Today (April 18, 2024), the Australian Bureau of Statistics released the latest - Labour Force,…

US labour market – strong improvement but for how long?

Last Friday (April 2, 2021), the US Bureau of Labor Statistics (BLS) released their latest labour market data – Employment Situation Summary – March 2021 – which showed that the recovery since the catastrophic labour market collapse in March and April 2020, which had stalled in recent months, has got back on track as States open up their economies. Payroll employment growth was very strong and the unemployment rate fell by 0.2 points to 6 per cent. The broader labour wastage captured by the BLS U6 measure fell by 0.4 points to 10.7 per cent. Whether the vaccination process in train allows businesses to remain open is an unknown at present. Time will tell.

Overview for March 2021:

- Payroll employment increased by 916,000.

- Total labour force survey employment rose by 609 thousand net (0.41 per cent).

- The seasonally adjusted labour force rose by 347 thousand (0.22 per cent).

- Official unemployment fell by 262 thousand to 9,710 thousand.

- The official unemployment rate fell by 0.2 points to 6.9 per cent.

- The participation rate rose by 0.1 points at 61.5 per cent.

- The broad labour underutilisation measure (U6) fell by 0.4 points to 10.7 per cent.

For those who are confused about the difference between the payroll (establishment) data and the household survey data you should read this blog post – US labour market is in a deplorable state – where I explain the differences in detail.

BLS explanation of COVID effects on data

The BLS say:

As in previous months, some workers affected by the pandemic who should have been classified as unemployed on temporary layoff were instead misclassified as employed but not at work. However, the share of responses that may have been misclassified was highest in the early months of the pandemic and has been considerably lower in recent months. Since March 2020, BLS has published an estimate of what the unemployment rate might have been had misclassified workers been included among the unemployed. Repeating this same approach, the seasonally adjusted unemployment rate in March 2021 would have been 0.4 percentage point higher than reported. However, this represents the upper bound of our estimate of misclassification and probably overstates the size of the misclassification error.

So we are now operating in an environment of minimal uncertainty.

Payroll employment trends

The BLS noted that:

Total nonfarm payroll employment increased by 916,000 in March but is down by 8.4 million, or 5.5 percent, from its pre-pandemic peak in February 2020. Job growth in March was widespread, with the largest gains occurring in leisure and hospitality, public and private education, and construction.

In March, employment in leisure and hospitality increased by 280,000, as pandemic-related restrictions eased in many parts of the country … Employment in leisure and hospitality is down by 3.1 million, or 18.5 percent, since February 2020 …

In March, employment increased in both public and private education, reflecting the continued resumption of in-person learning and other school-related activities in many parts of the country … Employment is down from February 2020 in local government education (-594,000), state government education (-270,000), and private education (-310,000).

Construction added 110,000 jobs in March, following job losses in the previous month (-56,000) that were likely weather-related … Employment

in construction is 182,000 below its February 2020 level.Employment in professional and business services rose by 66,000 over the month but is down by 685,000 since February 2020 …

Manufacturing employment rose by 53,000 in March … is down by 515,000 since February 2020.

Transportation and warehousing added 48,000 jobs in March …

Employment in the other services industry increased by 42,000 over the month … . is down by 396,000 since February 2020.

Social assistance added 25,000 jobs in March … is 306,000 lower than in February 2020.

Employment in wholesale trade increased by 24,000 in March … is 234,000 lower than in February 2020.

Retail trade added 23,000 jobs in March … is 381,000 below its February 2020 level.

Employment in mining rose by 21,000 in March … is down by 130,000 since a peak in January 2019.

Financial activities added 16,000 jobs in March … has 87,000 fewer jobs than in February 2020.

Employment in health care and information changed little in March.

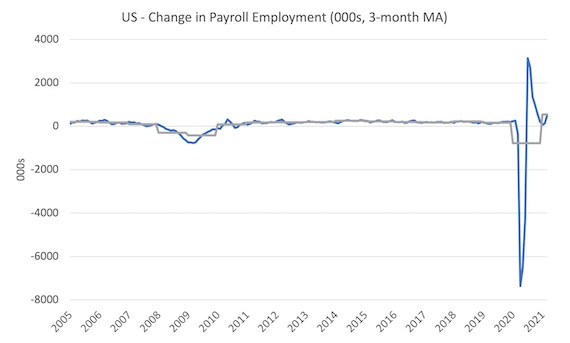

The first graph shows the monthly change in payroll employment (in thousands, expressed as a 3-month moving average to take out the monthly noise). The gray lines are the annual averages.

