It's Wednesday and I discuss a number of topics today. First, the 'million simulations' that…

Can we really say the US economy is in recovery?

The latest US Federal Reserve Bank Bulletin – (Volume 100, No. 4) was released on September 4, 2014 and – Changes in U.S. Family Finances from 2010 to 2013: Evidence from the Survey of Consumer Finances provides a very deep insight into what has been going in America over the period since 2010 with some comparative data from 2007-2010. So we get a glimpse of what happened during the crisis period in family incomes and wealth holdings (by a number of different characteristics) and then see what has transpired during the so-called ‘recovery’. The results will lead you to question the extent to which using the term ‘recovery’ is meaningful. In the growth period 2010-13, only the top 3 per cent of the income distribution have enjoyed real income gains whereas the bottom 40 per cent have seen major real cuts. A similar story relates to changes in family wealth. The reality is the highest income earners are capturing the real income growth at the significant expense of the rest notwithstanding the overal decline in unemployment. It is a recipe for disaster – an increasingly unequal society where some cohorts have virtually no chance for upward mobility.

The Federal Reserve Board conducts a “triennial Survey of Consumer Finances (SCF) collects information about family incomes, net worth, balance sheet components, credit use, and other financial outcomes”.

The shift in fortunes between 2010 and 2013 is telling – the Bank says that the 2013 Survey “eveals substantial disparities in the evolution of income and net worth since … 2010”.

As a brief note on the use of statistical measures, the mean is the average of the whole sample whereas the median is the value in the sample where half the observations are above and half below. Both are so-called measures of central tendency of a sample of observations.

There are times when the median is a superior measure of central tendency relative to the mean and vice versa. The appropriateness of each depends on the circumstances.

The short rule of thumb is that when the distribution of observations is symmetrical, then the mean is the best measure. Otherwise, the median is generally a more reliable indicator.

The mean is limited in application because its value is sensitive to samples which have extreme values (large or small). The spread of observations that are skewed (right or left) if there are extreme values.

This is an important consideration when dealing with data that shows the distribution of household income. In this context, more people earn low incomes than extremely high incomes. The distribution across all households is not symmetrical.

For example, what might we conclude if the average household income rose over a period? This could just mean that a few very high income earning households had enjoyed income rises while people at the bottom of the income distribution could be enduring falling incomes.

In this case, it is better to use to the median.

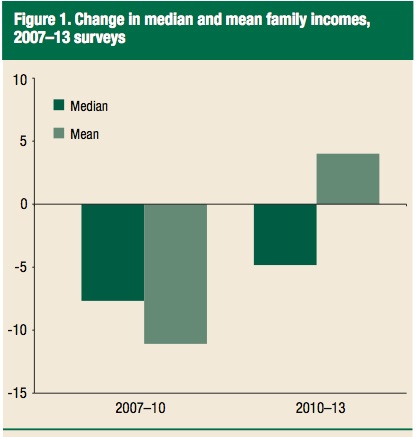

The Federal Reserve Bulletin article presents “Figure 1 Change in median and mean family incomes, 2007-13”, which splits the period into 2007-10 and 2010-13, coinciding with the two most recent SCF surveys.

The Figure (see reproduction below) shows that in the first years of the crisis, both the median and mean family incomes fell but in the period 2010-13, the mean family income rose despite the median falling.

The Bulletin notes that:

Between 2010 and 2013, mean (overall average) family income rose 4 percent in real terms, but median income fell 5 percent, consistent with increasing income concentration during this period.

In other words, the underlying inequality in the income distribution worsened in the second period (2010-13).

The first period saw the mean fall more than the median because very high income earners endured large declines in their incomes and then recovered those losses (to some extent) in the second period.

Further:

Families at the bottom of the income distribution saw continued substantial declines in average real incomes between 2010 and 2013, continuing the trend observed between the 2007 and 2010 surveys.

