It's Wednesday, and as usual I scout around various issues that I have been thinking…

Some MMT considerations for an independent Scotland – Part 2

This is the second and final part of my series on Scotland as I prepare for a visit to Edinburgh and Glasgow this week. You can see the details from my – Events Page – and I urge interested readers to support the events that are run by activists. I will be talking about issues pertaining to the monetary arrangements that might accompany a move to Scottish independence. I have noted in the past that this is a controversial issue in itself that is also made more divisive because it has become intertwined with the vexed issue of EU membership. In Part 2 I provide a detailed critique of the so-called ‘six tests’ that the Scottish Growth Commission put forward as being determining factors as to when Scotland could move off the pound. I find the tests to be just neoliberal artifacts designed to keep Scotland on the pound indefinitely and thus curb any real independence. I also consider issues such as EU membership. And I provide some historical details of the way a monetary union might dissolve.

My previous blog posts on Scotland are:

1. Some MMT considerations for an independent Scotland – Part 1 (May 6, 2019).

2 Ridiculous MMT critiques distorting Scottish independence debate (April 23, 2019).

3. Oh Scotland, don’t you dare! – Part 2 (June 5, 2018).

4. Oh Scotland, don’t you dare! – Part 1 (June 4, 2018).

5. I would be voting NO in Scotland but with a lot of anger (August 18, 2014).

6. Bonnie Scotland – ignorance or denial – either way it is fraught (October 30, 2013).

7. Scotland should vote yes in 2014 but only if … (September 27, 2012).

At the recent Scottish National Party Spring Conference (April 27-28, 2019) the delegates rebelled against the leadership of the Party by successfully proposed the so-called Amendment D, which demanded that a new currency be introduced “as soon as practicable” after a vote for independence.

Significantly, it also requires that the new government take back responsibility for determining when the currency would be introduced instead of the previous position that the government would take advice from the central bank about the progress towards meeting the ‘six tests’.

However, I was disappointed to see that the Conference did not vote on any changes to the validity or standing of the ‘six tests’.

Another attempt to change the status quo, the so-called Amendment B, which wanted explicit removal of the ‘six tests’ from the process, was rejected.

Indeed, I saw a Tweet from the First Minister after Amendment D went through, along the lines of:

Amendment urges progress as quickly as practicable, and six tests to ensure solid foundation for decision are endorsed. We can move forward now with confidence to make the case for Scotland’s future in Scotland’s hands.

This is a major disconnect in the understanding of what Amendment D was seemingly aiming to achieve. It also represents a major problem within senior SNP ranks about what the ‘six tests’ mean and why they will hold back prosperity should independence be achieved.

So let’s examine the ‘six tests’ one more time.

The currency choice

While the Sustainable Growth Commission (see – Part 1 for links to Final Report) recommended the retention of the British pound until “a series of tests for future currency decisions” are met, it seems that in the last several months the debate has moved on somewhat.

In previous analysis of the so-called ‘six tests’ (see blog posts (3) and (4) above), I concluded that if adopted Scotland would be locked into using the British pound indefinitely.

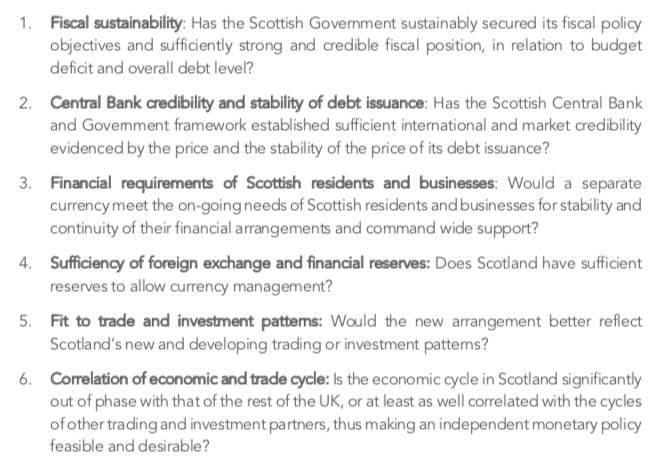

The six are (as outlined in the SGC Report):

From a Modern Monetary Theory (MMT) perspective, these tests have limited relevance to whether a nation is viable with its own currency.

Test 1

Fiscal sustainability is erroneously defined in terms of some financial ratios and targets that the currency-issuing government cannot realistically achieve anyway, given the fact that the fiscal outcome is heavily driven by the spending and saving decisions taken by the non-government sector.

