The IMF and the World Bank are in Washington this week for their 6 monthly…

Japan again demonstrates basic errors in mainstream macroeconomic theory

It is Wednesday and a quite blog writing day for me. I have to catch a flight a bit later and finish some other things before I do that. But I receive a lot of E-mails from readers puzzled by the fact that the low-interest rate environment (even negative) has not stimulated economic activity to the point of accelerating inflation. As part of the paradigm shift that is now, finally, occurring in macroeconomic policy-making, the RBA governor Phillip Lowe continued his theme that monetary policy has basically exhausted its counter-stabilisation potential, when he made his – Remarks at Jackson Hole Symposium (August 25, 2019). He talked about the “the elevated expectations that monetary policy can deliver economic prosperity” against the reality that central banks do not have “the best lever” to manage the economy. This theme has been expressed by many central bankers now. And there is emerging research to show that the low-interest rate environment is actually achieving the opposite – reducing the inflationary pressures. This is no surprise to Modern Monetary Theory (MMT) economists. Our basic presumption is that monetary policy is an ineffective tool for modifying aggregate spending and that rising interest rates, which are designed to quell inflationary pressures, probably actually intensify those pressures through their impact on business costs. Today, I will briefly discuss a paper I read yesterday that adds to the growing research evidence on this theme.

Negative Interest Rates and Inflation Expectations in Japan

In early November, I am doing a speaking tour in Japan. As regular readers will know I have a particular interest in Japan because I consider it to be the clearest real-world example of why mainstream macroeconomics fails to provide an adequate understanding of how a modern moentary system operates.

In fact, I consider it ratifies many of the key insights of MMT in a real-world environment.

As part of my preparation for this tour I have been studying inflationary processes in Japan – to bring myself up to speed on any nuances I might have missed.

In that context, I was reading the latest FRBSF Economic Letter (2019-22) – Negative Interest Rates and Inflation Expectations in Japan – released by the Federal Reserve Bank of San Francisco on August 26, 2019.

The paper seeks to examine the impacts of negative interest rates, which the Bank of Japan introduced in 2016, on inflationary expectations.

They find that when the common perception that such a low interest rate environment would be expansionary and trigger rising inflation, which was the stated objective of the Bank when they introduced the policy, is wrong.

In fact, when the policy was introduced “market expectations for inflation over the medium term fell immediately”.

The latest data on inflation expectations demonstrate that the central bank policies are not having the desired effect.

New Keynesian suggest that prices are adjusted to accord with expected inflation. With rational expectations, the mainstream models predict that inflation will respond one-for-one with shifts in expected inflation.

The Bank of Japan has been trying to manipulate that ‘theoretical claim’ in real space through its QE and negative interest rate experiments.

I wrote about QE in Japan in this blog post – Bank of Japan’s QE strategy is failing (April 24, 2018).

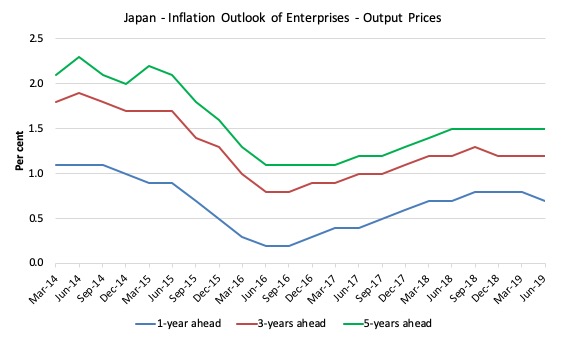

The following graph is taken from the – Tankan Summary of “Inflation Outlook of Enterprises – the latest data being released on Julyl 2, 2019, covering expectations up to June 2019.

Firms are asked to assess the future price movements in output prices and consumer prices.

The first graph shows the outlook for output prices – 1-year ahead, 3-years ahead and 5-years ahead.

While the longer-term expectations (3 and 5 years) are what we call firmly anchored (flat), the short-term expectations are now declining.

