Edward Elgar, my sometime publisher, is interested in me updating my 2015 book - Eurozone…

Iceland proves the nation state is alive and well

On May 27, 2016, Statistics Iceland (the national statistical agency) released the news – Iceland economy to grow by 4.3% in 2016. The nation is enjoying strong household consumption and investment growth and tourism is driving export growth. Inflation is low and the exchange rate, which depreciated sharply during the crisis, is stable, if not steadily appreciating again. Compare that to the Eurozone Member States, which are in varying states of moribund. We also learned this week that the Icelandic government has increased the intensity of its capital controls and is forcing speculative capital to behave itself. For those who think the state is dead, particularly those on the Left who promote grand (delusional) schemes of a Pan Europe Democracy as the only way of taking on the powers of corporations, Iceland proves that neo-liberalism has to work through the legislative capacities of sovereign states. Corporations do not have armies (usually). They have to manipulate the legislative process in their favour. The currency-issuing state is still supreme – globalisation or not – and the Right know that. The Left have been duped into believing otherwise. That is what has to change before progress is made in restoring some decency to the policy making process around the world.

You can read all about the capital controls policy prevailing in Iceland at present via the Central Bank’s – Capital Accounts Liberalisation Strategy page.

See also – A tale of two economies – Greece and Iceland and Are capital controls the answer? – for further discussion about Iceland.

Further, recent revelations coming out of the IMF demonstrate what a schizoid organisation it is becoming as its hard-core neo-liberal ideology keeps coming up against the brick wall of reality.

The June 2016 (Vol 53, No.2) edition of its in-house journal Finance and Development carried an article – Neoliberalism: Oversold? – which has been attracting attention across the media since it was pre-released last week.

In that article, the IMF authors (who did the earlier research on capital controls referred to above) basically eschewed the notion that self-regulating markets – the catchcry of the free market lobby – deliver optimal outcomes.

They define neo-liberalism as resting “on two main planks”:

The first is increased competition-achieved through deregulation and the opening up of domestic markets, including financial markets, to foreign competition. The second is a smaller role for the state, achieved through privatization and limits on the ability of governments to run fiscal deficits and accumulate debt.

The sort of policies the IMF has been inflicting at great damage for four decades on poor nations and more recently on advanced nations such as Greece.

Now, the IMF authors admit that “the neoliberal agenda … [has] not delivered as expected”, particularly in the area of free capital flows and “austerity” (aka “fiscal consolidation”).

They now reach “three disquieting conclusions” in relation to this agenda:

– The benefits in terms of increased growth seem fairly difficult to establish when looking at a broad group of countries.

– The costs in terms of increased inequality are prominent. Such costs epitomize the trade-off between the growth and equity effects of some aspects of the neoliberal agenda.

– Increased inequality in turn hurts the level and sustainability of growth. Even if growth is the sole or main purpose of the neoliberal agenda, advocates of that agenda still need to pay attention to the distributional effects.

Rather at odds with the mainstream IMF mantra, one would say!

The upshot of these revelations is that:

1. They question the benefits and purpose of “short-term international capital flows” and conclude that “capital controls are a viable, and sometimes the only, option when the source of an unsustainable credit boom is direct borrowing from abroad”.

2. There is no economic theory about the optimal size of the state despite all the mainstream economists suggesting otherwise – to wit, that a smaller state is better. They just make that up and the statement reflects their ideological bias rather than any authority drawn from theory.

The IMF says that “Austerity policies not only generate substantial welfare costs due to supply-side channels, they also hurt demand-and thus worsen employment and unemployment.”

3. “In sum, the benefits of some policies that are an important part of the neoliberal agenda appear to have been somewhat overplayed.”

Memorise those conclusions and shout them from rooftops and at dinner parties when your smug, so-called progressive left mates start talking about the incapacity of the ‘state’ to defend a nation against global capital flows and preach austerity lite!

The government of Iceland has clearly understood who has the power – them and not global capital!

On May 22, 2016, the Icelandic Parliament approved new “steps toward liberalisation of capital controls in Iceland” (Ministry of Finance Press Release).

The new laws – Bill of Legislation on the treatment of króna-denominated assets subject to special restrictions – provided for new measures for dealing with foreign holdings of around 320 billion worth of króna-denominated assets.