The SGC uses the Stability and Growth Pact rule that a fiscal deficit should not exceed 3 per cent of GDP without acknowledging the dysfunction that rule has cause Member States in the EMU and without recognising that its origins were purely arbitrary anyway. There was no economic foundation to that rule.

I discuss the provenance of the rule in detail my 2015 book – Eurozone Dystopia: Groupthink and Denial on a Grand Scale.

Further, what context does that recommendation relate to?

What happens if, in order to attain full employment, in the face of an external deficit (certain for Scotland) and a high desire to save overall from the private domestic sector, a fiscal deficit of 8 per cent of GDP was necessary?

From an MMT perspective that would be ‘sustainable’ because it was consistent with advancing well-being and providing public spending support to achieve full employment.

Trying to achieve a 3 per cent or lower fiscal deficit in this context would devastate the economy.

At present, the fiscal deficit (with North Sea revenue) is around 8 per cent.

What is going to change in Scotland that would justify taking more than 5 per cent of GDP out of the economy by contracting public net spending?

Does the Growth Commission think there will be a major export boom? It would have to be massive and unprecedented. And … it is not going to happen.

Does the Growth Commission think the private domestic sector will be prepared to go into massive deficits and accumulate ever increasing levels of indebtedness?

That would not only be an unsustainable trajectory but is also not going to happen.

To better understand the concept of fiscal sustainability and disabuse yourself of the false claim that it is somehow related to deficit history or public debt ratios, the following introductory suite of blog posts will help:

1. Fiscal sustainability 101 – Part 1 (June 15, 2009).

2. Fiscal sustainability 101 – Part 2 (June 16, 2009).

3, Fiscal sustainability 101 – Part 3 (June 17, 2009).

They explain how Modern Monetary Theory (MMT) constructs the concept of fiscal sustainability.

Test 2

How would a new central bank that doesn’t set interest rates ever establish such credibility?

Credibility for financial markets?

And how would it establish competence when fluctuations in the British economy would still seriously undermine the newly independent nation’s capacity to raise pounds in international markets if it continues to use the British pound?

Imagine the British trade deficit increases and the pound starts to depreciate. Given that Scotland would be using the British currency, its price level would be dependent, in part, on British exchange rate movements.

So Scotland would be forced to import inflation via the British pound depreciation despite nothing fundamentally changing in terms of its own unit costs. This is purely because it chose to forego the benefits of its own currency.

And the ‘central bank’ would be powerless to do anything about it – even in mainstream terms.

Scotland would have to take UK interest rates as given (so no room to create incentives or disincentives for financial flows) and nominal movements in the pound would drive Scotland’s real exchange rate, which is the accepted indicator of international competitiveness.

There are situations where importing such dynamics from Britain would be favourable but there are also many situations where they would destabilise the Scottish economy.

You could imagine a situation, for example, where productivity growth in the British economy was accompanied by favourable capital inflow which was pushing sterling up in foreign exchange markets.

There was no coincident productivity growth in Scotland.

As a result, Scotland’s real exchange rate would rise and its international competitiveness would decline, while the productivity growth in Britain would offset the loss of competitiveness via the nominal exchange rate increase.

Further, the interest rate environment is clearly determined by what the Bank of England deemed to be suitable for advancing its agenda, which certainly would not include any consideration of the impact of different interest rate choices on Scotland.

Why does this matter?

If the economic cycles of the two nations start moving in different directions, then being forced to adopt interest rates that are designed for the current state of the UK economy will result in ‘pro-cyclical’ policies being implemented in Scotland.

So, for example, if the UK is facing an inflationary surge while Scotland was in recession and the Bank of England starts hiking interest rates, Scotland would have to endure higher interest rates even though the responsible direction for Scottish policy is to relax monetary policy.

The reverse of this type of dynamic is what caused the massive imbalances in the Eurozone prior to the crisis. Low interest rates imposed by the ECB were to offset the German recession and stagnation in 2002-03. But they fuelled a massive property boom in Spain and Ireland, for example, nations which were not in need of the monetary support.

Of course, this may not matter that much given that monetary policy is not a very effective policy tool for controlling aggregate spending patterns anyway.

But usually, fiscal policy is forced into passively supporting the monetary policy stance. And then the pro-cyclicality of the policy positions becomes deeply problematic.