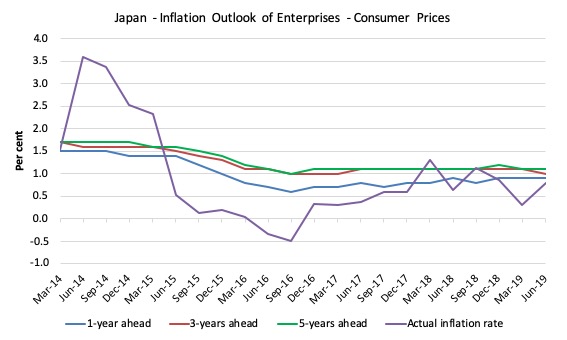

The second graph shows the outlook for consumer prices – 1-year ahead, 3-years ahead and 5-years ahead. It also includes the actual inflation rate (Purple line).

There is no inflationary pressure coming from expectations in Japan despite the monetary policy gymnastics.

The FRBSF research formally demonstrates that when inflationary expectations are “anchored at low levels”, negative interest rates will not act to stimulate activity or upward price movements.

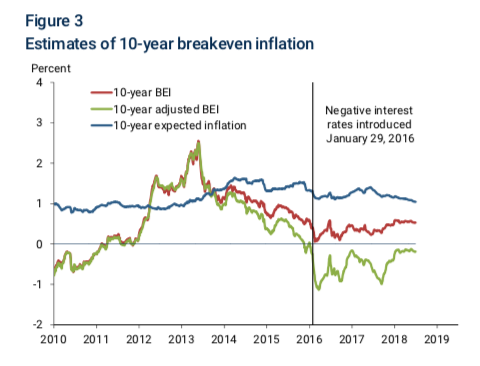

They use ‘market-based’ data – using “inflation-indexed bonds’ to examine the:

… difference between nominal and real yields of the same maturity, commonly known as the breakeven inflation (BEI) rate …

The BEI “is widely used to assess inflation expectations”.

So while the TANKAN data is the result of direct surveys of businesses, this method is indirect.

They make adjustments for “inflation risk premiums” and an “estimate of the value of deflation protection”.

The following graph (reproduced from their Figure 3) shows their “estimates of 10-year BEI rates and expected inflation, with the BEI estimates since 2013 adjusted for deflation protection”.

They conclude that:

… the estimate of 10-year expected inflation has been positive throughout but not very volatile. It drifted up modestly in 2013, as enthusiasm over the proposed Abenomics reform program spread. However, it drifted down again as pessimism over implementing the program began to emerge in 2014. Notably, inflation expectations immediately declined after the BOJ policy rate became negative, and dropped even lower at the end of our sample.

They try to explain this by arguing that “the market appeared to treat negative rates as bad news, perhaps because investors were concerned that the BOJ’s unprecedented move meant that economic conditions were worse than they thought.”

But that proposition is not substantiated in their paper.

The fact is that there is a strong demand for Japanese government bonds.

A lot of readers have asked me how can investors make money when yields are negative. The answer is complicated and involved factors such as the cost of exchange rate hedging and the difference between what is known as carry and roll.

For example, roll relates to moving down the slope of the yield curve. So if you hold a 10-year bond for a year, then it is a 9-year bond and if the curve is positively sloping then the yields will be lower and the price higher, so a capital gain is evident.

I will write more about that some other day.

For now, Japan once again demonstrates basic errors in mainstream macroeconomic theory.

The era of fiscal policy dominance is coming!

Call for financial assistance to make the MMT University project a reality

The – Foundation for Monetary Studies Inc. – aka The MMT Foundation serves as a legal vehicle to raise funds and provide financial resources for educational projects as resources permit and the need arises.

The Foundation is a non-profit corporation registered in the State of Delaware as a Section 501(c)(3) company. I am the President of the company.

Its legal structure allows people can make donations without their identity being revealed publicly.

The first project it will support is – MMTed (aka MMT University) – which will provide formal courses to students in all nations to advance their understanding of Modern Monetary Theory.

At present this is the priority and we need some solid financial commitments to make this project possible and sustainable.

Some sponsors have already offered their generous assistance.

We need significantly more funds to get the operations off the ground.

In order for FMS to solicit tax-exempt donations while our application to the IRS is being processed, the Modern Money Network, Ltd. (“MMN”) has agreed to serve as a fiscal sponsor, and to receive funds on FMS’s behalf.

MMN is a non-profit corporation registered in the State of Delaware, and is a federal tax-exempt public charity under Section 501(c)(3) of the Internal Revenue Code.

Donations made to MMN on behalf of FMS are not disclosed to the public.

