It was only a matter of time I suppose but the IMF is now focusing…

Still sinning … a German economist who cannot face facts

German economist Hans-Werner Sinn, who has been implacably opposed to the Eurozone bailouts and so-called debt mutualisation is at it again with an article in the UK Guardian yesterday (October 22, 2014) – Europe can learn from the US and make each state liable for its own debt – calling for Eurozone states to be forced to take responsibility for their own public debt and became bankrupt if that responsibility leads private creditors to cease providing funds to these states. Like all these vehement (and often German) perspectives on the Eurozone crisis, his solution based on a comparison with the federal arrangements in the US, leaves out the crucial element that renders the comparison invalid – the lack of a federal fiscal function in the Eurozone (compared to the US). Further, his solution would have led to the Eurozone breaking up in 2010 had it been implemented at that time. It’s what happens when one is blinkered by an ideology that does not permit evidence and experience to modify its more extreme dimensions.

I have discussed the ideas of Hans-Werner Sinn previously in these blogs – Rescue packages and iron boots and Defaulting on public debt as a way to progress and Selective versions of history, driven by a blinkered ideology, always fail.

It seems that Dr Sinn is not an adaptive creature who learns from his mistakes.

Back in 2012, Dr Sinn appeared before the German Constitutional Court which was considering whether the European Stability Mechanism (ESM) is “compatible with Germany’s constitution”. In this regard, there was an interesting article on German economist Hans-Werner Sinn in Der Spiegel (July 1, 2012) – Professor Propaganda Is German Economist Exacerbating Euro Crisis?.

His opposition to the Eurozone bailouts was expressed in this New York Times article (June 13, 2012) – Why Berlin Is Balking on a Bailout where he wrote:

… such a bailout is illegal under the Maastricht Treaty, which governs the euro zone. Because the treaty is law in each member state, a bailout would be rejected by Germany’s Constitutional Court … [and] … a bailout doesn’t make economic sense, and would likely make the situation worse. Such schemes violate the liability principle, one of the constituting principles of a market economy, which holds that it is the creditors’ responsibility to choose their debtors. If debtors cannot repay, creditors should bear the losses.

If we give up the liability principle, the European market economy will lose its most important allocative virtue: the careful selection of investment opportunities by creditors. We would then waste part of the capital generated by the arduous savings of earlier generations. I am surprised that the president of the world’s most successful capitalist nation would overlook this.

When I read this article I wondered why he hadn’t recognised the massive failure of the “liability principle” to allocate investment resources appropriately.

The massive pre-crisis German trade surpluses were not being used to reward their own workforce in the form of real wages growth. Given the stifled domestic demand, the German funds flowed south. The speculation in Greece and Spain came from German (and French) money.

How much capital was wasted through the folly of the financial markets as a result of this crisis? The idea that you leave it to the ‘markets’ to resolve everything assumes that they are working for the good of all humans and are effective in doing so. Neither proposition is remotely true.

Further, the ‘markets’ are not even effective at advancing private interests at times as the GFC proved without doubt.

But I agreed with him that the bailout strategy currently in place will never work because it is accompanied by austerity which kills growth and therefore kills the wherewithal to pay back the debt.

In the Spiegel article, Dr Sinn is reported as telling the Constitutional Court that there would be “bottomless pit” and the ESM would become a “machinery of asset destruction”. He was, of-course, referring to financial asset destruction, which is really the problem.

The world is obsessed with financial assets and forgets that there is massive asset destruction going on every day as a result of this misplaced emphasis. I am referring to the entrenched mass unemployment which is wasting the most valuable assets that an economy ever has.

Youth unemployment (official or hidden) and underemployment above or approaching 50 per cent in many nations now constitutes massive asset destruction.

Fiscal austerity is a brilliant machine for ensuring this destruction persists and increases.

Dr Sinn’s belief that the “liability principle” (that is, the free market) will stop this destruction is misplaced. Without strong regulation and government deficits (typically) mass unemployment and rising inequality become the norm rather than the exception.

But he is still at it in 2014. In the Guardian article he writes:

The eurozone should emulate the US approach in how to maintain stability in a monetary union

Really. If that was to be then there would be a major federal fiscal function created as the responsibility of the European Parliament (being the only elected body that spans all the Eurozone nations. It would stand ready to transfer massive amounts of euros to beleagured Member States, who had surrendered their currency-issuing capacity when they joined the monetary union.