Test 3

How would we decide whether “a separate currency … [was meeting] … the on-going needs of Scottish residents and businesses for stability and continuity of their financial arrangements and command wide support”.

If we imposed all tax and other obligations to the state in the new currency then it would immediately “meet the on-going needs” because Scottish residents and businesses would have to acquire the currency.

Further, if the newly independent Scottish governments used its newly acquired currency-issuing capacity to bring idle resources into productive use (for example, via a national job creation scheme – Job Guarantee) then it would be hard to say that that the on-going needs of Scottish residents were not being met.

How would that be established?

For example, the newly independent Scottish government would not be able to run an independent full employment policy with large-scale public sector job creation if the UK government was running an austerity bias and the Scottish government was forced to target fiscal balance due to lack of tax revenue or borrowing capacity in the foreign currency.

Consider the situation where the remaining British citizens decided to increase their overall net saving (meaning that the private domestic sector aimed to spend less than its income), then, given its external deficit, unless the British government increased its fiscal deficit to ‘fund’ the new saving aspirations of the private domestic sector, the British economy would go into recession and its fiscal deficit would rise anyway via the automatic stabilisers.

The situation in Scotland would be dire and its government would be largely defenseless.

A major British recession would impact directly on Scotland in three important ways: (a) its tax revenue in pounds would slump; (b) its ability to borrow in pounds to fund a rising deficit would be compromised; and (c) its export revenue would decline.

From this state, the application of the fiscal rules proposed by the Growth Commission would force the Scottish government to cut its spending for fear of running short of pounds.

As a consequence its recession would be magnified and the Scottish government could do little to avoid the damage.

The problem that is often raised is shifting to a new currency disadvantages those who hold debt (and particularly, home mortgage debt) obligations.

There are well-established policy interventions that can be used to overcome these issues.

1. The only moves that are really required to establish the new currency is that the Scottish government announces that from some point onwards, all tax obligations must be resolved using that new currency.

Further, it announces that all its employment and procurement payments will be in the new currency.

That decision generates a pent-up demand for the currency.

2. There is a huge difference between introducing a new currency altogether, which has no volume in foreign exchange markets and breaking a peg of an existing currency or abandoning the use of a foreign currency which is already being bought and sold in the international currency markets.

The Scottish government would have to supply the new currency into existence and/or swap British pounds at parity for the new currency.

Initially, the supply of the currency would be restricted by the government spending (given that this is the way the currency would enter the monetary system).

So massive excess supplies of the currency are not likely immediately, and that is the requirement for depreciation in a floating exchange rate system.

Eventually, as the currency volumes increased in the foreign exchange markets, buying and selling on international markets would determine its value.

There is no reason to assert that the new currency would then collapse.

As we will see, the swapping of the currencies would also generate substantial sterling reserves in the newly created Scottish central bank, which if the government chose, could be used to service former British debt obligations.

3. There is no real need to redenominate all contractual (public or private) arrangements into the new currency.

For example, the government could decree that existing bank deposits be swapped to left depending on the choice of the depositor. If they wanted to leave their deposits in pounds that would not impinge on the newly-established sovereignty of the government.

These depositors, would have to acquire the new currency to pay their tax obligations and the act of selling pounds to get the new currency would serve to strengthen the new currency.

My preference would be for the new Scottish government to redenominate all its own debts (including those they incur as part of a sharing agreement with the British government upon exit) in the new currency by taking advantage of the principle of Lex Monetae (the Law of the Money).

I discussed this in detail in my 2015 book – Eurozone Dystopia: Groupthink and Denial on a Grand Scale – in relation to the Eurozone.

This is a well-established legal principle, backed up by a swathe of case law across many jurisdictions, and is internationally accepted.

It states broadly that the government of the day determines what the legal currency is for transactions and contractual obligations within its national borders.

There is thus no question that Scotland could introduce its own currency, and require all taxes to be paid and all contracts to be denominated in that currency.

Lex Monetae also has been taken to mean that if, say, an Italian had borrowed US dollars from a London bank operating under English law, the definition of the ‘currency’ for the purposes of resolving this contract is governed by US law.

Finally, the principle also means that if a government changes its currency and re-denominates at some given parity, all contracts must be honoured at the re-denominated rate.