To prevent this cash destabilising the exchange rate when the nation reduces the capital controls, the Government has chosen to “segregate the offshore króna assets in a secure manner so that it will be possible to take the next steps towards lifting the capital controls and re-establishing unrestricted cross-border transactions with krónur.”

The assets in question include “deposits, funds held in custodial accounts, bonds, and bills.”

The Government is giving the asset owners a ‘free choice’ – which the Wall Street Journal article (May 27, 2016) – Iceland Puts Freeze on Foreign Investors – said was tantamount to offering a Hobson’s choice.

The Government says that the “owners may hold these assets until maturity. Therefore, no one is being forced to sell offshore króna assets.”

The króna-denominated asset holders will have two options:

1. They can take the “clear exit path where all owners of offshore króna assets will be ensured an exit at a specified minimum price.”

This will be achieved by a “voluntary” decision before September 1, 2016 to sell their holdings to the central bank at one of the central bank auctions in return for króna, which the central bank will then exchange into euros at an exchange rate of 210 króna per euro. The rate can drop to 190 króna per euro under certain conditions.

The current market rate is 139.22 króna per euro.

So this protects the official exchange rate but still gives the asset holders the choice of exiting the currency.

2. Any funds not exchanged for euro will be forced to invest “in Central Bank of Iceland certificates of deposit” which “do not have a specified maturity date” and will receive an “annual interest rate of 0.5%”.

That is the money is impounded for as long as the government sees fit and receives next to nothing in return.

The new Law demonstrates how a sensible government resists the demands of speculative capital and prioritises the well-being of its own people.

The Minister of Finance said in his press release that the changes “will focus on households and businesses in Iceland”, which is a refreshing alternative to those who always claim that governments have to inflict damage on their people to garner the ‘confidence’ of international capital.

Iceland demonstrates very clearly who is in charge.

Capital controls do not sit well with mainstream economists.

But the controls in Iceland (as in Malaysia in the late 1990s) have certainly helped them stabilise the economy and put it back on a growth footing. The Government is now slowly relaxing the controls as the recovery unfolds.

The conservatives are once again ramping up the argument that foreign investment will dry up, that the government will not be able to fund itself and that the ratings agencies will downgrade public debt and force higher costs onto the government.

I laugh when I read some of the journalistic pieces – in one breath saying that the Icelandic government will not be able to fund itself and the next saying Moody’s will impose higher funding costs onto the government.

The careful decision-making of the Icelandic government has demonstrated that neither is true. It can fund all its domestic programs in króna without recourse to foreign funds. Indeed, it should completely avoid borrowing in foreign currencies.

If the bond markets do not want to invest in Iceland public debt that is their problem – the Government is fully sovereign and can maintain whatever spending program it deems wise in the circumstances.

The central bank governor told the press that their policies would prevent any new waves of speculative capital in the future.

He said of the billions still held up in króna-denominated assets that:

We don’t need the money … These are remnants from the last boom and bust, and we are not going to repeat that mistake.

One of the recurring themes during the Q&A sessions that followed my public presentations in Spain recently related to the future of the Eurozone in 20 or so years given the travesty that the elites are foisting onto their children.

‘Their’ in this context being the ‘royal their’ – clearly their own children are probably safely ensconsed in private schools doing very well with a network of employment opportunities to ease the transition to the labour market.

The point I made on several occasions is that the Euro leadership is severely out of touch with the reality of the situation they have created. What they have now is a disaster on their hands and the costs will linger for generations to come.

An unemployed teenager in Greece or Spain will probably have been unemployed through the entire latter part of their teenage years and have become young adults – with no work experience, limited education and a sense of betrayal.

What is their future and, by definition, the future of their nations looking like? Its gets pretty scary when you think of the legacy that the policy ideology has created.

Iceland is prioritising its youth over the interests of foreign capital. A salutary lesson.

How is Iceland doing then?

Real Wages growing strongly in Iceland

Iceland Statistics reports that Real wages (Nominal wages adjusted for changes in the price of goods and services) initially fell after the crisis and the closure of the banks (by 13.1 per cent between February 2008 and May 2010).

However, once the government intervention stabilised the economy, real wages have grown strongly again and are now (April 2016) 12.8 per cent higher than they were at the peak before the crisis (February 2008).