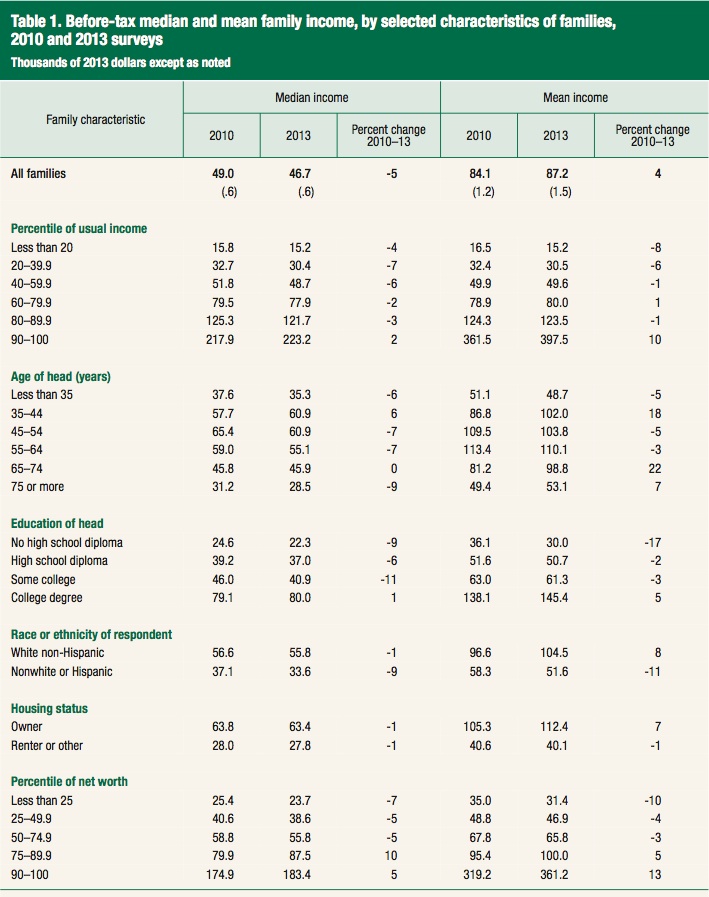

The following graphic is drawn from Table 1 of the Bulletin Report and bears on a range of issues that are relevant to understanding who has benefitted from the growth in national income since 2010.

The Bulletin notes “The changes for both the 2007-10 and 2010-13 periods stand in stark contrast to a pattern of substantial increases in both the median and the mean dating back to the early 1990s.”

You can see that there are “predictable patterns” across the demographic characteristics – “a strong positive association with education”, “Incomes of white non-Hispanic fami- lies are substantially higher than those of other families” and “income is systematically higher for groups with greater net worth”.

But an examination of the impact across the percentile distribution is telling.

The only group to enjoy income increases between 2010-13 were the top 10 per cent (Percentile 90-100). Their average annual income rose by 10 per cent (from $361.5 thousand to $397.5 thousand).

The groups between percentile 40 and 90 all went backwards by 1 per cent in real terms (note the data is expressed in thousands of 2013 dollars).

At the bottom end of the income distribution the lowest 20 per cent of income earning families lost 8 per cent of their average income and the 20-39.9 percentile group lost 6 per cent.

So the top 10 per cent were able to capture increased real income at the expense of the rest with the big losers being the bottom 40 per cent of the income distribution.

We might reasonably ask in what sense can one say that the US economy is recovering. The FRB Bulletin is cogniscant of that anomaly.

They note at the outset that:

Although aggregate economic performance improved substantially relative to the period between the 2007 and 2010 surveys, the effect on incomes for different types of families was far from uniform.

The FRB Bulletin also considers what has happened to the wealth distribution in the US over the period spanned by the last two SCF surveys.

In the last surveys, the data showed “showed dramatic decreases in median and mean net worth in the 2007-10 period, while the 2007 survey showed substantial increases relative to 2004.”

The “patterns in net worth over the past decade were largely driven by the boom and bust in house and other asset prices. The bust, in particular, had a disproportionate effect on families in the middle of the net worth distribution, whose wealth portfolio is dominated by housing”.

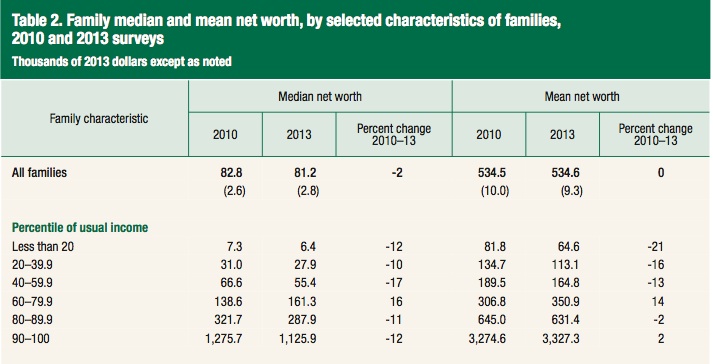

The following graphic is drawn from Table 2 of the Bulletin Report and show the movements in Family median and net worth. The family characteristics in the full FRB Table 2 are the same as those in the above Table 1. I have only included the income distribution characteristics in this verion.

The results are consistent with the information in Table 1. Overal, there has been no increase in average real wealth in America between 2010 and 2013.