So as part of the break with the rUK, the new Scottish government should negotiate an arrangement that any debt it inherits from the old UK (on a per capita basis presumably – see below) is immediately redenominated in the new currency at a 1:1 parity.

Given, the new currency should also be allowed to float, then the initial conversion rate is moot. The foreign exchange markets will sort out the levels quickly enough.

Floating will give the domestic policy instruments (fiscal and monetary) maximum scope to pursue domestic aims including restoring growth and creating jobs.

As noted above, it would reasonable to expect the new currency to push up in relative value initially.

Application of the Lex Monetae principle would be blurred or dual in nature in this context because the British pound would persists after the introduction of the new currency.

The complication is likely to apply more to private contracts than the public debt, which typically recognises that a government issues liabilities in the currency of use.

Ultimately, the legislative capacity of the new independent government would be dominant and would allow that government to introduce whatever arrangements it felt were in the best interests of its citizens.

One of the advantages of redenomination is that any losses only arise if the new currency depreciates significantly. This provides the holders of the redenominated assets an incentive to work to ensure the depreciation is contained and that there is confidence in the new currency.

Test 4

This Test reflects the sort of scaremongering that neoliberals deploy to militate against currency freedom.

First, why would it be necessary for “Scotland … [to] … sufficient reserves to allow currency management” if it floats its currency?

It would be madness for the new nation to peg its new currency to the pound or the euro or any currency and then try to manage that peg.

Smaller nations that adopt pegs are always the prey of currency speculators.

Like all nations that issue their own currencies, the newly independent Scotland would be advised to float its currency on international currency markets.

The float will settle at the level that matches its relative productivity and domestic costs.

It frees the central bank from having to compromise domestic policy to defend a peg and also means it does not have to accumulate foreign reserves.

Further, in times of currency stress, a far better strategy for the new Scottish government would be to deploy capital controls to advantage, instead of trying to use the ‘market’ to buttress the exchange rate. Trying to beat of the speculators with foreign exchange sales is fraught and finite.

I would also not advocate borrowing in foreign currencies to establish a pool of foreign reserves. That is a recipe for disaster for any nation and compromises its currency sovereignty.

Other suggestions to engage in currency swaps with central banks elsewhere are also fraught (they introduce exchange rate risk before the swap is reversed) and are unnecessary (why bother?).

But, as I noted above, the new nation would likely accumulate foreign reserves (principally the pound) in large quantities. How?

1. The need for the new currency created by imposing all tax and other obligations to the state in the new currency would generate a flow of pounds into the new government’s reserves as holders of pounds sought to get hold of the new currency.

2. In the settlement with the rUK upon independence, not only would the new nation (presumably) take on a per capita share of outstanding British government liabilities but would also receive its share of the UK’s official gold and foreign currency reserves.

At present these reserves are held by the Bank of England and are made up of (Source):

– gold

– foreign currency assets

– International Monetary Fund (IMF) special drawing rights

– the UK’s Reserve Tranche Position (RTP) at the IMF.

These reserves (except the RTP) are held in a government account known as the Exchange Equalisation Account (EEA), which is administered by the Treasury.

The latest data from the Bank of England – UK International Reserves – April 2019 – (published May 3, 2019) shows that:

1. The UK has total reserve assets worth $US 171,971 million comprising …

a) Foreign currency reserves of $US119,441 million.

b) IMF reserve position of $US7,048 million.

c) SDRS of $US13,675 million.

d) Gold of $US12,786 million.

e) Other reserve assets of $US19,021 million.

7. The UK also has foreign currency liabilities (forwards, swaps and repos) amounting $US114,761 million so its net position was $US57,210 million.

8. The Bank of England, itself, has net foreign currency assets of $US7 million.

So a per capita share based on the ONS estimate that the Scottish population is around 8.2 per cent of the UK population, would suggest that the new government would immediately gain around $US4.7 million of the net foreign exchange assets.

This would be $US14.1 billion in reserve assets and $US9.4 billion in reserve liabilities.

Test 4, however, is redundant if the currency floats.

Test 5

A monetary sovereign nation has to have its own currency and only then can it look forward to being able to create an attractive investment climate.

Using the pound would mean that Scotland’s cycle would remain tied into the rUK cycle and the investment climate that was established by the rUK policy settings.

Those settings might be sound and the investment climate attractive.

But in this era of austerity, the investment ratio has slumped and businesses have demonstrated a reluctance to engage in new innovations (with exceptions).