The data swings are still large and dwarf the past history.

Clearly, the 916,000 jobs gain (net) in March is a massive improvement as States eased restrictions on what could be open.

But the US labour market is still 8.4 million jobs short from where it was at the end of February 2020.

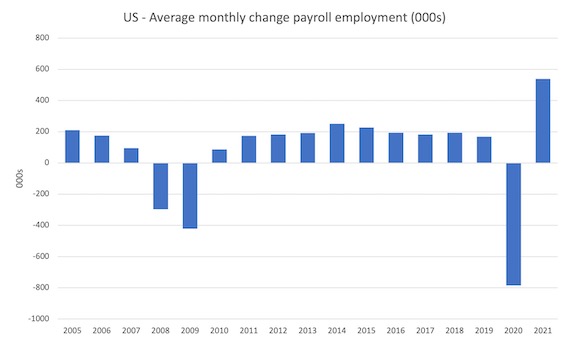

The next graph shows the same data in a different way – in this case the graph shows the average net monthly change in payroll employment (actual) for the calendar years from 2005 to 2020 (the 2020 average is for the months to date).

The final average for 2019 was 168 thousand.

The final average for 2020 was -785 thousand.

The average for 2021 (so far) is 589 thousand.

Labour Force Survey – employment growth positive

The data for December reveals:

1. Employment as measured by the household survey rose by 609 thousand net (0.41 per cent).

2. The labour force rose by 347 thousand (0.22 per cent).

3. The participation rate rose by 0.1 points to 61.5 per cent.

4. As a result (in accounting terms), total measured unemployment fell by 262 thousand to 9,710 thousand and the unemployment rate fell from 6.2 per cent to 6 per cent.

The BLS note that both unemployment measures:

The unemployment rate edged down to 6.0 percent in March. The rate is down considerably from its recent high in April 2020 but is 2.5 percentage points higher than its pre-pandemic level in February 2020.

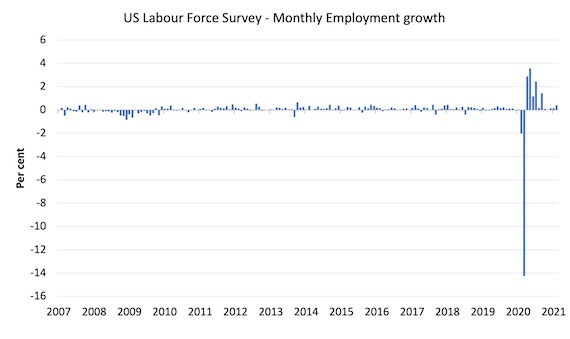

The following graph shows the monthly employment growth since January 2008, which shows the massive disruption this sickness has caused.

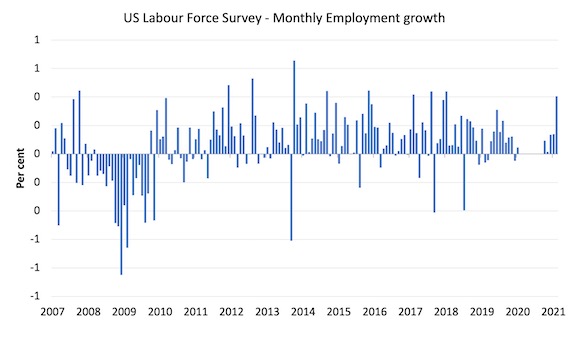

To put the recent period in perspective I took out the extreme observations (outliers) between March 2020 and October 2020 and repeated the graph.

This graph shows the current recovery more realistically.

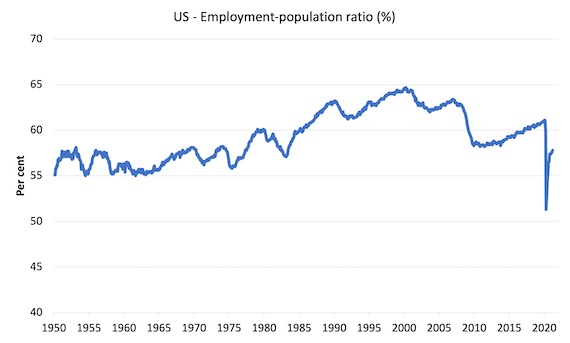

The Employment-Population ratio is a good measure of the strength of the labour market because the movements are relatively unambiguous because the denominator population is not particularly sensitive to the cycle (unlike the labour force).