Compare that the the Eurozone area where real wages overall have only grown by 4.8 between 2000 and 2015. For Greece, real wages have fallen by 14.1 per cent over that period; Spain growth by 6.1 per cent, Italy zero growth and Portugal a decline of 5.1 per cent.

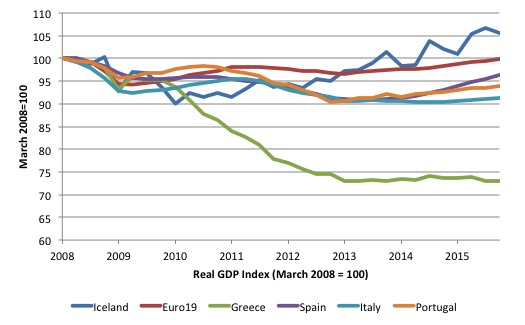

Real GDP has grown strongly since recovery in Iceland

Since returning to growth in the March-quarter 2011, Iceland has sustained positive growth. The outlook is strong with domestic expenditure growth robust, helped along by the growth in real wages.

Tourism has been aided by the lower exchange rate which has boosted exports.

The following graph shows annual real GDP growth since the March-quarter 2008 to the December-quarter 2015. The data for 2016 (not shown) suggests that growth will be stronger this year (estimated at 4.3 per cent) than last year when it averaged 3.9 per cent.

The next graph shows the comparison with the Eurozone nations. The real GDP indexes are set at 100 at the March-quarter 2008 and extended to the December-quarter 2015.

The Eurozone 19 Member States together had still not returned to the March-quarter 2008 peak by the end of last year. Greece was 27.4 per cent smaller, Spain 3 per cent smaller, Italy 8.4 per cent smaller and Portugal 6.2 per cent smaller.

By contrast, Iceland was 5.5 per cent larger than it was at the pre-crisis peak in 2008. It lost 10 per cent of its output by March 2010, and then started its recovery.

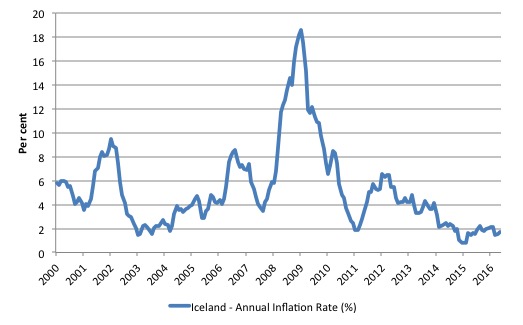

Inflation is low

Inflation experienced a sharp rise in inflation in 2009 as a result of the depreciating currency. But this shock soon dissipated and inflation is now low again.

The following graph shows the annual inflation rate from 2000 to May 2016.

It demonstrates that fears that hyperinflation will follow a currency crisis are ill-founded, as Modern Monetary Theory (MMT) proponents continually aim to reinforce.

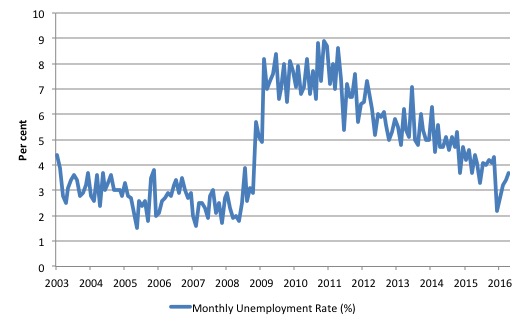

Unemployment is the envy of the world

The following graph shows the official Icelandic monthly unemployment rate from January 2003 to April 2016.

The official Icelandic unemployment rate was 3.7 per cent in April 2016 after peaking at 8.9 per cent in November 2010.

Most of the Eurozone nations would love to have an unemployment rate this low, especially only a few years after a massive collapse of its banking system.

Note also that unemployment has been falling while real wages have been rising strongly – putting paid to the orthodox claims that the latter causes the former to rise!

Private consumption has recovered in the last two years and is driving growth along with Business investment

The National Accounts demonstrate that Gross domestic final expenditure grew by 1.6 per cent in the December-quarter 2015 on the back of strong growth in private final consumption (1.8 per cent growth), private business investment (3.9 per cent growth) and residential construction (11 per cent growth).

Government capital investment in improved infrastructure and services also grew by 6.2 per cent in the December-quarter.