Having its own currency would allow the Scottish government to work with industry to develop new productive activities and ensure a reliable supply of skilled labour.

A fully-employed economy, with a high quality education and training system, and stable government that maintains the rule of law (with contractual stability) is what attracts business investment.

Scotland will struggle to provide that while using the pound.

Test 6

As noted above, as long as Scotland used the pound and was an interest-rate taker and bound by fiscal rules dominated by the rUK, the capacity to break out of the rUKs economic cycle is close to zero.

Scotland would always be in the position that if the rUK sneezed, Scotland would catch a cold.

Once independence was established and fiscal sovereignty introduced, then the cycles could vary as a result of different fiscal policy regimes.

Conclusion on the Tests

The tests are a mixture of neoliberal sound finance and strategic barriers, which when taken together, would ensure the new government would become an indefinite client state of the rUK.

Those seeking independence and who pushed through Amendment D seem to want a new currency within three years of independence. Even that time horizon would appear to be too long.

But if the six tests are maintained, Scotland may never be able to implement its own currency.

Other issues

1. Membership of the EU

Scotland should make no attempt gain membership if the EU.

Scotland would cease to be an independent nation once its legislative autonomy is compromised by the fact that the European Court of Justice can overrule it and it has to be consistent with the neoliberal, corporatist agendas coming out of Brussels.

And if Brexit occurs, then Scotland will have less of a transition problem than if Britain stays in the EU.

I should note that this issue, as well as other policy choices, is not derived directly from MMT reasoning. Everyone might fully understand MMT principles yet still opt, based on their values, to join the EU and take the consequences as they see them.

MMT is a lens for achieving a superior understanding of how the monetary system operates and the capacities that the currency issuing government has within that system.

One has to overlay a set of values (an ideology) to then make headway on specific applications of those principles. In this respect, my values are deeply opposed to the EU status quo where neoliberalism is embedded in the constitutional structure of the union (via the Treaties). It is a root-and-branch matter.

Joining the EU means that a nation surrenders its legislative independence to a neoliberal cabal which has undermined the prosperity of the citizens in the Member States and implemented policies that favour the top-end-of-town.

So as a left progressive I would advocate staying out of that cabal.

2. Debt sharing

Not really an issue. It is probably better than Scotland takes a per capita share of the debt and then redenominates it into the new currency.

But even then that is not necessary.

Under no circumstances should the newly independent Scotland issue debt denominated in any other currency but its own.

3. Freely floating exchange rate

Under no circumstances should the newly independent Scotland peg its new currency to any other currency.

By allowing the currency to float, the nation will achieve maximum domestic policy autonomy and provide the best competitive environment for its traded-goods sector.

It will have all the capacity it needs should the currency become a speculative vehicle that runs the risk of creating damage to the real economy.

4. EMU membership

Under no circumstances should the newly independent Scotland contemplate joining the EMU. This is tied in with point (1).

For a new nation that joins the EU the Treaty says it must adopt the euro as its currency.

“All EU Member States, except Denmark and the United Kingdom, are required to adopt the euro and join the euro area. To do this they must meet certain conditions known as ‘convergence criteria’.”

By taking up a foreign currency, the independence exercise becomes futile and they would have been better off staying within the UK.

5. Who owns the oil?

The debate about sharing of the North Sea oil, which is still in copious supply, will need to be resolved.

It would seem that the rUK will push for a per capita share while Scotland would be advised to push for a geographic a share of North Sea oil?

The Median line – originally used in the 1960s to establish national rights to the oil and was part of the 1965 Norway-UK agreement would probably allow Scotland to have 95 per cent of the oil production currently deemed UK production.

6. Should the new government issue debt?

There is no doubt that the fiscal deficits will have to remain at current and higher levels for some time into the future after independence.

That is not a problem and will be essential to underpin sustainable growth and high levels of employment.

The question that will have to be addressed is what monetary arrangements might accompany that fiscal position.

I will write a separate blog post about this issue (in general) but I do not favour any currency-issuing government issuing debt to the non-government sector to match its fiscal deficits.

Such debt is essentially corporate welfare and is not required to ‘fund’ the deficit spending.

7 Will Scotland be better off after independence?

The transition to independence will be disruptive.

In a material sense, I suspect Scotland will, at least initially, be worse off.

Its fiscal deficit will probably have to increase while trade arrangements are worked out.

It will have to replace the net inflow of public funds from the central government.

