I have received several E-mails over the last few weeks that suggest that the economics…

With idle labour equal to 14.5 per cent, the fiscal deficit is too low

The fiscal position of a government that issues its own currency should never be a focus of attention other than to understand why it have evolved to its current level – whether it is reflecting mainly discretionary policy choices or cyclical effects (automatic stabilisers). If there was accelerating inflation and high GDP growth then one might be tempted to conclude the fiscal deficit is to expansionary and needs to be cut back. One might equally conclude that private spending is too strong and needs to be cut back. But when there is declining growth and very high and persistent labour underutilisation rates, it is hard to argue that the fiscal deficit needs to be cut. It is, in fact, lunacy!

Here are some facts that should disturb any journalist who thinks Australia has to ‘fix’ the fiscal deficit:

- Real GDP growth is well below its recent trends (before the GFC).

- With trend productivity growth averaging around 1.5 per cent per year and trend labour force growth averaging around 1.7 per cent per year, GDP growth has to be around 3.2 per cent if unemployment rates are to remain unchanged. Real GDP growth is currently stumbling in the low 2 per cents and it is no surprise that unemployment is rising.

- Unemployment and underemployment are around 14.5 per cent of the available working age population in Australia.

- Labour force participation rates are well below their peaks.

- The employment-population ratio has started to decline.

- Private investment is falling and firms have signalled that in 2016 they will cut capital formation significantly.

- Australia runs a current account deficit of upwards of 4 per cent of GDP.

- Australian households are carrying near-record levels of debt and the saving ratio is now around 10 per cent (up from negative values before the GFC).

Taken together, this data tells me that the fiscal deficit in Australia is well below what a responsible government should aspire to provide the Australian economy.

I say provide in the sense that a fiscal deficit provides spending support to Australian businesses which allows them to employ people. If the current spending patterns of the non-government sector is delivering the sort of outcomes articulated in the list above, then we know that the fiscal support to the economy is inadequate.

After we acknowledge that point then we can have a discussion about what the composition of the fiscal deficit should look like – that is, how much government consumption and investment spending there should be.

We might believe that a large-scale investment program in building public infrastructure (for example, to rid us of this antiquated broadband system we have) is warranted – and there is certainly a case to be made in that regard.

We might also think that providing schools with better quality teaching materials and increasing welfare payments would be beneficial – which would see a rise in the recurrent spending (consumption) of government.

But given the state of the Australian economy, it is inconceivable that anyone who really understood the macroeconomics and was wanting to comment on those economics rather than make an ideological/political statement would suggest the fiscal deficit is too large and needs to be pushed back into surplus.

Thinks about it for a second. With an external deficit which is not going to be eliminated in the distant future, income generated in Australia is being lost, in net terms, to foreigners and not being recycled back into the domestic economy to support that on-going income (output) generation.

That state allows us to enjoy all sorts of imported goods and services over and above what, in real terms, we have to send to other nations in return. So the income drain from the external deficit works in our favour – in real terms.

So the spending injections that are required to offset that external spending drain have to come from the private domestic economy and/or the government fiscal deficit (spending greater than taxation revenue).

In the – Statement 2: Economic Outlook – published by the Government in May 2015, the external deficit for 2015-15 was forecast to be 3.5 per cent of GDP. I think that will turn out to be optimistic given the June-quarter data is already indicating an external deficit well above that level.

The – Statement 3: Fiscal Strategy and Outlook – forecast a fiscal deficit of 2 per cent of GDP down from 2.5 per cent in 2014-15. I think that will be an understatement but lets work with that.

So at current national income levels, the private domestic sector is expected to be in deficit over 2015-16 of 1.5 per cent of GDP, given the sectoral balances relationship that holds within the national accounts.

With households carrying near-record levels of debt, there is not a major appetite for more leveraging in that sector. At present the massive debt levels in the household sector are not causing major insolvencies because interest rates are very low.

The business sector is also not likely to be ramping up capital expenditure in the next year to the levels sufficient to lift the growth rate back towards the level required to eat into the massive stock of labour underutilisation.

So given the external drain on spending, the only reasonable assessment is that the fiscal support is inadequate at present and that means the fiscal deficit has to rise.

I typically think that the Fairfax journalist Peter Martin writes about interesting topics. I know Peter personally and think he is a decent chap.