With household spending growth now recovered (and real wages growing strongly to avoid a reliance on credit growth), business firms have an incentive to reinvest in new plant, equipment and buildings.

The strong domestic growth is creating a virtuous cycle of development, something that the Eurozone is incapable of achieving.

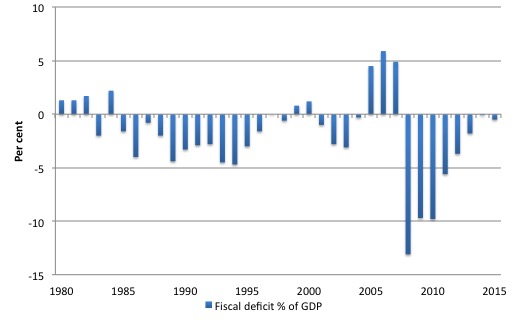

The public deficit supported growth until private domestic expenditure was strong enough

The following graph shows the Fiscal deficit as a percent of GDP from 1980 to 2015. The large deficits in 2008 were in response to the collapse of the economy as the financial sector imploded.

The government didn’t impose large-scale austerity in response but allowed the deficit to support growth as long as it was required to allow private domestic expenditure to recover and take over the growth role.

The deficit is now small relative to GDP.

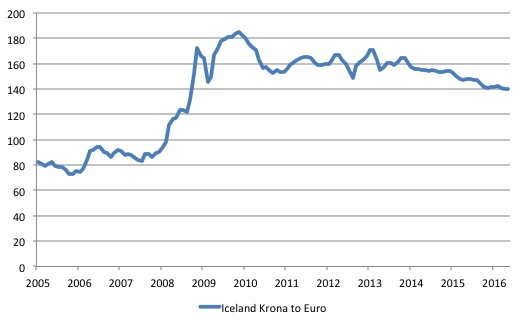

Exchange rate flexibility

The National Accounts also show that exports growth is strong (2.5 per cent in the December-quarter 2015).

The exchange rate depreciation in 2009 was large but finite and the following graph, which shows the exchange rate against the Euro from January 2005 to May 2016 has started a slow appreciation since its low of 184.64 in November 2009.

It has since regained strength on the back of the strengthening domestic economy as stands at 139 or so.

The comparison of these fixed exchange rate euro nations with Iceland is striking.

The fundamental differences between the Eurozone nations and Iceland are threefold:

(a) Iceland issues its own currency while the other nations use a foreign currency;

(b) Iceland enjoys a floating exchange rate; and

(c) Iceland sets its own interest rate.

These are the characteristics that differentiate sovereign from non-sovereign nations in terms of the currency in use.

Iceland has experienced a massive gain in its international competitiveness in recent years with less austerity.

The exchange rate depreciation in Iceland made its exports cheaper and demand for them grew rapidly at the same time as import demand fell because of the rise in prices in the local currency.

The same sort of dynamic assisted Argentina in growing after it allowed its exchange rate to drop significantly in 2002.

Iceland’s real effective exchange rate evened out after its initial plunge. That is a common pattern.

After an initial plunge, the nominal exchange rate stabilises as growth returns.

The scaremongers who claim that the weaker euro nations would experience massive and ongoing currency plunges are in denial of history.

Iceland’s approach to the crisis was less painful and more effective. Greece and other weaker euro nations could have enjoyed similar improvements in their external competitiveness if they had exited the EMU and allowed their currencies to float.

Internal devaluation has clearly not been an effective route to increasing international competitiveness despite all the neo-liberal claims to the contrary.

The costs of such a strategy have been huge in terms of lost output, mass unemployment and social breakdown.

A recurring misconception is that Modern Monetary Theory (MMT), as part of the “Post Keynesian” family should eschew the notion that exchange rate depreciation provides a fillip for exports and discourages imports. Apparently that notion is “neo-classical” and should be abandoned.

All sorts of issues are raised to claim that the current account doesn’t respond to large exchange rate changes. For example, there are apparently: (a) lags in adjustment; (b) dominance of income over substitution (relative price) effects; (c) dominance of capital flows over trade in goods and services etc.

I agree that all these things are part of the real world. Currency prices are largely driven by movements in financial capital in world foreign exchange markets, which reflect speculation (often irrational in its motivation) in the face of uncertainty.