But the blinkered Dr Sinn does not really want there to be a true emulation of the federal-state arrangements in the US existing in the Eurozone.

What he wants is something far more limited, which would actually destroy the Eurozone.

He asserts that:

… a fundamental flaw in the structure of the European Monetary Union … [is the absence of] … the liability model …

Yes, he is still on about that.

He claims that the alternative to the liability model – “the mutualization model” – aka the collective bailout model is failing to stop nation states building up debt and violating the fiscal compact – the revised Stability and Growth Pact (SGP), which “sets a strict ceiling for a country’s structural budget deficit and stipulates that public-debt ratios in excess of 60% of GDP must be reduced yearly by one-twentieth of the difference between the current ratio and the target”.

He is keen to tell us that the fiscal compact, which tightened the SGP straitjacket even further, was “as the quid pro quo for Germany to approve the European Stability Mechanism”. We know that the Germans bullied the other nations into agreeing to tightening the constraints, which had already created massive damage across the Eurozone economies.

The fact that the French and Italian governments, the other big economies in the currency union, are now proving that they cannot politically sustain the austerity required to satisfy the revised SGP rules, given the sustained mass unemployment and rising social instability (which manifest in the May European Parliament elections), is testament to the inapplicability of these rules to the real world.

They just blow economies up when aggregate spending is weak. People will not tolerate mass unemployment, increased poverty rates and widening income inequality forever. There will be a point where society will fight back against the mindless technocratic rules that the Germans and Dr Sinn seem to think are reasonable.

The recent decline in economic activity in Germany is also testament to the unworkability of the fiscal structures imposed on the Eurozone by the technocrats.

Dr Sinn’s solution to the malaise is to abandon the mutualisation model and force each Member State to take:

… responsibility for its own debts, with its creditors bearing the costs of a default. Faced with that risk, creditors demand higher interest rates from the outset or refuse to grant additional credit, thereby imposing a measure of discipline on debtors.

So, if a nation is facing insolvency, the private bond markets will refuse to grant it additional credit. It will then default – become bankrupt given that the ECB would not be able to intervene as it did in May 2010 with its Securities Market Program, which saved the Eurozone.

What would happen then?

Well the state would have to severely cut spending very quickly and try to raise extra tax revenue. In Greece’s case, the public debt ratio jumped from 107.4 per cent in 2007 to 148.3 per cent by 2010. Between 2008 and 2009, its primary balance (that is the difference between spending and tax revenue net of interest payments) went from 4.8 per cent to 10.5 per cent of GDP. Real GDP growth fell by 3.1 per cent in that year, the relative calm before the storm.

Remember, that significant parts of the rising deficits in the Member States were due to the cyclical effects on their revenue. Unemployed people pay no income taxes and VAT taxes fall when spending falls. Trying to constrain those cyclical effects with discretionary cuts to net spending, which is what the SGP in all its incarnations requires only makes the initial spending collapse worse.

If the government had have been forced to close its primary deficit of 10.5 per cent in that year imagine what would have happened to total spending and growth. It was bad enough. In the ensuing years, with the bailouts, mass unemployment rose beyond 25 per cent and youth unemployment touched 60 per cent.

Without the bailouts, Greece would have left the Eurozone. It would not have been able to politically sustain the social unrest that would have accompanied the economic disaster that would have occurred.

Dr Sinn seems to think that these nations would simultaneously resist reintroducing their own currencies (and thus abandoning the Eurozone) and bear the costs of massive unemployment and increased poverty. He is living in a dream world and should get out more.

If Greece had have paved the way to exit the Eurozone other nations would have soon followed. Maybe not the culturally compliant Ireland but almost assuredly Spain and then Italy. Both would have been able to observe that with its own currency in place, Greece would have resumed growth almost immediately and staved off the disaster that followed and endures to this day.

Dr Sinn seems to believe that his plan:

… would serve notice to investors that they cannot hope to be saved by the printing press in times of crisis, and would thus compel them to demand higher interest rates or deter them from granting credit in the first place. This would lead to greater discipline among the eurozone’s indebted countries and save Europe from a debt avalanche that could ultimately drive currently solvent states into bankruptcy and destroy the European integration project.

His plan would not “ultimately” create bankruptcy but, rather, would immediately force nations into bankrupt states with mass unemployment.