But sometimes, especially when he discusses fiscal matters he loses track.

He became lost in this article (November 3, 2015) – Turnbull should split the budget in two.

Turnbull is the new Prime Minister in Australia and took office after he was part of an internal government coup to get rid of the hapless and hopeless Tony Abbott a month or so ago.

We have replaced a dumb hard-line neo-liberal with a smarter, softer neo-liberal. But a neo-liberal nonetheless!

The Fairfax article’s basic point is that the fiscal position is in bad shape (whatever that means) and:

… keeps getting worse. Interest payments on debt will cost $11.6 billion this financial year … Unless we find an escape hatch, debt payments will one day cost as much as defence or education – especially when interest rates rise. Our budget will be so weighed down with debt payments there will be no easy way to get back to surplus …

The budget deficit has to be brought down …

Turnbull is in a position to create a credible sense of urgency. Unless he does, and unless he does it in the December budget update, the deficit will become harder and harder to fix.

And more of that sort of stuff.

Cars sometime need ‘fixing’ because the bearings wear out or something else ceases to function. People need medical attention to ‘fix’ problems because we are biological and skeletal entities that get sick or wear out.

But there is no meaning to the language that a fiscal balance “keeps getting worse” or “will become harder and harder to fix”.

That’s the worst of the neo-liberal framing and metaphor that you will find in the public debate. It invokes an association with things we understand can become dysfunctional or stop working because they are sick and need ‘fixing’ and the fiscal policy accounts of a currency-issuing government.

The metaphorical association is very powerful because we are dopes and use our own experiences as if they are applicable knowledge to other matters where the personal experience has not application.

The Fairfax article just asserts that there is something wrong with the fiscal position of the government – that is, the fiscal deficit is too high – and a surplus is desirable.

The only weak justification for the statement is that the income flows from the bond interest are rising. Yes but so what?

There is no context provided to argue that a lower fiscal deficit is warranted in the context.

He talks about the need to lift productivity and redistribute income away from “high earners” who enjoy ridiculous tax concessions courtesy of years of conservative governments (on both sides of politics).

But in all of that he acknowledges that:

… fixing the budget won’t allow Turnbull to give the economy a boost by investing in infrastructure.

No, if by ‘fixing’ he means trying to reduce government support for total spending, the effect will be to push Australia into recession and worsen the prospects for private investment.

So his argument is to engage in some trickery and split the fiscal accounts into current and capital and pretend that this makes a difference.

This is the ‘golden rule’ logic which I have discussed in several blogs – most recently in – The non-austerity British Labour party and reality – Part 2.

It is really about creating smokescreens.

Peter Martin acknowleged that the Australian government is now borrowing long-term at low rates and:

… could separate “recurrent” spending and the income needed to fund it, from “capital” spending and the borrowing used to fund it. That way, he could borrow big for demonstrably worthwhile projects while at the same time tightening the recurrent budget.

How that squares with his concern for interest income one day being as “much as defence or education” is a puzzle.

But it doesn’t overcome the problem that however you compose the fiscal position, the net result has to fill the non-government spending gap or else the economy will slow and unemployment will rise.

Placing artificial restrictions on what the government can deficit spend on is just another way of reducing the effectiveness of the fiscal policy to maintain full employment.

While Peter Martin talks about preserving credit ratings the data doesn’t suggest that there is the slightest problem. I am not suggesting that the Australian government should worry about credit rating agencies at all. They are largely irrelevant. But even within the orthodox logic there are quite amazing things happening in Australian bond markets at present.

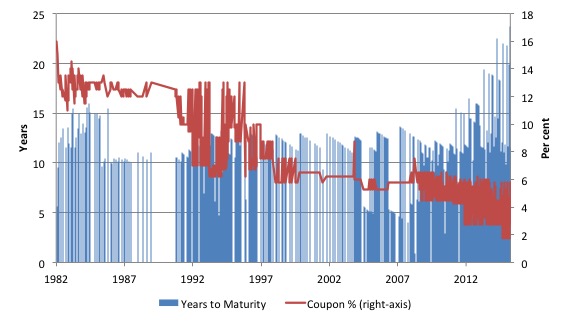

In the last few years, the Australian government, through its debt management agency the Australian Office of Financial Management, has been issuing increasingly longer debt instruments at lower coupon yields. You can get the data for all Treasury Bond tenders since 1984 – HERE.

