It was only a matter of time I suppose but the IMF is now focusing…

China slowdown highlights the madness of the Eurozone austerity

Last Friday (October 18, 2019), the GDP data for China was released and we learned that growth has slowed quite significantly. The ABC news report – China’s economy hits three-decade low, with GDP growth falling to 6pc – suggested that this is the “fifth consecutive quarter of slowing growth” and a fall of 0.2 points from the last release. Its trade accounts reveal slower exports growth, and, importantly, slower import growth as growth in domestic demand declines. That last fact should raise fears of recession for the Eurozone elites, who have been content to export their austerity bias and rely on spending within other nations (outside the Eurozone) to maintain the weak growth that we have witnessed. The chickens are coming home to roost at present and the irony of all this is that ultimately German and Dutch external surpluses will fall below the allowable EU imbalance threshold of 6 per cent of GDP, not because those nations are doing anything sensible to address their damaging stance, but, rather, because their economies have become dependent on export growth and with China slowing that will hurt them badly. In other words, they will only come back within the EU laws through domestic recessions, and then, their fiscal positions will come under scrutiny again. A crazy system.

Reuters article – Six warning lights flashing for China’s slowing economy – provides several activity measures to show the longer term decline in economic growth.

Gone are the days of 14 per cent growth rates that China was achieving just before the GFC.

Why this is significant is because it exposes the madness of the austerity bias that the Eurozone has inflicted on its Member States and the continuing hypocrisy of its so-called adherence to ‘rules’.

The Germans like to tell us that “alles in Ordnung” and on March 19, 2019, joined with Belgium to propose an annual rule of law review for all Member States as an additional piece of bureaucratic oversight on Member State freedom, which appears unnecessary given Article 7 in the Treaty.

The German State Secretary was quoted as saying that the rule would be based on “objective criteria” and would (Source):

… not apply only to two or three member states but all of them.

Except, if the Member State is Germany and certainly not with respect to ‘objective criteria’ such as statistics published by national statistics agencies (or Eurostat) against procedures spelt out in European law.

Then, anything seems to be acceptable to the European Commission.

But everything is certainly not in order!

Recall my recent blog post – Leading indicators are suggesting recession (October 3, 2019) – which drew on the latest PMI survey data to reveal a very bleak outlook for Germany.

I concluded that while the trade disruptions are implicated, the irresponsible policy position of the German government (refusal to run fiscal deficits) and the European Union overall is exacerbating the external weakness.

Germany is especially reliant on external conditions, given its suppression of domestic demand. It is now paying the price of that imbalanced growth strategy.

On the – National Accounts loading page – of DeStatis (Statistisches Bundesamt) there were several items listed under “Press Releases”.

The following graphic captured them.

As a note, the August 19, 2019 entry about Manufacturing output has now been overtaken by events as I explained in the PMI survey blog cited above.

Fiscal surplus – GDP contraction – decline in economic performance.

But alles in Ordnung!

The following facts are obtained from the latest German National Accounts data for the second-quarter 2019:

1. Output fell by 0.01 per cent.

2. Exports fell by 1.35 per cent, which was partially offset by the decline in imports of 0.3 per cent.

What the data is telling me is that Germany’s plan to squeeze its Eurozone partners of growth by maintaining that fiscal rules have to be adhered to at all costs and then rely on growth in export markets elsewhere (such as China) is a difficult strategy to maintain.

I updated my balance of payments data today.

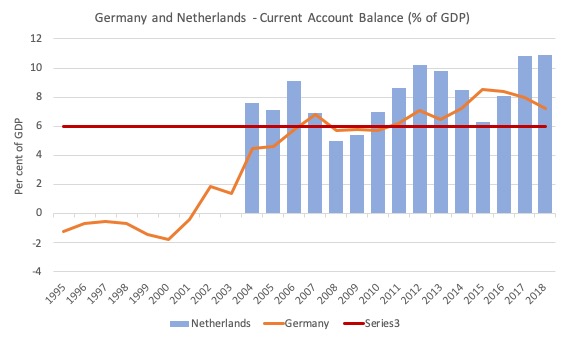

Consider the following graph, which shows the annual current account positions for Germany and the Netherlands from 1995 to 2018 (Eurosat data for Netherlands begins 2004).

The horizontal red line is the upper limit allowed under the rules laid out in the European Commission’s – Excessive imbalance procedure – which specifies a maximum external surplus of 6 per cent.

As I have explained before this is an arbitrary threshold designed to give Germany (and other nations such as Luxembourg, Austria, the Netherlands, etc) some room to move, given their growth strategy has been predicated on running external surpluses since the GFC.

I will come back to the question of imbalance presently.

The graph shows that in 2018, Netherlands recorded an external surplus of 10.9 per cent and it has been consistently above the EU’s maximum surplus.