The following graph shows the US Employment-Population from January 1950 to March 2021.

While the ratio fluctuates a little, the April 2020 ratio fell by 8.6 points to 51.3 per cent, which is the largest monthly fall since the sample began in January 1948.

In March 2021, the ratio rose by 0.2 points to 57.8 per cent.

It is still well down on the level in February 2020 (61.1 per cent).

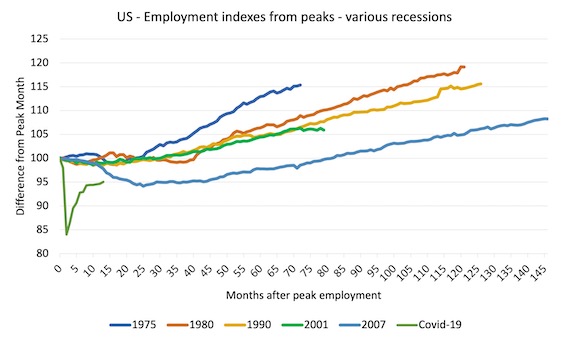

As a matter of history, the following graph shows employment indexes for the US (from US Bureau of Labor Statistics data) for the five NBER recessions since the mid-1970s and the current 2020-COVID crisis.

They are indexed at the employment peak in each case and we trace the data out for each episode until one month before the next peak.

So you get an idea of:

1. The amplitude (depth) of each cycle in employment terms.

2. The length of the cycle in months from peak-trough-peak.

The early 1980s recession was in two parts – a short downturn in 1981, which was followed by a second major downturn 12 months later in July 1982 which then endured.

Other facts:

1. Return to peak for the GFC was after 78 months.

2. The previous recessions have returned to the 100 index value after around 30 to 34 months.

3. Even at the end of the GFC cycle (146 months), total employment in the US had still only risen by 8.3 per cent (since December 2007), which is a very moderate growth path as is shown in the graph.

The current collapse is something else recent gains are evident.

Unemployment and underutilisation trends

The BLS report that:

The number of unemployed persons, at 9.7 million, continued to trend down in March but is 4.0 million higher than in February 2020.

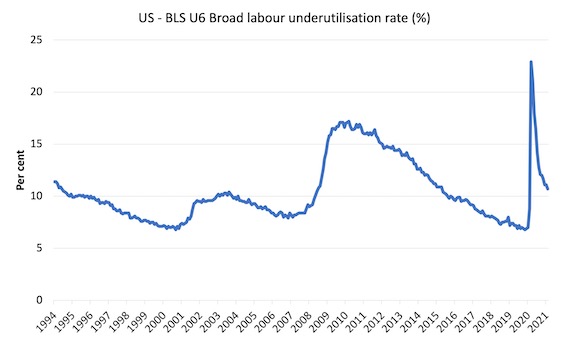

The first graph shows the official unemployment rate since January 1994.

The official unemployment rate is a narrow measure of labour wastage, which means that a strict comparison with the 1960s, for example, in terms of how tight the labour market, has to take into account broader measures of labour underutilisation.

The next graph shows the BLS measure U6, which is defined as:

Total unemployed, plus all marginally attached workers plus total employed part time for economic reasons, as a percent of all civilian labor force plus all marginally attached workers.

It is thus the broadest quantitative measure of labour underutilisation that the BLS publish.

In December 2006, before the effects of the slowdown started to impact upon the labour market, the measure was estimated to be 7.9 per cent.

In March 2021 the U6 measure was 10.7 per cent, a decline of 0.4 points.

The part-time for economic reasons cohort (the US indicator of underemployment) fell by 262 thousand (4.3 per cent).

The BLS say that:

The number of persons employed part time for economic reasons, at 5.8 million, changed little in March but is 1.4 million higher than in February 2020. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs …

The number of persons not in the labor force who currently want a job was about unchanged at 6.9 million in March but is up by 1.8 million since February 2020. These individuals were not counted as unemployed because they were not actively looking for work during the last 4 weeks or were unavailable to take a job …

Among those not in the labor force who currently want a job, the number of persons marginally attached to the labor force, at 1.9 million, was essentially unchanged in March but is up by 416,000 since February 2020. These individuals wanted and were available for work and had looked for a job sometime in the prior 12 months but had not looked for work in the 4 weeks preceding the survey. The number of discouraged workers, a subset of the marginally attached who believed that no jobs were available for them, was 523,000 in March, essentially unchanged from the previous month.