The AOFM tell us that:

Treasury Bonds are medium to long-term debt securities that carry an annual rate of interest fixed over the life of the security, payable six monthly.

They are issued by tender at auctions held each Wednesday and Friday (at present).

The following graph shows the history of the Treasury Bonds tender in terms of the maturity length of the bonds issued at each tender (left-hand axis in years) and the Coupon % for each issue (that is, the annual rate of interest paid to the bond holder until maturity.

It is a rather interesting graph. The obvious points are that the length of Treasury bonds offered is getting longer and the yields are getting lower.

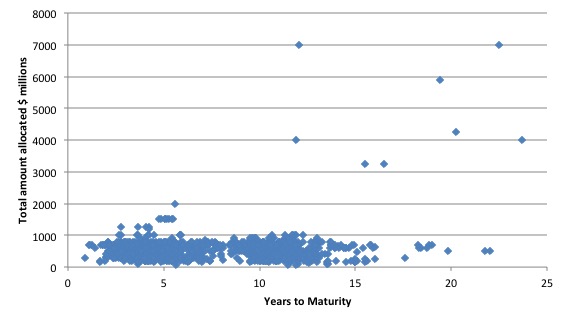

The next graph relates the total amount of the bond issue at each tender in $A millions to the years to maturity of each issue.

The total amount amount of these long maturity issues is much larger than it is for the shorter-duration Treasury Bond issues.

The other point to note is that the so-called ‘coverage ratio’ remains high.

The ‘bid-to-cover’ or ‘coverage’ ratio is just the the $ volume of the bids received to the total $ volumes desired. So if the government wanted to place $20 million of debt and there were bids of $40 million in the markets then the bid-to-cover ratio would be 2.

First, the use of the ratio assumes it matters. It doesn’t matter because the Australian Government is not revenue-constrained so it could just abandon the auction system whenever it wanted to if the ratio fell to 0.00001.

Second, it is highly interpretative as to what the ratio signals. It certainly signals strength of demand for the specific bond instrument being auctioned. But how ‘strong’ becomes an emotional/ideological/political matter. Even if you believed that the government was financing its net spending by borrowing, then a bid-to-cover ratio of one would be fine – enough lenders to cover the issue. Some commentators think that 2 is a magic line below which disaster is imminent. There is no basis at all for that.

There is also no basis in the statement that a ratio above 3 is successful and by implication a ratio below 3 is unsuccessful. After all, anything above 1 tells you that some investors do not get their desired portfolio (their tender rates are above the final market yield determined at the auction). That sounds like a failure to me.

On October 14, 2015, for example, the AOFM issued a 23.7 year long bond (maturing on June 21, 2039) at a Coupon % of 3.25 per cent. That sort of pricing has been on offer for these very long bond issues for more than a year now and the Coupon is dropping as the months pass.

The total amount of the bond issue was $A4000 million

This means that for the next 23.7 years, the $A4000 million the government swapped with the non-government sector in exchange for a promise to pay 3.25 per cent per annum over that time is fixed whatever happens in secondary markets when speculative trading of this particular issue takes place.

So if the fiscal deficit was such a problem why would the non-government sector be prepared to park its savings for 23.7 years in a different ‘bank account’ at the central bank – which is effectively all a Treasury Bond is – and only receive 3.25 per cent per annum over that period, especially with inflation running around 2 per cent?

I should add that this whole process – whereby the Australian government provides this level of corporate welfare to the bond markets – is totally unnecessary. The Australian government could just simply ask its central bank – the Reserve Bank of Australia – to credit various bank accounts without having the accounting hoopla that puts numbers in a special bond account and then transfers these numbers into a government spending account.

The Government, after all, issues the currency that it then borrows back from the non-government sector after the government has previously spent it into existence. It is a very curious set of accounting restrictions that governments voluntarily place on themselves.

Why would anyone want to loan the Australian government cash at little or no real return? Especially if there is a fiscal crisis that needs to be ‘fixed’.

That answer is that the Australian government debt is risk free and the bond markets are scared of the likely impacts of austerity (and think that the deflationary bias that has hit world economies will persist). They clearly also don’t buy into the fiscal emergency hysteria promoted by the conservatives.