But there are considerable variations across the income distribution underpinning this result. The wealthiest 10 per cent of families enjoyed a 2 per cent increase in their average wealth between 2010 and 2013. The 80-80.9 percentile group in the income distribution lost 2 per cent of their real wealth.

The bottom 20 per cent lost a staggering 21 per cent of their wealth (From 81.8 thousand to 64.6 thousand), the second lowest lost 16 per cent of their real wealth and the third lowest group lost 13 per cent of their average real wealth.

Running against the tide was the 60-79.9 percentile group which saw a rebound in real average wealth of 14 per cent over this period.

So what has been going on?

First, those on higher incomes can accumulate more wealth because their savings are higher and as they amass wealth the income flows that arise from the growing stock provide, in turn, for higher incomes and the cycle perpetuates itself.

Low income households do not save and cannot accumulate any significant wealth holdings or enjoy extra income flows.

The Survey revealed that between 2007 and 2013, the number of families reporting that they had saved fell in total, as family incomes became squeezed.

But underlying this result was the fact that in 2013 “the fraction of families in the top income group that saved was 82.4 percent. This percentage was more than double the 40.2 percent that saved in the lowest income group” and that the proportion only rose in top 10 per cent of income earning families.

Second, the 2013 survey “confirm that the shares of income and wealth held by affluent families are at modern historically high levels.”

Third, “the gains in income and wealth shares have been concentrated among the top few percentiles of the distribution.” This includes the top few percent rather than the popularised 1 per cent. The 99/1 division is misleading. Better to consider a 97/3 split.

The FRB Bulletin notes that “the share of income received by the top 3 percent of families was 31.4 percent in 2007 but fell to 27.7 percent in 2010 as business and asset income declined particularly sharply in the recession and financial crisis … Since that time, the income share of the top 3 percent has rebounded, climbing to 30.5 percent in 2013.”

So when we say the top 10 per cent have enjoyed real income growth since 2010, the additional fact that is relevant is that the 90-97 percentile group has seen their share of income remain static since 1989. All the action is at the top 3 per cent.

Fourth, changes in wealth shares are “less cyclical than income”.

Fifth, the share of wealth of the “top 3 percent climbed from 44.8 percent in 1989 to 51.8 percent in 2007 and 54.4 percent in 2013.” The share of the next 7 per cent has been largely unchanged (“hovering between 19 and 22 percent over the past 25 years, and registering 20.9 per cent in 2013”.

The “share of wealth held by the bottom 90 percent fell from 33.2 percent in 1989 to 24.7 percent in 2013”.

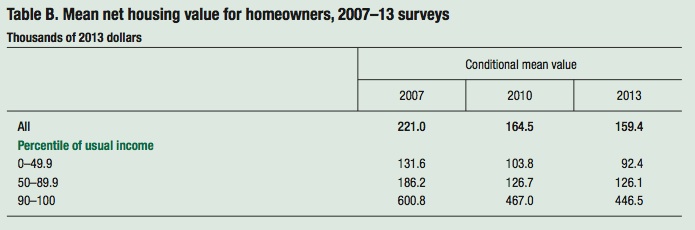

There has also been a dramatic decline in real housing values in the US between 2007 and 2013. The following graphic is taken from Box 8 Table B in the Bulletin article.

The FRB Bulletin concludes that:

Between 2007 and 2010, the mean net value of housing fell between 20 and 32 percent for all three usual income groups. Between 2010 and 2013, mean net housing value continued to fall for all three groups, but the magnitudes of the declines differed substantially. For the upper-middle income group, mean net housing was essentially unchanged between 2010 and 2013, falling just $600. For the bottom income group, net housing value fell 11 percent between 2010 and 2013, and for the top income group, net housing value fell 4 percent.

At the same time, the real “level of education loan debt held by U.S. families has increased dramatically over the past decade” from an average figure of $16.9 thousand to $29.8 thousand. While this debt is concentrated on families with incomes of more than $60,000 per year (which puts them above the 60 percentile in the income distribution), a much “larger share of education debt was held by young … families with incomes of less than $30,000.”

Conclusion

I thought the survey results were an interesting supplement to the other material that is available which shows who is capturing the income growth in the US economy since the so-called ‘recovery’ began.

It is clear that income growth has been positive since the ‘recovery’ began. But the growth has not benefited all. Even though employment growth has occurred across the income cohorts, the suppression of wages growth at the bottom end of the distribution has precluded the lowest waged workers from participating in the largesse, what there has been of it at that.

The dynamic unfolding in the US is deeply disturbing.