Furthermore, all donations made to MMN on behalf of FMS will be used exclusively for FMS projects.

Please help if you can.

We cannot make the MMTed project viable without funding support.

Music for this morning …

When I moved out of my parent’s home in my teens, I shared a large old mansion in Melbourne with a large number of others – many who were musicians.

The great interpreter of Franz Liszt – Leslie Howard – was one of the original inhabitants with me, for example.

There was a lot of music played as you might expect.

And at that time, the first album by British band – King Crimson – came out.

I had first picked up on King Crimson the year before because they opened the Rolling Stones Hyde Park concert in July 1969.

That album – In the Court of the Crimson King – released in October 1969, but didn’t get to Australia until early 1970 – was on regular play list in our chaotic mansion, which we called the ‘Pink House’ because it was a rendered exterior painted pink (that fashionable colour in the 1930s or so.

I loved the sound of the Mellotron that was becoming popular during that period. I also loved listening to Robert Fripp’s guitar lines.

I regularly wheel out my old album and listen to it.

This track is a particular favourite – Epitaph. You only get the first half here because of YouTube licensing rules (I understand) and Robert Fripp’s protective attitude to the band’s old library.

Greg Lake on vocals is superb. But the guitar and mellotron are magical to my ears.

Oh the memories of a chaotic youth!

If you are in Melbourne tonight and want to hear some live music …

Then my band – Pressure Drop – is playing at the Maori Chief Hotel, 117 Moray St, South Melbourne, from about 20:00 to late.

This is a great little inner city pub in Melbourne which has consistently supported live music. Such venues need the support of all of us.

And, what else is there to do on a Wednesday night in Melbourne anyway?

Lots of great dub, rock steady and reggae coming up tonight. We will throw some jazz in there somewhere too!

I can also discuss Modern Monetary Theory (MMT) during breaks in the sets!

That is enough for today!

(c) Copyright 2019 William Mitchell. All Rights Reserved.

Jazz and MMT. What more could one ask for 🙂

Wow-you shared a house with Leslie Howard-an extraordinary musician. I remember him giving a great radio talk about Liszt and how he was the intermediary stage between Haydn and Bartok -a great musician and great thinker about music.

Must have been interesting days to say the least!

“For example, roll relates to moving down the slope of the yield curve. So if you hold a 10-year bond for a year, then it is a 9-year bond and if the curve is positively sloping then the yields will be lower and the price higher, so a capital gain is evident.”

Ignoring transaction costs, you will earn the initial 12 month rate on your portfolio if you hedge the position. Under such conditions of no arbitrage, a nine year bond one year forward will have the same value at expiry of that year as its initial value. Your profit/loss is the interest received/paid over that time, at the initial 12 month rate, on the money you have invested/borrowed.

Plus/minus any amounts because the hedge was wrong!

This is the “no free lunch rule”. A 12 month position will earn the 12 month rate on own funds invested. If you borrow these funds, net interest paid/received will be nil.

Bill, have never bothered to read your musical offerings but I just caught the name ‘Lizst’. Respect.

I have read the “Remarks at Jackson Hole Symposium” of Governor Philip Lowe.

The stand-out point (that you also emphasise) is that monetary policy has limitations that are more and more apparent in the current economic climate. Governor Lowe links this to the manifestation of the global economy.

He equates the global role of trade with (among other things) the difficulty in maintaining full employment; indeed we may only have started along the tumultuous path that is taking developed economies from mass manufacturing to all manner of alternative occupations and investments.

MMT’s Job Guarantee is seen as an antidote to this upheaval. But can it operate with sufficient flexibility to meet a range of demands that are only now becoming appreciated. Whilst it may prove adaptive to the infrastructural and social demands that are placed upon it, how successfully can it pursue this socially biased theme in the face of other burgeoning trading nations raising their comparative living standards at rapid rates.

Some sovereign states may be able to adjust to a self-contained existence so that international trade is able to be reduced, but there will still be strains on society as employment adopts to a new industrial/service structure, in which large swathes of employment may have to adjust to less buoyant prospects.

Historically, unemployment disruption has been attributed to a large extent on the workings of an indefinable market place. It will however, be much easier to blame unrest onto a government-determined economy.

That is why Governor Lowe’s reference to the importance of imparting a meaningful message to the population of a country is so significant.