While the result is rather amazing it begs the question – why does the Australian government borrow at all?

There is no financial requirement for the Australian government to issue debt because it is empowered through the RBA to issue the Australian dollar at will, floats the exchange rate and doesn’t back the currency with any commodity (such as gold or silver).

Further, a sovereign government with a floating currency can issue securities at any rate it desires. The central bank can always control the yields that the government desires by ensuring it uses its powers to purchase sufficient government debt to achieve that purpose.

It is simply false reasoning to claim that there is an inevitable link between the size of a sovereign government deficit and the interest rate paid on the bonds it issues.

Continuous fiscal deficits are normal

The obsession with getting back into fiscal surplus denies history.

There is the notion in the public sphere, promoted by a few decades of neo-liberal hectoring, that continuous deficits are somehow abnormal or bad. The public now think – that responsible governments ‘balance their budgets over the business cycle’.

Where did anyone get that idea from other than ideologically-laden mainstream macroeconomic textbooks that our students forced to use?

The reality is that fiscal deficits have been the norm over any of the successive business cycles. There is no evidence that Australian governments ‘balance budgets’ over the cycle.

The further evidence is that as the neo-liberal persuasion has become dominant in macroeconomic policy, Australian governments have attempted to run discretionary surpluses. The outcomes of this behaviour have not been good and overall this period (since around the mid-1970s) have been associated with lower average real GDP growth and more than double the average unemployment rate.

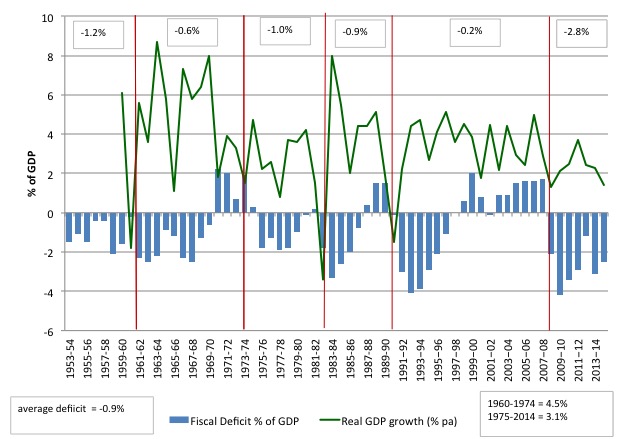

The following graph is based on historical data which is explained in this blog – Australian fiscal statement – attacks the weakest and will undermine prosperity overall.

The graph below is a reasonably reliable depiction to the history of Federal government fiscal outcomes outcomes over the period – 1953-54 to 2014-15.

The columns show the Federal fiscal balance as a per cent of GDP (negative denoting deficits) while the green line shows the average quarterly real GDP growth (averaged over the financial year at June).

The red vertical lines denote the trough of the respective business cycles. So the real GDP growth line approximates where in the year the negative real GDP growth manifested. But for our purposes it is near enough.

The upper numbers in boxes are the average deficits over each cyclical periods. The average deficit over the whole period was 0.9 per cent of GDP. The average real GDP growth per quarter from 1959-60 was 1.2 per cent and after 1975 this dropped to 0.8 per cent. The unemployment rate averaged below 2.0 per cent in the pre-1975 period and averaged around 5.5 per cent after 1975.

The 1975 Budget was a historical document because it was the first time the Federal Government began to articulate the neo-liberal argument that fiscal deficits should be avoided if possible and surpluses were the exemplar of fiscal responsibility.

Please read my blog – Tracing the origins of the fetish against deficits in Australia – for more discussion on this point.

Some points to note:

1. One the rare occasions the fiscal balance was pushed into surplus (usually by discretionary intent of the Government) a major recession followed soon after. The association is not coincidental and reflects the cumulative impact of the fiscal drag (that is, the surpluses draining private purchasing power) interacting with collapsing private spending.

2. There is no notion over this period that the fiscal outcome was ‘balanced’ over the business cycle. The historical reality is that the federal government is usually in deficit. If I had have assembled more historical data which is available in the individual budget papers going back to the 1930s then it would have just reinforced the reality that surpluses have been rare in our history independent of the monetary system operating (the old convertible system or today’s non-convertible system).

