Yesterday (April 24, 2024), the Australian Bureau of Statistics (ABS) released the latest - Consumer…

Central banks still funding government deficits and the sky remains firmly above

There was an article in the Financial Times last week (August 16, 2017) – Central banks hold a fifth of their governments’ debt – which seemed to think there was a “challenge” facing policymakers in “unwinding assets after decade of stimulus”. The article shows how central banks around the world have been buying huge quantities of government (and private) bonds and holding them on their balance sheets. Apparently, these asset holdings are likely to cause the banks headaches. I don’t see it that way. The central banks, in question, could write the debt off any time they chose with no significant consequence. Why they don’t is the question rather than whether they will become insolvent if the values crash (they won’t) or whether the yields will skyrocket if they sell them back into the non-government sector (they won’t). Last week (August 15, 2017), the US Department of Treasury and the Federal Reserve Board put out their updated data on Foreign Holders of US Treasury Securities. Other relevant data was also published which helps us trace the US Federal Reserve holdings of US government debt. Overall, the US government holds about 40 per cent of its own total outstanding debt – split between the intergovernmental agencies (27.6 per cent) and the US Federal Reserve Bank (12.4 per cent). In some quarters, the US central bank has been known to purchase nearly all the change in total debt. That folks, is what we might call Overt Monetary Financing and the sky hasn’t fallen in yet as a consequence.

They report, as if it is news, that “Leading central banks now own a fifth of their governments’ total debt” which is in the assessment of the journalists:

… a sign of the scale of the challenge they will face in unwinding unprecedented stimulus measures deployed over the past decade.

Why is that?

Well central banks in six nations that “embarked on quantitative easing over the past decade” now hold “more than four times the pre-crisis level” of assets and the public composition amounts to “one dollar in every five of the $46tn total outstanding debt owed by their governments.”

Scared yet?

The article recounts that:

Central banks’ bond-buying has helped push sovereign yields to record lows and in some cases into negative territory, with bondholders paying governments to own their paper.

Okay, that just shows who is in charge – the currency-issuing government not the bond markets.

Private bond dealers are being forced ” into a hunt for yield” by the central banks. The idea that the bond traders could force yields up is a myth, although you won’t find that mentioned in any mainstream macroeconomics textbook.

Students are taught – relentlessly – or should I say indoctrinated to believe that when governments run fiscal deficits there is upward pressure on interest rates and bond yields as the finite supply of funds in the investment (loanable funds) markets are squeezed.

We don’t observe that in the real world.

So after reading the article you won’t be able to answer the question the journalists posed that policy makers are now in a difficult situation holding all those public (and private) assets on their books yet wanting to push up interest rates.

The inference is that if the central banks reverse their transactions and start selling the bonds back into the secondary bond markets, the excess supply will drive down prices and push up yields.

Then the government will run out of money, n’est ce pas? That sort of nonsense still takes up space in newspapers and other media on a more or less daily basis.

Solution?

Simple, select the numbers pertaining to these assets in the accounting system of each central bank and hit delete.

Yes, that seems easy enough.

All those government liabilities could be written off by the central banks holding them – without consequence.

That is about all you need to know.

The fact is that for many years now, central banks have been funding government deficit spending in a number of countries by creating liquidity – the very act that is meant to lead to an apocalypse of hyperinflation.

At various times the hysteria propagated by the mainstream economics fraternity swings between fears about foreign ownership of government bonds to central banks going broke because their assets become worthless as governments default to central banks running out of control printing presses in sinister and dark basements that lead to people buying wheelbarrows to wheel their loose change from shopping around.

We know that foreign purchases of, say, US government cannot be construed as funding the US government. If that government chooses it can keep spending with zero foreign government debt purchases.

We know that there are no printing presses running mischieviously in basements. Just operators at computer terminals crediting and debiting relevant accounts.

And we know that the massive buildup on the asset side of central bank accounts of government bonds has no implications for their solvency. Central banks can never go broke.

I have been tracking this for a number of countries. Today, I update my US analysis given the Treasury and Federal Reserve has only recently provided new data.