I agree that income effects (the loss or gain of income when a price changes) are stronger, usually, than substitution effects. In this case, a depreciation undermines real income in a nation to the extent that import prices are higher. But there are also boosts to real income if exports improve.

Further, trade adjustments if they occur take time (so-called adjustment curves) and it is entirely possible that following an exchange rate depreciation the current account increases before it decreases due to valuation effects on outstanding contracts etc.

There was a view in the Cambridge model of Godley and Cripps that real wage resistance would eliminate any competitive gains arising from depreciation.

All of the above a acceptable propositions. But they don’t lead to the conclusion that it is strictly a neo-classical view to consider that if something becomes much cheaper then other things equal the volume demand for it will rise over time, and vice-versa. Post Keynesians would accept that proposition just as much as a mainstream economist would accept it.

The other proposition that often gets raised against MMT ideas is that the depreciation will be so severe that it destroys the currency.

Iceland proves the folly of that notion.

Conclusion

The new Law brought in this month by the Icelandic government demonstrates categorically who is in charge!

For those who think the state is dead, particularly those on the Left who promote grand (delusional) schemes of a Pan Europe Democracy as the only way of taking on the powers of corporations, Iceland should proves that neo-liberalism has to work through the legislative capacities of sovereign states.

Corporations do not have armies (usually).

They have to manipulate the legislative process in their favour. The currency-issuing state is still supreme – globalisation or not – and the Right know that. The Left have been duped into believing otherwise.

That is what has to change before progress is made in restoring some decency to the policy making process around the world.

The series so far

This is a further part of a series I am writing as background to my next book on globalisation and the capacities of the nation-state. More instalments will come as the research process unfolds.

The series so far:

1. Friday lay day – The Stability Pact didn’t mean much anyway, did it?

2. European Left face a Dystopia of their own making

3. The Eurozone Groupthink and Denial continues …

4. Mitterrand’s turn to austerity was an ideological choice not an inevitability

5. The origins of the ‘leftist’ failure to oppose austerity

6. The European Project is dead

7. The Italian left should hang their heads in shame

8. On the trail of inflation and the fears of the same ….

9. Globalisation and currency arrangements

10. The co-option of government by transnational organisations

11. The Modigliani controversy – the break with Keynesian thinking

12. The capacity of the state and the open economy – Part 1

13. Is exchange rate depreciation inflationary?

14. Balance of payments constraints

15. Ultimately, real resource availability constrains prosperity

16. The impossibility theorem that beguiles the Left.

17. The British Monetarist infestation.

18. The Monetarism Trap snares the second Wilson Labour Government.

19. The Heath government was not Monetarist – that was left to the Labour Party.

20. Britain and the 1970s oil shocks – the failure of Monetarism.

21. The right-wing counter attack – 1971.

22. British trade unions in the early 1970s.

23. Distributional conflict and inflation – Britain in the early 1970s.

24. Rising urban inequality and segregation and the role of the state.

25. The British Labour Party path to Monetarism.

26. Britain approaches the 1976 currency crisis.

28. The Left confuses globalisation with neo-liberalism and gets lost

29. The metamorphosis of the IMF as a neo-liberal attack dog

30. The Wall Street-US Treasury Complex.

31. The Bacon-Eltis intervention – Britain 1976.

32. British Left reject fiscal strategy – speculation mounts, March 1976

33. The US government view of the 1976 sterling crisis

34. Iceland proves the nation state is alive and well

The blogs in these series should be considered working notes rather than self-contained topics. Ultimately, they will be edited into the final manuscript of my next book due later in 2016.

That is enough for today!

(c) Copyright 2016 William Mitchell. All Rights Reserved.

Sigh if only the Greeks after that Yes vote had taken the Grexit option offered to them they may have a chance over the coming years to prove they can do the same. I fear there is so much “brain drain” from Greece and long suffering that will make it a much longer process and the longer they wait the worse it will be.

When will those fools in the Eurozone wake up? You win again!

Dear Bill

There is no reason anyway why a rich country needs foreign capital. The only reason why a small rich country like Iceland might need foreign capital is that sometimes foreign capital comes together with technical know-how. That is only true in the case of direct green-field investment. The bulk of cross-border investments are not direct green-field investments. If some foreigners take over already existing Icelandic companies, that is direct brown-field investment, why should that be important? Nothing new is added.