Forcing nations to live under the German yoke would also increase the right-wing extremism that is now mounting in Europe and surely undermine the European integration project more quickly than anything else that could be contemplated.

What is his motivation? Well he thinks the Eurozone should emulate the US. He thinks:

The best example of the liability model is the United States. When US states like California, Illinois, or Minnesota get into fiscal trouble, no one expects the other states or the federal government to bail them out, let alone that the Federal Reserve will guarantee or purchase their bonds.

US states can go bankrupt – that much is true. And the Federal Reserve doesn’t buy the debt of the States. Again true.

But that is as far as the comparison goes.

The US comparison

The first point to note is that the US suffered a terrible recession as a result of the collapse of the housing market and the subsequent spread of panic, which severely undermined total spending in the economy. Even with an active federal function and currency sovereignty the US downturn was severe and prolonged.

What that told us was that the fiscal stimulus, massive though it was in the US, was still inadequate and was not sustained for long enough. The intervention as a percent of GDP could have been much larger.

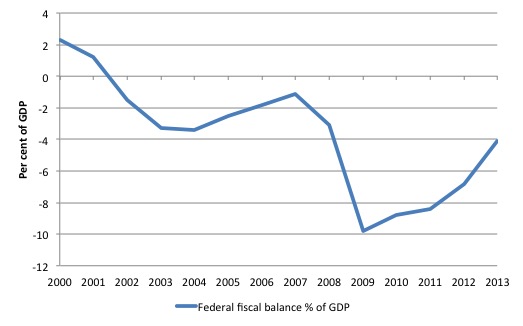

The amount of federal net spending that was injected into the US economy directly through the Federal fiscal balance in 2008-10 via discretionary stimulus measures and the automatic stabilisers (lost tax revenue and increased unemployment benefit payments) was huge as you can see in the following graph.

Second, given the US issues its own currency, the bond markets were never in a position to push yields up even though the US government matched that increase in net spending with debt issuance. The joint operations of the Federal Treasury and the Federal Reserve Bank (central bank) kept bond yields down to very low and stable levels.

There was never question of the government running out of funds despite all the debt ceiling hysteria which was just a demonstration by the Tea Party idiots of their lack of spine – all talk and no action when the crunch came.

The bond markets were told categorically by the central bank that it had unlimited funds to buy public debt and could create those funds out of thin air.

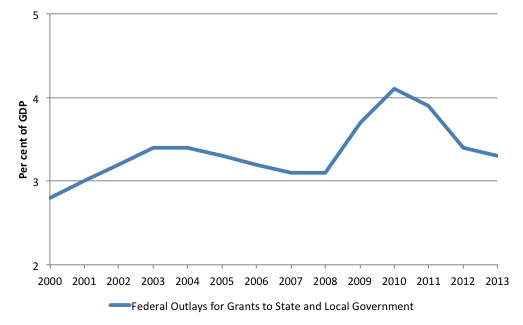

Third, the federal stimulus was not limited to its own expenditure. It also dramatically increased grants to the State and Local Governments. The next graph shows the Total Federal Outlays for Grants to State and Local Governments in the US as a percent of GDP.

That big spike in 2010 is what properly constructed federations can do when the federal fiscal capacity takes responsibility and seeks to redress regional variations in economic outcomes.

There were major handouts to the States and Local Governments to individuals and also capital investment programs.

Clearly not sufficient to prevent the severe recession and the States themselves cut back heavily. But things would have been much worse without those transfers between levels of government.

Conclusion

Dr Sinn steadfastly refuses to accept the need for a federal fiscal capacity in the Eurozone, which would act like the US Treasury and ensure that asymmetric spending collapses across the Eurozone space would be addressed with federal transfers.

He doesn’t want to emulate the US federal system only parts of it.

If he truly wanted to emulate the US system then there would be a major federal fiscal function created as the responsibility of the European Parliament (being the only elected body that spans all the Eurozone nations.

It would stand ready to transfer massive amounts of euros to beleagured Member States, who had surrendered their currency-issuing capacity when they joined the monetary union.

Those transfers would likely create sufficient economic activity at the state-level that state bankruptcies would be unthinkable.

That is enough for today!

(c) Copyright 2014 BIll Mitchell. All Rights Reserved.

Bill,

I’m just wondering what it was like talking to these characters face to face? Do you think they really believe what they are saying? Surely they must be more intelligent than that!