I have written about the US central bank balance sheet before (among other blogs):

1. The nearly infinite capacity of the US government to spend.

2. When the government owes itself $US1.6 trillion.

3. The US government can buy as much of its own debt as it chooses.

4. Helicopter money is a fiscal operation and is not inherently inflationary.

5. Foreign sales of US government debt are largely irrelevant.

There are a few data sets that you can pull together to break the total US public debt outstanding down into various categories:

- The US Treasury’s Bulletin Chapter on Ownership of Federal Securities, which provides a detailed breakdown of who holds the outstanding US government debt.

- US Treasury Foreign breakdown.

- US Federal Reserve Bank’s Consolidated Balance Sheet data.

- US Federal Reserve Bank’s Financial Accounts of the United States.

So what has been going on?

First, 2011.

The following pie-chart shows the proportions of total US Public Debt held by various categories as at the March-quarter 2011.

The government sector held about 42 per cent of its own debt. These holdings were either in the intergovernmental agencies or the US Federal Reserve Bank.

The US Federal Reserve held 8.9 per cent of total US public debt. Its total holdings were around $US 1,274.3 billion.

The three largest foreign US debt holders at the March-quarter 2011 were China (8 per cent), Japan (6.4 per cent) and Britain (2.3 per cent). The total foreign held share was equal to 31.4 per cent.

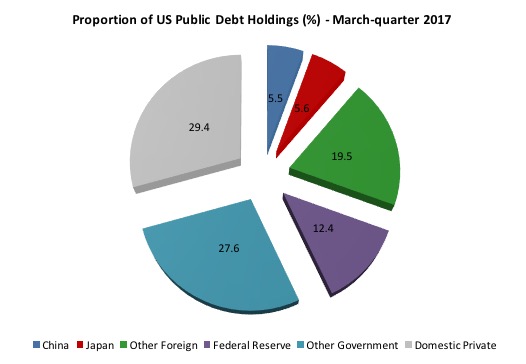

Now, to the most recent data – March-quarter 2017 – some 6 years later. Some of the data, by the way, is available for the June-quarter 2017, but only the complete set required for this analysis is available for the March-quarter.

As at the end of March 2017, there were $US19,845.90 billion Federal Securities outstanding. These were broken down into:

1. Privately held – $US11,904.80 billion (60 per cent of total).

2. Federal Reserve and Intragovernmental holdings (SOMA and Intragovernmental Holdings) – $US7,941.10 billion (40 per cent of total).

3. Foreign and international – $US6,079 billion (30.6 per cent of total) – of which $US3,879.7 billion held by Foreign Official institutions (central banks etc).

A comparison of movements over the last 5 or so years in the composition of US Treasury debt holdings is provided by the two pie charts

The government sector held about 40 per cent of its own debt in the September-quarter 2016. This is slightly down on the proportions held in the March-quarter 2011 (41.8 per cent).

These holdings were either in the intergovernmental agencies (27.6 per cent) or the US Federal Reserve Bank (12.4 per cent). So the central bank has increased its holdings over the period in question and now holds $US2,464.4 billion and increase of 93.4 per cent in overall levels.

The Chinese holdings were around 5.5 per cent of the total and hardly consistent with the rhetoric that China was bailing the US government out of bankruptcy. These holdings have fallen in recent years (see below).

The three largest foreign US debt holders at the March-quarter 2017, were China (5.5 per cent); Japan (5.6 per cent) and Ireland (1.6 per cent).

The impact of the British austerity is noticeable. In 2011, Britain was the third largest holder of US public debt (at 2.3 per cent of total US public debt). By March 2013, this had dropped to 0.95 per cent. They shed $US166 billion worth of US treasury securities in that 24 month period. As at the March-quarter 2017, the British share had risen again to 1.2 per cent of the total.

Over the last year, the the US Federal Government has purchased 23.5 per cent of the new public debt issued, the US Federal Reserve has purchased 7.5 per cent and the private secotr has purchased 68.9 per cent.

By way of comparison, in 2011, the increases in the US Federal Reserve’s holdings accounted for 54.7 per cent of the total increase in US federal government debt. That fell away to 4.3 per cent in 2012 and then rose again to 84.9 per cent in 2013.