Regards. James

Superb explication. Iceland’s “natural” experiment gives the lie to the Euro and UK “natural” experiments whose justifications have been shown to be entirely without foundation, as clearly shown by this post. Indeed, most of their claims have been shown up. The mystery is why the UK and Euro elites still insist on them when it should be obvious that continuing to implement them isn’t even in their own interests. In addition to Groupthink, perhaps another factor, as yet unexplored, that reinforces Groupthink is at work here, and it isn’t and cannot be self-interest.

If Iceland can do it, maybe Greece can too; certainly Spain could. The scarcity of available local resources to develop a self sufficient domestic economy has been mentioned as one reason for Greece being so reluctant to abandoning the monetary union, and for placing their fate in the hands of others. There is a real confidence problem arising from the sense of inability to make a go of things domestically. To believe this is to lose the belief in the ability of the state to remain sovereign.

This does seem an illusion fostered by the neo liberal taint on globalism and the lack spirit of divisiveness that accompanies it.

Iceland should proves that neo-liberalism has to work through the legislative capacities of sovereign states. Bill Mitchell

A major way it does so is through government subsidies for depository institutions.

Why, for example, do we need government-provided deposit insurance when all citizens should be able to use their nation’s fiat the same way the banks do – via convenient, inherently risk-free accounts at the central bank?

Why, for example, isn’t liquidity (new fiat) distributed equally to all citizens if interest rates are deemed too high? Why does the central bank create fiat for special interests such as the banks?

Why is equal protection under the law ignored when it comes to fiat? Which is supposedly the citizens’ money?

Bravo to Iceland! To a people so “simple” that they understand justice – at least much more so than the so-called sophisticated US and European authorities.

Great post, Bill.

I know you’re a very busy man and you’re focused on Europe at the moment, but it would be nice to share your thoughts on what’s happening in Venezuela.

aka, government-backed deposit insurance is generally needed because the banks the public uses are private and the insurance is to protect their deposits in case of bank default, which would otherwise wipe out their savings and other deposits. Whether this is the best system is another matter.

I would caution that the population of Iceland is a mere 330,000 compared with 11 million for Greece and 65 Million for the UK. Maybe easier to pull it off in a country that small.

I have just been reading and interesting pamphlet by Bryan Gould, a New Zealander and onetime Cheif Secretary to the UK Treasury, and published by the Fabian Society. It starts off in the right direction but somehow gets a bit muddled along the way and doesn’t really come to the best solution at the end. Never-the-less better than what we have got at the moment.

All going to pot anyway. I don’t know if you are getting the news feeds from France Spain and Belgium out there in the wide world?

aka, government-backed deposit insurance is generally needed because the banks the public uses are private … larry

Because the public may not have inherently risk-free accounts at the central bank is the ultimate reason. And why not? Why are the citizens not allowed to use their own nation’s fiat except in the crude, unsafe form of physical fiat, aka cash? Cui bono? Isn’t it obviously the banks and the rich, the most so-called creditworthy?

Besides, the abolition of government-provided deposit insurance should require the equal distribution of large amounts of new fiat to the citizens to allow the transfer of at least some of currently insured deposits to inherently risk-free accounts at the central bank (I speak of the US).

Maybe easier to pull it off in a country that small. Nigel Hargreaves

With today’s computers and communications it is beyond dispute that even China could allow its citizens to each have even multiple inherently risk-free accounts at its central bank.

I guess the idea has not yet occurred to the Icelandic authorities.

No deposit insurance in New Zealand (or Australia I think).

No deposit insurance in New Zealand (or Australia I think). william

Perhaps not explicitly but I doubt their central bank/bank regulators allow depositors to lose money – at least not yet. And there still remains the moral issue of the central bank creating fiat for private interests and not allowing the citizens to deal with their own nation’s fiat except crude, unsafe physical fiat.

Australia now has deposit insurance for a range of different types of accounts up to A$250k and applies to accounts in banks, building societies, and credit unions. These accounts are safe, up to the stipulated limit. Having no limit would incentivize hoarding behavior. What a proper limit ought to be should be arrived at via a general social decision process.

Having no limit would incentivize hoarding behavior. larry

Accounts at the central bank are inherently risk-free so there’s no need for government provided deposit insurance at all. It should be abolished as an unneeded subsidy of the banks and the rich, the most so-called creditworthy.

