal in that respect.

Fiscal policy should be the primary means of ensuring the best economic outcome for the general public. However in our separation of powers type government, it is very difficult to establish coherent policy. Perhaps more important than taxes versus spending is the actual use of government funds. While paying for two wars and a bloated military edifice, Congress has virtually ignored the infrastructure that underpins the domestic economy.

Monetary policy is not an alternative to fiscal policy; it should complement fiscal policy, but often needs to compensate for the lack of coherent fiscal policy. Wise monetary policy can be difficult because of the lags in system, but it is much simpler to implement. The officials responsible are fairly well insulated from government politics by the length of the term they serve (14 years).

Wm,