The proportion has been decreasing since then but has risen in the last year again.

The recent history thus provides a very important lesson. The US central bank can initiate very dramatic shifts in the mix of debt holders whenever it chooses.

This means that the central bank can always purchase any debt that the private sector chooses not to purchase via the primary auctions.

There is never a reason for US government bond yields to rise above a level that the government considers to be accpetable.

To repeat, the US government (consolidated Treasury and central bank) can always assume the role of its own largest lender and borrow as much as it likes from itself (subject to Congressional ceilings etc).

That is how nonsensical these voluntary conventions are. They sound robust but in the end the currency-issuer is the currency-issuer and can always work around the so-called constraints.

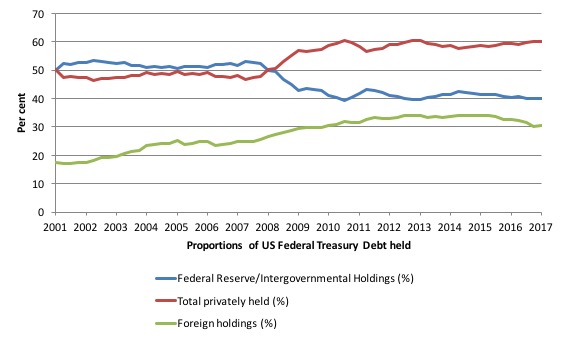

The next graph shows the evolution from the March-quarter 2001 to the March-quarter 2017 of the US public debt by private, public and foreign holdings (%). The foreign holdings are a subset of the private series.

There are some interesting points to note. At a time when the US public debt ratio has risen beyond what the mainstream claim is the danger point (80 per cent) – the point after which we are repeatedly told a nation will struggle to ‘fund’ its outstanding public debt – the private demand for US public debt has risen.

Private markets know that US Treasury debt is risk free, despite all the scare mongering that the likes of the Peter Peterson Foundation and its ilk might regularly entertain.

The other point, in relation to the rising foreign share is that you cannot conclude that the foreigners (China, Japan etc) are ‘funding’ the US government. The US government is the only government that issues US currency so it is impossible for the Chinese to ‘fund’ US government spending.

To understand the trend shown in the graph more fully we need to appreciate that the rising proportion of foreign-held US public debt is a direct result of the trade patterns between the countries involved (and cross trade positions).

For example, China will automatically accumulate US-dollar denominated claims as a result of it running a current account surplus against the US. These claims are held within the US banking system somewhere and can manifest as US-dollar deposits or interest-bearing bonds. The difference is really immaterial to US government spending and in an accounting sense just involves adjustments in the banking system.

The accumulation of these US-dollar denominated assets is the ‘reward’ that the Chinese (or other foreigners) get for shipping real goods and services to the US (principally) in exchange for less real goods and services from the US. Given real living standards are based on access to real goods and services, you can work out who is on top (from a macroeconomic perspective).

Note that a worker in Detroit or some other degenerate industrial region in the US who is suffering from unemployment as a result of cheaper imports coming from nations with lower labour standards (pay and conditions) than the US is unlikely to agree with me. In his/her case I wouldn’t agree with me either.

But from the perspective of macroeconomics there is no issue.

The point is that the US Federal Reserve Bank (as in the case of other central banks around the world) have been taking up significant proportions of the outstanding government debt in the last 10 years. In some years, this proportion has been very high.

We didn’t observe any major inflationary spikes associated with these shifts in monetary operations underpinning the government debt-issuance (and deficit) outcomes.

Please read my blog – Direct central bank purchases of government debt – for more discussion on this point.

Also please read the following blogs – Building bank reserves will not expand credit and Building bank reserves is not inflationary – for further discussion.

Here are some other observations that impact on how one interprets the Financial Times article.