As for discouraging hoarding within cb accounts, negative interest could be charged past a certain account balance or equal fiat distributions to individual citizen accounts at the cb could be used to generate price inflation and thus punish hoarding by eroding purchasing power. I prefer the latter.

Yes, I definitely prefer the latter. Forget I mentioned negative interest rate, please. Hoarding should be punished with price inflation via equal fiat distributions to the citizens.

Nigel,

Was that the ‘Productive Purpose’ pamphlet? I felt Gould’s reasons for rejecting MMT were unfounded.

“Because the public may not have inherently risk-free accounts at the central bank is the ultimate reason. And why not? ”

Central bank accounts and insured deposit accounts at private banks are functionally equivalent. It changes the accounting slightly and reduces the risk cost of private banks allowing them to make loans at a lower cost.

You have to think of private banks in the same way you do private refuse collectors who work for your local council. They are still part of the council service and are constrained by contract in the same way as any other outsourcer.

Central bank accounts and insured deposit accounts at private banks are functionally equivalent. Neil Wilson

No they are not because the present system conflates risk-free deposits with at-risk, not necessarily liquid investments thereby holding the economy hostage to the banking cartel. Let’s abolish deposit insurance, allow accounts for all at the central bank and the economy will finally be free of the banking cartel since an alternative payment system will then exist outside it.

and reduces the risk cost of private banks allowing them to make loans at a lower cost. Neil Wilson

By holding the deposits of the poor and other non so-called creditworthy captive to the banking cartel. Is that how you prefer interest rates to be kept low, Neil? By looting the poor?

Besides, equal fiat distributions to all citizens can drive interest rates in fiat to near zero if desired. As for inflation risk, that can be reduced by eliminating other privileges for the usury cartel too such as a fiat lender of last resort.

You have to think of private banks in the same way you do private refuse collectors who work for your local council. Neil Wilson

Implying that garbage collection is a natural monopoly? Maybe so (but a poor example of one, btw) but anyone could lend fiat once they have an account at their central bank. But we can’t have that can we? Because the deposits of the poor and other non so-called creditworthy must be held captive within the usury cartel?

Hello Bill,

but what about Russia?

(a) Russia issues its own currency;

(b) Russia enjoys a floating exchange rate; and

(c) Russia sets its own interest rate.

Is Russia a sovereign monetary nation? Or strong dependence from oil export destroying basic MMT assumptions?)

aka and Neil ,

For me the important thing is there is a state bank.

It should be unconscionable that the state could bail out or nationalize failed financial parasitic banks again.

The insured deposits should only be accessible through an account at the state bank.

In general we should not nationalize failed concerns .If the state feels some goods and services

are vital and the private sector is failing to provide such services which are adequate quality

or affordable to people on modest means the state should provide them independent and

parallel preferably .

Health,Education,Banking,Housing,Scientific Research,Non co2 producing energy.

“I would caution that the population of Iceland is a mere 330,000 compared with 11 million for Greece and 65 Million for the UK. Maybe easier to pull it off in a country that small.”

The europhiles say that this or that country is too small to pull it off. When the cpuntry is bigger, they say: it is much bigger to pull it off like Iceland. Horse shit.

J Christensen: The scarcity of available local resources to develop a self sufficient domestic economy has been mentioned as one reason for Greece being so reluctant to abandoning the monetary union.

Mentioned – meaning merely claimed, stated. For this claim has no basis in reality.

Greece has two world class foreign exchange earners – the largest merchant shipping fleet in the world, about 15% of the entire world’s- based in a quite small country. And tourism of course, a solid earner. Greece is self-sufficient in food. As for petroleum it has substantial refinery overcapacity, which it has already used to “turn into oil” – by basically barter deals, avoiding “international finance” by taking crude and accepting payment by a fraction of the refined product.

As you say, it is all based on illusions. Unfortunately, Alex Tsipras and too many of his Syriza party are utterly brainwashed by these illusions spread by sharply dressed men who pretend to know what they are talking about. And his suicidal stupidity spread to the Greeks who re-elected him, after having defiantly voted NO, giving him all the support he needed to exit the Euro.

Again: The most potent weapon in the hands of an oppressor is the mind of the oppressed.