3. The Australian federal government ran fiscal deficits of varying sizes in 75 per cent of the years between 1953-54 and 2014-15 (46 out of the 61 years).

4. The fact that the conservatives were able to run surpluses for 10 out of 11 consecutive years (1996 to 2007) is often held out as a practical demonstration of how a disciplined government can run down public debt and provide scope for private activity. The reality is that during this period we have witnessed a record build-up in private indebtedness (see below).

The only way the economy was able to grow relatively strongly during this period was that private spending financed by increasing credit growth was strong. This growth strategy was never going to be sustainable and the financial crisis was the manifestation of that credit binge exploding and bringing the real economy down with it.

5. The higher deficits in the recent period is testament to the fiscal stimulus package and, perversely, the fiscal contraction that followed. Remember this is a ratio of the fiscal balance to GDP. So if the numerator (fiscal balance) goes up faster than the denominator (GDP) then the ratio rises and vice-versa. But if the denominator falls more quickly than the numerator (at a time of fiscal austerity) the ratio can also rise. The previous government cut hard in their second last fiscal statement and that caused the economy to slow.

Conclusion

The fiscal position of a government that issues its own currency should not be a focus of attention other than to understand why it have evolved to its current level – whether it is reflecting mainly discretionary policy choices or cyclical effects (automatic stabilisers).

If there was accelerating inflation and high GDP growth then one might be tempted to conclude the fiscal deficit is to expansionary and needs to be cut back. One might equally conclude that private spending is too strong and needs to be cut back.

But when there is declining growth and very high and persistent labour underutilisation rates, it is hard to argue that the fiscal deficit needs to be cut. It is, in fact, lunacy!

That is enough for today!

(c) Copyright 2015 William Mitchell. All Rights Reserved.

Excellent post as always. However this statement:

“If there was accelerating inflation and high GDP growth then one might be tempted to conclude the fiscal deficit is to expansionary and needs to be cut back. One might equally conclude that private spending is too strong and needs to be cut back.” ….could be made basically irrelevant by the macro-economic policy tools of a universal dividend and a discount to retail prices to the individual (in other words everyone) that was rebated back to retailers so that they could be whole on their margins and overheads and the system, which would also include all of the excellent insights of MMT, would fit seamlessly within profit making systems which actually served the individual.

I have posted here before about these macro policies and about the fact that retail sale to the individual is the key policy target because it is the terminal end of all costs for any item or service as well as the terminal end of the entire productive process itself. A couple of posters here declared that these policies would not stabilize or bracket the entire economy, but they gave no actual or valid reasons why they believed that to be true.

I’m not here to invalidate MMT in any way, I’m only interested in integrating it with other reform movements like Public Banking and Social Credit thinking that such integration would bring a greater clarity and hope to a mass movement whose lay, economic and political constituency might actually get such an integrated and hence complete program actually enacted.

Strong post Bill, very illuminating.

You asked the question, “Why does the Australian Government borrow at all ? ”

I have asked myself the very same as I have read your work over the last few months, and as yet have not come to a satisfactory answer…. Would you or any of your regular contributors care to share your opinion ?

Dear Bill

As you know of course, the current account contains more items than the trade account. Part of Australia’s current-account deficit must be due to remittances and investment income. Australia is home to many immigrants from poorer countries, and they send money to their relatives. Australia has a negative international investment position of over 900 billion. That should mean that more investment income leaves than enters Australia.

“Continuous fiscal deficits” is not something that scares your readers, but it is something that scares most people. The reaction of nearly everybody will be: “Continuous fiscal deficits are unsustainable. Today’s fiscal deficits are tomorrow’s tax increases”. As usual, the conventional wisdom is against you.

At least part of the decline in the employment/population ratio must be due to aging. I know that aging is often accompanied by “üngreening”, as the Dutch call it. Still the increase of the share of the Australian population that is 65 or older must be larger than the decrease of the share of the Australian population that is 14 or younger because a lot of ungreening already occurred much earlier. It is because ungreening precedes aging that countries can enjoy a demographic dividend.

Regards. James

Dear James (at 2015/11/03 at 16:11)

You might like to read this blog – https://billmitchell.org/blog/?p=29140

best wishes

bill

Steve,

Do you have reading recommendations for learning more about public banking and social credit?