Last week, the Australian Broadcasting Commission broadcast a 2012 BBC documentary called – Park Avenue: Money, Power and the American Dream – by Alex Gibney, which examined the behaviour of those who live at – 740 Park Avenue, Manhattan (the richest apartment building in the world inhabited by the likes of David Koch, Stephen Schwarzman and John Thain live. Thain oversaw the demise of Merrill Lynch but still pocketed a fortune.

It is where “the 1 per cent of the 1 per cent” live and “Ten minutes to the north, across the Harlem River, is the other Park Avenue, in the South Bronx. Here, unemployment runs at 19% and half the population need food stamps” (Source).

You can view the film – HERE.

It categorically debunks any notion that the US is a land of equal opportunity and that through hard work and initiative a person can move across the river to join the high income and wealthy elite of the US.

It also shows how this group use their incomes and wealth to manipulate the US political system in their favour.

The data shown in the FRB Bulletin provides one little glimpse of how successful these characters are. In the midst of the worse crisis since the Great Depression and its aftermath, the top 3 per cent continue to prosper, albeit at a slower rate of growth than prior the crisis.

But the poorest Americans have gone backwards in a significant way and that cycle becomes one of despair.

The policy framework is all wrong and somehow the people of the US have to seize it back.

That is enough for today!

(c) Copyright 2014 Bill Mitchell. All Rights Reserved.

Is the world of work changing?

I am indebted to Bill for providing evidence to support the view that inequality has increased since the GFC began. There are means available to tackle this problem and it is hoped that political and economic policies will be enacted to achieve this.

The wider question arises as to how much of the problem arises from a relative decline in the wealth generating potential of a Western world that is losing its productivity drive compared say, with emerging Eastern economic powerhouses.

If this relative decline is a fact, it may mean that the West has again to adjust its wealth sharing criteria to avoid the rise in inequality that we are witnessing.

It may also be the case that the profound changes in Eastern production capacity coupled with technical advances change large areas of employment and the West has yet more adjustments to make in its dispersion of wealth.

Bill,

Your upcoming project on income inequality sounds very interesting. Have you checked out the approach taken and the data generated by the University of Texas Inequality Project? The data they provide is very extensive and brilliantly broken down. The potentials for exploration are fantastic. And their use of the Thiel statistic seems to me a refreshing approach to the problem.

http://utip.gov.utexas.edu/

Also worth a look. Lots of good links in here to data sources.

http://www.advisorperspectives.com/dshort/commentaries/Real-Median-Household-Income-Growth.php

Bill ~ Please remember, the US elections are coming up, so anything the government here says regarding our welfare must be suspected (more than usual) as being campaign propaganda. We’ve got two full months before then, and already our TV boxes are jammed with (mostly negative) campaign ads. (It’s not uncommon to see two ads back-to-back, one each for opposing candidates, that are on the same issue, with each being directly opposite of the other. It’s really a hoot, but it says these people really have WAY TOO MUCH money to spend, money that could be far better spent on a job guarantee.)

It is eery how similar today in the USA is to the one in Minsky’s of 1971. All the analysis in his talk “Where the American Economy-and Economists-Went Wrong” would, with the change of a few names and dates, seem to be written today. His “guns and butter” inconsistency breakdown of GDP benefits to classes is especially helpful in illustrating what you are describing here. I am only starting to understand this point now, to my shame. For those like yourself who have been able to see that clearly for that long, and still find time to illuminate others like me with the minimum of rancor with a blog like this, is humbling indeed.

The people siezing back control over the policy framework would be very difficult without major constitutional reforms. It seems that elite control of the policy framework was always part of the plan:

http://www.counterpunch.org/2014/09/05/how-would-you-change-the-constitution/

Was the US ever a land of equal opportunity ?

Talk of equality is usually meaningless propaganda or wishful thinking.

All that can be hoped for is a government which legislates for and promotes fair outcomes for all citizens. The US is a long way from that and so is Australia.

The Marxist Professor Richard D. Wolff certainly agrees that the US “recovery” is not a recovery at all and that the bottom 90% (or so) are getting poorer. He is predicting the collapse of the American middle class. His analyses of last stage capitalism are very good. He certainly explains the current decline of the West very well. Borderless capitalism naturally moves real production to the areas with low labour costs like China. The West is responding with financialisation and is able to imperialistically capture some of the new action that way. But financialisation is an empty bubble in the long run.

The bottom line is that the West is now being de-industrialised relatively and very soon it will be happening absolutely. At the same time, Limits to Growth will bring “Chindia” and its rapid industrialisation to a crunching halt also relatively soon. All the chips are about to be thrown in the air. We are closely approaching a crisis period of rapid change, major disruption and disjunction.