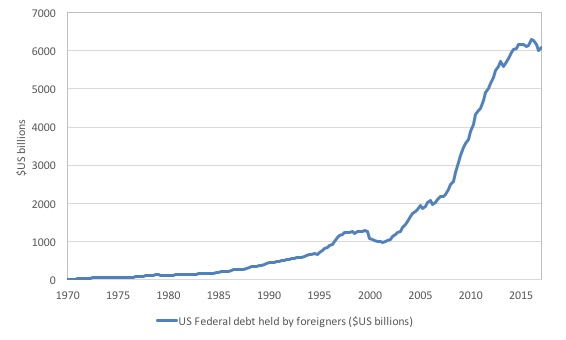

The following graph shows the total US Federal debt held by foreigners since 1970 (in $US billions). There was a dramatic escalation after 2000.

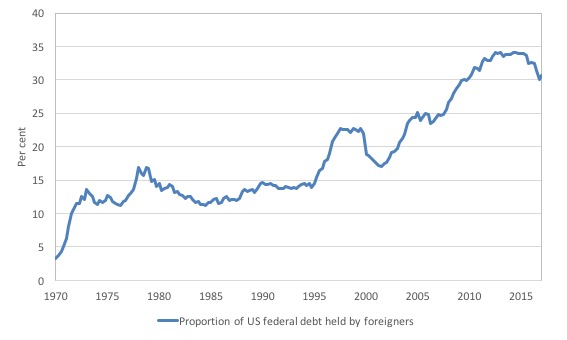

The same data expressed as a proportion of total US Federal debt is shown in the next graph since 1970. You can see that the downturn since 2015 has not been very dramatic in historical times. The US has witnessed variable shares of total debt held by foreigners over this long historical period.

Conclusion

This sort of analysis shows that central banks have been funding government deficits in the US (and similar patterns exist elsewhere as the Financial Times article shows).

Nothing untoward has happened.

The sky is still firmly above our heads.

As a proponent of Modern Monetary Theory (MMT), I do not consider there to be a public debt problem so the analysis presented here is to document what has been happening.

What it shows is that even within the voluntarily-constrained system that regulates the relationship between the US treasury and the central bank, the latter can still effectively buy as much US government debt as it likes.

So if yields rise on US Treasury debt in the coming year it will be because the US government has chosen to allow higher interest payments on the corporate welfare it extends the non-government sector in the form of voluntary debt-issuance.

The question that financial commentators really should be asking is why should the US government extend that corporate welfare to domestic bond-buyers and foreign governments/private investors.

There is no financial reason (in terms of facilitating fiscal policy) for the bond issuance. It is just a form of welfare spending which helps the top-end-of-town.

I would actually like the central bank to just debit and credit treasury bank accounts as required and for governments to dispense with the charade of issuing debt altogether.

Sydney Event – Future of Work and Welfare

For those living around Sydney, Australia, I will be speaking on Thursday afternoon at a Workshop – Right2Work Sydney: Future of Work and Welfare – which has been organised by the Right2Work Coalition and Australian Unemployed Workers’ Union.

The event will run from 14:00 and finish at 16:00.

The location is at the Unions NSW offices, level 3, 4 – 10 Goulburn Street, Sydney, Australia 2000.

I will be debating well-known sociologist Eva Cox, who considers a UBI to be the way forward. I will be discussing employment guarantees in that context.

Crowdfunding Request – Economics for a progressive agenda

At time of writing 63 per cent has been raised with only 4 days left.

I received a request to promote this Crowdfunding effort. I note that I will receive a portion of the funds raised in the form of reimbursement of some travel expenses. I have waived my usual speaking fees and some other expenses to help this group out.

The Crowdfunding Site is for an – Economics for a progressive agenda.

As the site notes:

Professor Bill Mitchell, a leading proponent of Modern Monetary Theory, has agreed to be our speaker at a fringe meeting to be held during Labour Conference Week in Brighton in September 2017.

The meeting is being organised independently by a small group of Labour members whose goal is to start a conversation about reframing our understanding of economics to match a progressive political agenda. Our funds are limited and so we are seeking to raise money to cover the travel and other costs associated with the event. Your donations and support would be really appreciated.

For those interested in joining us the meeting will be held on Monday 25th September between 2 and 5pm and the venue is The Brighthelm Centre, North Road, Brighton, BN1 1YD. All are welcome and you don’t have to be a member of the Labour party to attend.