Or are they acting in a way they feel others may wish them to?

Peter

Peter,

Most of these clowns are intelligent only if intelligence is a measure of how well one can regurgititate the mumblings of others idiots.

Compliance and learning by rote are unfortunately more valued in our so called society, than critical thinking.

And given that following the ruling majority is a lot easier than opposing them it’s little wonder clowns like Hans-Werner Sinn exist.

I can think of no reasonable man or rational argument for remaining in the currency union after a diktat such as this?

Dr. Sinn is arbitrarily allocating responsibilities to EMU members that are beyond their control, then, leaving them to the discretion of the wolves.

What does he think would be the result in this sort of madness ….. Greece would be purchased by Google in administration?

“Greece would be purchased by Google in administration?”

Once TTIP is in place, that is very likely – given that no government could then override the undemocratic will of global corporations.

This is not going to end well, and nobody is listening to sense any more.

Completely agree. If Sinn is representative of the German and EU approach, and there’s fair evidence to suggest that he is, then there is no way known that the Euro project can be supported and sustained. It was a bad idea in 1999, it fell at the first hurdle, and has been unable to recover because of its rigid and stupid structure (which applies to ‘elites’ as well).

All roads in a dumbass currency union like this lead to the strongest economy, and now look what’s happening to Germany. It will take an almighty catastrophe there to wake these people up to take advantage of exceptionally low rates to add demand (which still hasn’t been tried, and which QE does nothing to support either – it’s a bank-saver, that’s all). The alternative is for countries to leave and become truly sovereign again.

The peripherals were thrown to the wolves because they were too small to matter to the core for anything other than pillaging (as debt relief was tied to exports). What a great plan for a supposed union. And now that the no.2 economy, along with Italy, are determined to ignore the preposterous impost on their ability to avert depression by adding some discretionary demand through their budgets, the whole mess is fraying further. Some nitwit on Twitter keeps exhorting to buy French bonds … clearly missed 2011 somehow. That is an accident waiting to happen, because the Troika are hardly going to be sympathetic (even in their Keystone Cops fashion) to a country looking for assistance with funding without compromise as yields soar.

I don’t agree about Google because even they couldn’t afford the huge value of the internal Greek assets – property & land being just two. That’s what default is for, which they should have explored while exiting the Euro, rather than punish citizens and lock in depression. But then, the governments there have always been hopeless, so what can we realistically expect?

Other than that, no strong opinion, lol.

Dear Bill,

Werner-Sinn cannot be out of his mind so there must be an agenda and an interest group which he is not making explicit that he is defending. The settlement in gold is so ridiculous that it’s hard to understand where it all went very wrong in his train of thought. I used to comment on his Project Syndicate articles but gave up, his arguments on TARGET2 balances were pretty much demolished by Karl Whelan (I happened to be re-reading his articles last night) and this presentation was really good (http://www.karlwhelan.com/Presentations/Whelan-BoE.pdf).

With intellectual backing like this it is hard to find a solution to the Eurozone that does not involve break up.

Regards

Javier

I am not against him heading some German policy framework if he can bring down the euro.

Wheres the harm in that ?

I have been looking back at Irish trade figures recently (1930 to present)

We were only ever in trade surplus during the hard hard years of the war 1942,43 and 44.

It took the euro system and not the war to drive us into chronic surplus in the search for scarce money.(thus burning up a huge amount of real resources in this strange mercantile quest.)

After the first euro depression of the early / mid 80s we started to post a real goods surplus after Y1985 and went exponential after that.

There was a decline in the surplus during the early to mid 00s but this was a result of corporate conduit like consumption rather then a return to human scale purchasing power.

In 2010 we posted our biggest surplus ever at nearly 44billion euros.

Now we seem to be on the cusp of repeating the “mistakes” of the early 00s as the nature of the internal consumption is highly skewed to ever more consumer war goods.

Sinn is wrong of course – we live inside a strange euro oscillation of devastating capital allocation.

It is no accident.

It is caused by a extreme form of real purchasing power subtraction that has been the characteristic of the euro system since the 70s.

When people have been subtracted from the equation all that remains is the dumping of consumer war goods into societies that no longer exist.

PS

Bill is of course correct about Irish cultural compliance.

If you read the correspondence betwwen Jack Lynch (Irish PM) and Edward heath during the 70s it is very much like a schoolboy /teacher relationship.