If it adopts an austerity bent in the face of larger deficits then things will turn out badly.

A collapse of a monetary union

With the Brexit fiasco continuing, and on-going debate in Scotland about whether they should introduce their own currency or not and, if they do, whether they should peg it to sterling or the euro, it is wise to consult history.

There are many other examples where such policies can reduce foreign exchange market pressures. While the breakup of the Austro-Hungarian Monetary Union in 1919 also provides some insights into the strategies that a government can employ to avoid bank runs (‘overstamping’ existing banknotes; forced loans to government; restrictions on travel) one should not rely heavily on that experience.

The capacity to make electronic transfers now means that people do not have to get on intercontinental trains with suitcases full of banknotes to protect themselves from currency depreciation.

More recent examples demonstrate, however, that capital controls can be effective. Malaysia imposed a range of controls on capital outflows during the 1997-99 Asian financial crisis, which certainly separated its exchange rate movements from the havoc that the other neighbouring nations endured.

As a guide to dissolving a union, we do have a relatively recent example of a federal republic that used a single currency, but which, on February 8, 1993, split the currency into two as part the creation of two separate nations.

Prior to that event, the separate nations within that republic: The Czech Socialist Republic and the Slovak Socialist Republic – had determined they would split.

Historically, the fiscal transfers within the federation, went from the richer Czech Republic to the Slovak Republic and the federation was controlled from Prague. There were dissidents who wanted decentralisation to give more power to the poorer state but that was continually resisted.

An excellent account of these tensions is the 1996 book by Carol Skalnik Leff – The Czech and Slovak Republics. Nation versus State.

She describes “two different Slavic peoples with different languages and historical experiences” coming together into a federation but a “common Czechoslovak identity” never evolved although the “ideology of Czechoslovakism … was a source of endless conflict between the Czechs and Slovaks from the very inception of the state.”

After the so-called Velvet Revolution which followed the end of the Warsaw Pact and saw the transition of power from the Communist Party of Czechoslovakia to a democratically-elected parliament spanning the two states, talk turned to resolving the historical tensions between the, now, Czech Republic and the Slovak Republic (the Socialist tag being dropped).

In January 1991, the Czech government stopped sending payments to the poorer Slovakia (the former’s GDP per capita was more than 20 per cent higher).

Part of Slovakia’s lagging economic performance was due to its inefficient manufacturing sector inherited from the Communist period, the tardiness in the Slovak authorities to invest in new capital and reform pressures coming from the Prague-centred government. There is disagreement in the literature over the relative influence of these factors.

By 1992, the unemployment rate in Slovakia was 10.4 per cent compared to 2.6 per cent in the Czech Republic.

Further, the majority of foreign direct investment went to Czech activities, in part, because Prague officials encouraged injections into the more modern Czech industry.

The important point is that the split that came was not driven by economics. It was a political decision reflecting resentments to the previous Communist rule and a growing sense of Slovakian nationalism.

Eventually, and some argue inevitably, the two states agreed in 1992 to dissolve the federation that bound them together.

The public opinion in both nations was firmly in favour of maintaining the federation but the leaders persisted.

On January 1, 1993, the – Dissolution of Czechoslovakia – became effective, which meant the federal state became split into two separate nations: Czech Republic and Slovakia.

The template the nations used to accomplish the split of the federation is interesting and instructive.

1. Two principles were invoked to accomplish the breakup. On the one hand, a geographic principle was used (to split federal real estate assets). On the other hand, a population proportion principle was used for most of the federal assets.

2. All federal assets, such as military equipment, transport infrastructure, were split according to the relative populations.

3. Financial reserves and state debt was divided according to the 2:1 population principle.

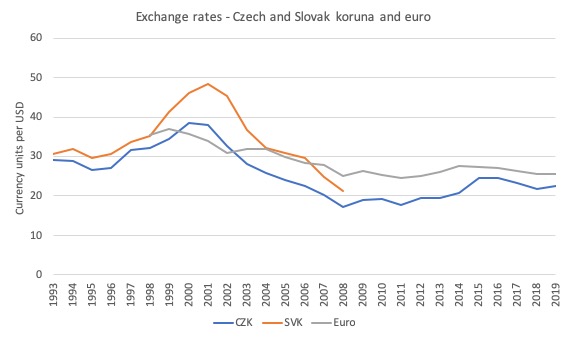

4. Currency – as part of the transition, the original currency – the koruna – was maintained but on February 8, 1993, they adopted separate currencies which were initially introduced at parity to each other.