It will be great to see as many people in Brighton as possible.

Please give generously to ensure the organisers are not out of pocket.

That is enough for today!

(c) Copyright 2017 William Mitchell. All Rights Reserved.

Debts, money, all just markings on an accounting books. Central banks hold the books.

Now what are we scared at, exactly?

@Hepion,

They are scared that if government is not revenue constrain, the only risk is inflation and inflation can be managed with taxes, the only issue left to discuss is how we distribute the economic output.

For sure, this is a discussion that they don’t want to have.

We? We are scared about the consequences of not having that discussion.

Great post! A little side note, the section just before the conclusion is repeated twice word for word. Keep up the good work Bill!

Bill, why do you keep saying that central banks are BUYING government debt, when they are actually SWAPPING government debt back into the “reserves” the government spent into existence previously. There is no net change in the net fiscal assets in the economy unless, the central bank buys a private sector (corporate) asset. In which case it would have to be funded by the currency issuing Treasury.

Dear acorn (at 2017/08/24 at 3:20 am)

I say “buying” because that is what they are doing. They are going into secondary asset markets and making purchases like anyone else who makes similar purchases.

There is no need to hide from that.

Clearly, there is no change in net financial assets in the non-government sector as a result, but that doesn’t negate the fact of the transaction.

best wishes

bill

Yep. The continued denial, to themselves and to anyone who can actually think for themselves, that central banks are part of the government sector shows the extent of the havoc that the Groupthink virus has caused on the brain function of economics experts who even attempt to rationalise the absurd of accounting of QE to make it fit in with their core beliefs. It really is absurd.

“Clearly, there is no change in net financial assets in the non-government sector as a result”

It’s rather important to focus on that point as opposed to what the transaction looks like. Because bank accounting is backwards, and that is used to confuse people.

For example bank reserves are technically the commercial bank lending to the central bank. A point that is used by certain economists (who shall remain nameless) as propaganda to try and show how the commercial banks control everything and why we need ‘sovereign money’.

In reality it is the power relationship that determines what happens not the fact that something is technically a loan. If I can force you to loan me money at a rate I determine, who is in charge?

Government accounting is similarly bank accounting and backwards. There is no justification for the term ‘government debt’ for example, unless you similarly use the term ‘bank debt’ to describe any accounts that are in credit.

Thanks Bill, I get your point. Meanwhile, I am trying to remember which of the MMTers used the term “the government always spends twice”. I think it was one of the UMKC profs.

Meaning, that when the UK Treasury keyboards (spreadsheet transfer) my pension into my high street bank account, it simultaneously keyboards the equivalent amount, into my high street bank’s “reserve” account at the Bank of England. Hence, the liability imposed on my bank, is balanced by an equivalent asset. Balance sheet remains balanced.

It makes it easier to explain the difference between a currency issuer and a currency user. Also, explaining how if I move my pension to another high street bank, the BoE will move the equivalent “reserve” to the new bank, to maintain balance sheet balance. Likewise, if I bought a government bond, the BoE would move the reserve to a Treasury securities account at the BoE; or, a cash account, if I took my pension out of an ATM.

This video is exactly what MMT needs a lot more of. https://www.youtube.com/watch?v=TDL4c8fMODk&feature=youtu.be

@great blog post

@neil ,if anything your description of bank reserves as commercial bank loans to the central bank is confusing

Actually, if equal protection under the law is to mean anything, the central bank should ONLY create fiat for its monetary sovereign – that or also distribute equal amounts to all citizens.

And if we are to avoid welfare proportional to account balance, rather than need, then the debt of a monetary sovereign should yield AT MOST 0% and that would be for the longest maturity sovereign debt (e.g. 30 yr US Treasury Bonds); shorter maturities should yield even less (negative yield) with private sector account balances at the central bank (aka “reserves” in the case of banks) having the most negative interest.

That said, individual citizens should have negative-interest-free accounts at the central bank up to, say, $250,000 per citizen. And then what need for government-provided deposit insurance and other privileges for depository institutions?

But, of course, ethics should be avoided at all costs wrt fiat and credit creation because look how well the current system has worked and is working! So never mind. /sarc