A cringeworthy episoide if ever there was one.

Dr. Mitchell/students/A CHALLENGE: To my knowledge-no where is the below on the table in seeking a solution to pervasive unemployment throughout the OECD, and yet, it is both common sense as well as a “law” [albeit unwritten] which would take a major step towards ending our unemployment crisis if adopted by the market-and where unemployment has a profound adverse effect on the market, as well as the jobless. According, I would appreciate evidence which would disprove the following, or if none exists, via research a refinement of the percent presented, if needed….Highest regards, Jim Green

THE LAW OF DIMINISHING INCOME TO THE MARKET RESULTING FROM UNEMPLOYMENT

The law of diminishing income to the Market, as a result of unemployment, starts with the loss in income from even one person [Source: common sense]…and grows exponentially with each percentage point increase in the unemployment rate-with the result that 3% is the zero-sum threshold above which there is a substantial loss in income to the market, and compounded by: Unemployment triggers inflation by diminishing labor training and skills, under-utilizing capital resources, reducing the rate of productivity advance, increasing unit labor costs, and reducing the general supply of goods and services–and the loss in income to the Market is compounded exponentially with each percentage point of increase in unemployment, above 3%.

Jim Green, Democrat candidate for Congress, Dist 21, Texas, 2000 jgreen5@satx.rr.com

http://www.Inclusivism.org

The more I study macroeconomics, the more I’m convinced that it is simply not within the ability of some people to conceive of what the macro is. People who find comfort in hierarchy and chaos in relativity not only cannot understand macro, but are also incapable of understanding that they can’t. It is as if a person who had lived his entire life in a two-dimensional world were suddenly asked to think in three dimensions. Not only would he not be able to do it, but he would likely consider the idea of doing so to be ridiculous to boot.

The irony of Sinn’s views goes beyond even the fact that he ignores the large ongoing fiscal role of the U.S. federal government in sustaining state finances, and the purchasing power of residents in those states hardest hit by recession.

Even more telling, in a way, is his ignorance of the role of the Assumption Act of 1790 in preserving the fledgling union of the states under its then-new Constitution. That Act federalized the war debts of the several states, making them the liability of the new federal government, and it did so without requiring austerity from the more-indebted states.

The arugments put forth against the Act by the southern (and especially the Virginia) representatives, led by Madison, are uncannily echoed in what we hear today from the likes of Sinn and his austerian fellow travelers: assumption of state debts by the federal government would prove an unjust burden to the more ‘prudent’ states, would set a ruinous example of public profligacy, and (much more accurately) would over time greatly strengthen the role of the federal government.

Had Jefferson not prevailed upon Madison and Hamilton, the Act’s champion, to compromise, and had they not done so, and gotten their followers to do so, thereby passing the Assumption Act in exchange for locating the new capital in the vicinity of the agrarian states, the union might not have survived.

In the event, the assumption of the state war debts by the federal government not only failed to prove ruinous to the ‘prudent’ states, it allowed the union to overcome its first great political crisis, and to prosper economically exactly as Hamilton had predicted. It also became a basis for a tradition of inter-sectional (inter-regional) compromise that was followed, largely successfully, for 70 years–until the South violently broke with that tradition, over its claimed right to continue the expansion of slavery ‘unmolested’ by federal authority.

For Sinn to ignore the Assumption Act, and its clear lesson for contemporary Europe’s own fledgling political-economic union, is to completely misconstrue the very foundation of the American economic unity he imagines himself to be extolling.

The sun is rotating around the earth, how can you not see it?!

What did you expect? Mr. Sinn and his crude theories are well known here in Germany, the few progressive german economists and journalists have long been labelling hit work as “Un-Sinn” (nonsense, literally). He has written quite a few gems that would be absolutely hilarious as a parody on economic theory if he wasn´t serious about them.

But he´s done me quite a favour as a student of economics by hitting me in the face with his blatant, unveiled nonsense, quite the eye-opener. 😉

So you want fiscal transfers and mutual debt? OK, then let´s a civil war first and wait a few hundred years like they did in the US!

Dear Sound-Money (at 2014/11/04 at 19:10)

Do you think Germany is that backward?

best wishes

bill

Thoughts on Sinn’s May 29, 2015 piece on Varoufakis?

http://www.project-syndicate.org/commentary/varoufakis-ecb-grexit-threat-by-hans-werner-sinn-2015-05