Dear Robert (at 2015/11/03 at 19:46)

I would prefer not to have to conversation about “public banking and social credit” here please? This is not the place.

best wishes

bill

“Why does the Australian Government borrow at all ? ”

The question is somewhat philisophical. Issuing money is creating liability and creating liabilities is borrowing just like issuing debt. Perhaps it helps to frame the issue in a right direction, but other than paying interest to the rentiers, the question is meaningless IMO to an MMT oriented person. There might be a political will to create income to seniors or something similar. I think the real issue is fear mongering: debt is too big, our children willl have to suffer etc.

Dear Bill and others

Government debts are assets of the private sector in a closed economy. In an open economy, those assets could of course also belong to the foreign sector. Here is something that isn’t quite clear to me. If the government “borrows” directly from the central bank, then government debt can no longer be an asset of the private sector. Where then will the savings of the private sector, which formerly went into government bonds, go now?

There is something else that baffles me. Let’s take a closed economy in which G =T and in which households save nothing. Firms can still invest with borrowed money since banks don’t need savings to lend. How will S become equal to I. By assumption, X = 0, M = 0 and G =T. So, S must be equal to I. How does that occur since households do not save?

Thanks. James

“Why does the Australian Government borrow at all ? ”

Actually, it doesn’t. You can’t borrow your own debt. When you attempt to, you don’t incur a liability for the “borrowed” money, as you already incurred that liability when you created the money itself.

Let’s create a simple example. You offer your son ten dollars to mow the lawn. He does, and you write him a ten dollar IOU. The IOU is your “money”.

You now decide to share a ten dollar pizza with your son, but you don’t have any money. You ask your son if you can borrow ten dollars from him, and he gives you the ten dollar IOU, for which you give him a second ten dollar IOU.

At the end of all of this, you owe your son ten dollars, and you have nothing to give to the pizza delivery guy when he gets there. Borrowing your own debt got you nowhere.

James Schipper: Here is something that isn’t quite clear to me. If the government “borrows” directly from the central bank, then government debt can no longer be an asset of the private sector. Where then will the savings of the private sector, which formerly went into government bonds, go now?

On the consolidated gov+cb perspective, this is identical to the government/cb just “printing/spending” money. This money, bank reserves, folding money, coins etc is then the NFA, the government debt that the private sector as a whole is saving. The point is to conflate government bonds and other forms of government debt like treasury or central bank notes or reserves. Not conflating, making imaginary, unintelligible distinctions without a difference is at least as important a source of obscurity these days as conflating genuinely, essentially different things.

Kristjan and Benedict@Large,

Your points above are standard MMT arguments which are theoretically valid only for a closed economy.

They do not apply to the extent that government debt is owed to foreigners.

About 66% of Australian government securities are held by non-residents.

See: http://aofm.gov.au/statistics/non-resident-holdings/

Dear Kingsley Lewis (at 2015/11/04 at 14:11)

Who owns the debt issued in Australian dollars is rather irrelevant. Yes, the foreign holders have claims on resources that are available for sale in Australian dollars as a result of purchasing a guaranteed $A income stream.

But that doesn’t alter the fact that the Australian government is always able to meet these liabilities. They do not have to accumulate any foreign currencies to retain the capacity and all exchange rate risk is borne by the bond holder (should they wish to convert back into their own currencies on maturity).

best wishes

bill

I think your discussion bonds actually understated how little the government really pays in interest. You talk about the Coupon Rate as being as the interest cost of the debt but this is slightly incorrect. It would imply there is no cost to issuing zero coupon bonds. The coupon rate is the rate of interest paid on the face value of the bond but not the interest as a percentage of the price received for the bonds at issuance. The price received for the bonds will be different to the face value so long as the yield to maturity is different from the coupon rate. The yield to maturity is a better indication of the “interest” cost (although calling it an interest cost can be slightly misleading given that some of cost can come from the face value being greater than the price received for the bond) as it reflects the return to investors which must be equal to the cost to the government for issuing the bonds (if the cost isn’t equal to the return where does the return come from). Given that the government bonds actually have a yield to maturity lower than the coupon rate, you could have made your argument stronger by discussing the cost of debt in terms of yield to maturity rather than coupon rates.