Eventually, the Slovak koruna depreciated (as a realignment) and then stabilised at the lower rate.

5. At the outset, the old Czech banknotes were differentiated using two different ‘stamps’ and were in use in Slovakia until August 1993. Interestingly, the ‘stamps’ were printed by a British company and the state-owned bank (Komercni Banka) glued them on the federal notes.

6. Capital controls were strengthened and were very effective in protecting the Slovak banking system. There were no bank runs.

7. The transition from old notes to new stamped notes took four days. Citizens could only swap small amounts in cash and had to put the remainder in bank deposits.

8. Citizens could choose with nation to become citizens of.

9. Cross-border passport controls were not established and traffic flowed freely.

10. The existing federal legal framework was embodied in to the legal code of the new nations, unless there were inconsistencies with the new constitutions.

11. Both new nations adopted all the treaties that the old Czechoslovakia had entered into.

12. After initial slumps in trade, the period following dissolution led to new trade relationships being formed.

The following graph shows the currency movements after the split. On January 1, 2009, Slovakia entered the Eurozone and the Slovak koruna (SKK) was exchanged at €1 = SKK 30.1260.

I wouldn’t want to push this example to strongly as a guide for Scotland. That is because at the time of the split there was less integration with the rest of Europe, a history of capital controls and fixed exchange rates.

Both nations were coming out of the Communist era with diminished productive capital.

But the desire to have their own currencies helped the transition and minimise the GDP losses that inevitably occurred in the first instance.

And it was accomplished within 12 months.

Conclusion

There are many issues I have not fully addressed in this two part series.

But I am much better informed of the Scottish situation and have a fairly deep familiarity with the data. Which is a good thing.

We will discuss these issues in more detail on Wednesday night in Edinburgh.

That is enough for today!

(c) Copyright 2019 William Mitchell. All Rights Reserved.

5 Seems a no brainer providing Scotland creates its own currency, floats it and does not take on any foreign debt.

Colin Teese

Apropos the Czech-Slovak case-study:-

“8. Citizens could choose with nation to become citizens of.

9. Cross-border passport controls were not established and traffic flowed freely”.

Prompts me to wonder how that would play out in the hypothetical Scotland-rUK case if Scotland thereupon or subsequently became an EU member. Especially with the example of the EU Commission’s behaviour in regard to the same issue on the island of Ireland in mind.

As we have all discovered, the questions posed by the juxtaposition consequent upon Brexit of a part of the territory of the EU (in the shape of the Republic of Ireland) and that of a non-member state (the United Kingdom of Great Britain and Northern Ireland) have been – or as a deliberate negotiating tactic by the Commission been made into – *the* principal issue bedevilling all attempts to conclude a Withdrawal Agreement acceptable to all parties.

Wouldn’t another land-border between the respective territories in the event of Scottish EU membership give rise to equally intractable difficulties? At least were an equivalent degree of cynical gaming of the rules to be yet again manifested by the Commission in such an instance too.

They habitually represent themselves as being bound by the rules – *their* rules of course. Yet as we have witnessed time after time they break their own rules whenever it suits *them* to do so. Like for example Draghi undertaking to do – and subsequently doing, regardless of the rules explicitly forbidding the actions he proposed – “whatever was necessary”” to preserve the Euro.

Excellent !

Test 4 is where all the Scottish think tanks and the Scottish government end up in a graveyard. That’s both unionist and Indy think tanks.

I would say for the last 3 years I’ve been trying to explain the foreign reserves issue with floating exchange rates they just don’t get it. They all come at it from the wrong point of view and and still stick to fixed exchange analysis based around apparent Kaldorian views religiously. I really don’t understand why post-Keynesian’s can’t get their head around the dynamics of floating rate exchange systems.

James Meadway and Simon Wren Lewis suffer from the same problem no matter how many times it is explained to them.

This nails it for me – So as a left progressive I would advocate staying out of the EU cabal.

Brexit is extraordinary we now live in a world where the right has started to act like the left and left are acting like liberals. This has happened because of a complete mis understanding of how monetary systems operate.