Germany recorded an external surplus of 7.2 per cent, slightly down from the 8.5 Per cent it recorded in 2015. It also has been consistently in violation of EU rules in this regard.

The latest quarterly data shows that in the second-quarter 2019, the Netherlands recorded an external surplus of 6.6 per cent, so well down – it is clearly being affected by the trade disruptions.

Germany, however, maintained an external surplus of 7.1 per cent, and this was down from 7.9 per cent of GDP in the first-quarter 2019.

So still a massive deflationary force for the rest of the world but a sign that the slowdown in its domestic economy is coming from the slowdown in exports noted above.

I outlined the macroeconomic imbalance procedure in this blog post – Greece “neither thrived nor struggled” – the financial press alt world (December 31, 2018) – see also the links within that post to earlier analysis of the situation.

The EU Home Page describes the:

… enhanced surveillance mechanism to ensure compliance with the macroeconomic imbalance procedure that can be activated for countries identified with excessive imbalances …

Euro area Member States that repeatedly fail to submit corrective plans considered sufficient by the Council or to implement them face the possibility of sanctions, including fines.

Note: possibility condition, which we interpret according to history as meaning:

(a) If the nation is Greece, or, more recently Italy, the possibility increases to near certainty.

(b) If the nation is Germany or the Netherlands, eyes look the other way.

It is clear that Germany’s dominance in the Eurozone both politically and economically means it can force the adjustment to overall ‘unsustainable’ external positions onto both its own citizens (lowering their material living standards), and, more obviously, onto citizens of other EMU nations.

But then it relies on growth, for example, in China to maintain its export position.

Further, if all EMU nations followed Germany’s lead – then there would be mass Depression throughout Europe.

While the architecture of the monetary union is flawed at its most elemental level – these nations should never share a currency – the fact that Germany has crafted a strategy based on the immiseration of its Eurozone partners makes it more vulnerable to crises.

The Single Market. Le marché unique. Der Binnenmarkt. Somehow, even progressives eulogise the concept.

But this massive imbalance is what it has created and the ‘imbalance procedure’ has failed to discipline the consistent violation of Germany, the Netherlands, and Denmark of the EU rules.

Violations of the imbalance rules trigger “the alert mechanism report (AMR)” – the latest being issued on November 21, 2018 – 2019 European Semester: Alert Mechanism Report.

But while there are words about the violations nothing ever gets done.

In the blog post cited above – Greece “neither thrived nor struggled” – the financial press alt world (December 31, 2018) – provided a detailed account of what the German and Dutch surpluses mean for the rest of Europe.

The summary points are:

1. The persistent German and Netherlands’ current account surpluses drain spending from elsewhere in the Eurozone.

2. Then fiscal surpluses further exacerbate the spending drain.

3. The causal links between these balances is clear. By suppressing domestic demand – public and private consumption and capital formation investment – through its attacks on wages growth and fiscal austerity, the surplus nations also stifle imports.

4. The surpluses lead to an accumulation of financial claims against the rest of the world.

5. If a Member State achieve a balanced fiscal outcome and is sitting on the current account surplus threshold (6 per cent), then its private domestic sector will be saving overall 6 per cent of GDP.

6. Those savings have not gone into the domestic economy of Germany, for example because the lack of domestic demand has suppressed profitable investment opportunities. As a result capital sought profits elsewhere.

7. So by deliberately constraining the standard of living of its citizens and undermining its own public and private infrastructure, the surplus nations also damaged their EMU partners.

How? The lack of demand for their exports and the provision of surplus nation savings leads to external deficits, which drain demand from the domestic economy.

To maintain high levels of employment, these partner nations have to run higher fiscal deficits, which then come up against the EU fiscal rules.

And the imposition of the austerity bias then means that these nations have below capacity growth, elevated levels of unemployment and underemployment, degraded public infrastructure, and are always in danger of a fiscal crisis if bond markets get skittish.

It is no way to run a monetary union.

Conclusion

The irony of all this is that ultimately German and Dutch external surpluses will fall below the allowable imbalance threshold of 6 per cent of GDP not because those nations are doing anything sensible to address their damaging stance, but, rather, because their economies have become dependent on export growth and with China slowing that will hurt them badly.

In other words, they will only come back within the EU laws through domestic recessions, and then, their fiscal positions will come under scrutiny again.

A crazy system.

And the Remainers in Britain think it is the exemplar of progressivism.

That is enough for today!

(c) Copyright 2019 William Mitchell. All Rights Reserved.

Spot on; thanks Bill – will share.

You may read posts from Brad Sester; he has been focusing for long on global imbalances and problem of surplus counties

Great article.

problems of the Eurozone clearly laid out.

So the Euro locks deficit nations into a perpetual stop-go cycle, to which you add an austerity bias to make it permanent stop.

The surplus nations suppress domestic consumption and wages, export their excess production, accumulate financial claims against the rest of the world and fall off a cliff if non-EU imports drop.

Nice system