If both the left and the right actually knew how monetary systems operate in reality. The left would be running for the exit door and the right would be trying everything they can to stay in. Instead, the left are doing political and economic gymnastics to stay in and the right are trying everything possible to leave. The liberal left and right the (middle ground) that is now in the middle of the right wing spectrum have fell in love with liberalism of the Neo persuasion. The change UK party should just go where they belong and join the liberal democrats with Chuka Umunna as the new Lib Dem Leader.

The EU is fiscal conservatism on steriods that’s handed real resource allocation to the bankers. If you are from the right what’s not to like ? in one word immigration everything else is from the fiscal conservative handbook.

There’s never been a time in British History when so many politcal parties are on the wrong side of the arguement. Fighting against what they actually stand for. Driven by voters who have no idea how the monetary system actually works.

No more so than in Scotland. With so many left wing voters spread right across the country who are proud to be called left wing and progressive. Yet, want to be at the heart of Europe which is liberalism/ fiscal conservatism on Steriods. Yet, at the last Scottish election the Lib Dems only won 7.8% of the vote and 6.8% of the vote in the UK general election.

No Scottish election in recent memory has ever voted for liberalism/ fiscal conservatism on Steriods. Yet, 60% of the population want to be at the heart of Europe. It’s a delusion as a large % of Scottish voters think the EU is a socialist paradise that will save them. Not bind them in neoliberal globalist/fiscal conservative chains. Then send the IMF in and put a technocrat in place to rule them and leave nothing in public hands apart from Bass Rock lighthouse if they are lucky.

Some of the text of Test 3 is not as clear, to me at least, as it could be. for instance, ” “a separate currency … [was meeting] … the on-going needs of Scottish residents”. There seems to be a missing term here, thereby rendering the sentence not entirely clear.

The relationship between paragraph 3 and paragraph 5 is not clear to me. In para 3, the Scottish government creates its own currency. In para 5, it can’t run an independent JG because the UK government is implementing an austerity program. Why not, one might be led to ask. It appears as though para 5 has reverted to keeping the UK pound.

As for the Euro, I have seen statements from the EU during the past two years that contend that Scotland will not have to adopt the Euro. Is this an instance where a party is not clearly abreast of the situation, or is it something else?

Bill, the Test 4 section seems to have “miilions” which should be “billions” in a number of places.

Intending to get to your Glasgow gig.

The six tests seem to have been drawn up, rather in the manner of Gordon Brown’s five tests for the UK (not) joining the Eurozone.

The intention seems to me transparent. To prevent the establishment of a new Scottish currency and thus to cripple any prospect of independence being successful. Presumably Scotland is expected then to crawl back in to the Union like a whipped dog saddled with huge bank loans that can only be settled by selling off yet more of the public estate to the private sector.

After the adoption of Amendment D, to adopt currency ASAP, the case must now be made that the establishment of the currency will in reality define what is the Day One of independence. The six tests thus become totally superfluous…or do I mean redundant.

Anything else is Brigadoon.

You have a tough anti-spam question for an economics blog.

Looking forward to hearing you in Edinburgh tonight.

Simple question.

Surely a Scottish government would only need to ALLOW that tax could be paid in Scottish pounds? No need to REQUIRE it. If the Scottish pound fell below the English pound then anyone would convert their English pounds to Scottish pounds before paying.

Or, maybe Brigadoom.

@Andrew (Andy) Crow

“The intention seems to me transparent. To prevent the establishment of a new Scottish currency and thus to cripple any prospect of independence being successful”.

“I can’t see their motivation as being so clever, devious or cunning as that. Surely, the reality is that they’re just too obtuse, too self-brainwashed, ever to be able to see – let alone admit that they see – any merit whatsoever in MMT’s analysis of how a modern monetary system works.

If that is so, they would not be one wit different from the vast majority of economists and other mouthpieces for orthodoxy and received wisdom. (Just like Jeremy Corbyn’s economic advisers and – maybe – even John McDonnell too, on the Left, and our revered Chancellor of the Exchequer on the Right).

Deliberate intent to sabotage needn’t be suspected, I suggest, only purblind folly born of wilfull ignorance. I’m not sure which is more culpable.

So, to post my comment, I had to answer the math equation 3+9.

I answered 12, and received the message wrong answer

I thought, after all it is an economics blog ,and left it.

Then the comment appeared after all

It has to be be an economics blog

I reckon, that if Scotland establishes its own currency, it should keep the English Sovereign’s image on the coin. Then you would be walking around with a sporran full of Sassenach heads. Och aye!