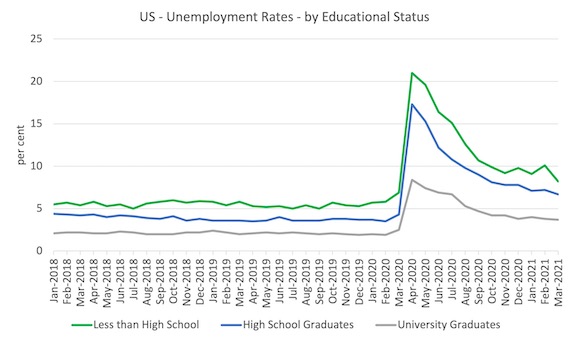

Ethnicity and Education

The next graph shows the evolution of unemployment rates for three cohorts based on educational attainment: (a) those with less than high school completion; (b) high school graduates; and (c) university graduates.

As usual, when there is a crisis, the least educated suffer disproportionately.

In the collapse in employment, the unemployment rates rose by:

- 14.1 points for those with less than high-school diploma.

- 13.0 points for high school, no college graduates.

- 5.9 points for those with university degrees.

The period since April 2020 has seen the unemployment rate fall by:

- 12.8 points for those with less than high-school diploma meaning the unemployment rate is now 3.8 points above the March level.

- 10.16 points for high school, no college graduates meaning the unemployment rate is now 4.6 points above the March level.

- 4.7 points for those with university degrees meaning the unemployment rate is now 2.3 points above the March level.

In the last month, the change in the unemployment rate has been:

- rise of 1.9 point for those with less than high-school diploma – so this cohort is bearing the cost of the stalled recovery.

- rise of 0.5 points for high school, no college graduates.

- fall of 0.1 points for those with university degrees.

In the US context, especially in the current time, the trends in trends in unemployment by ethnicity are interesting.

Two questions arise:

1. How have the Black and African American and White unemployment rate fared in the post-GFC period?

2. How has the relationship between the Black and African American unemployment rate and the White unemployment rate changed since the GFC?

Summary:

1. All the series move together as economic activity cycles. The data also moves around a lot on a monthly basis.

2. The Black and African American unemployment rate was 6.8 per cent in March 2020, rose to 16.7 per cent in May and is now down to 9.6 per cent in March 2021. In the last month, it fell by 0.3 points.

3. The Hispanic or Latino unemployment rate was 6 per cent in March 2020, rose to 18.9 per cent in April and fell to 7.9 per cent in March 2021. In the last month, it fell 0.3 points.

4. The White unemployment rate was 3.9 per cent in March 2020, rose to 14.1 per cent in April and fell to 5.4 per cent in March 2021. In the last month, it fell 0.6 points.

So the improvement in the labour market in the last month has been mostly because by Black and African Americans and Hispanic and Latino employment has improved relatively.

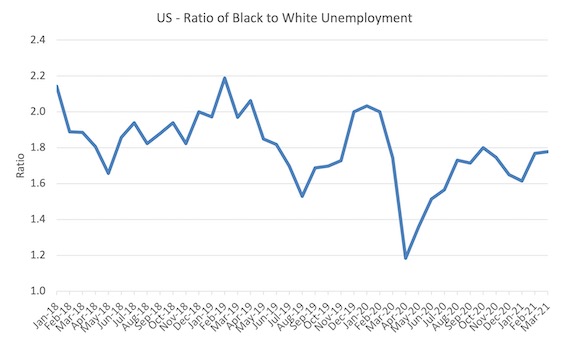

The next graph shows the Black and African American unemployment rate to White unemployment rate (ratio) from January 2018, when the White unemployment rate was at 3.5 per cent and the Black or African American rate was at 7.5 per cent.

This graph allows us to see whether the relative position of the two cohorts has changed since the crisis.

If it is rising, then the unemployment rate of the Black and African American cohort is either rising faster than the white unemployment rate or falling more slowly (or a combination of that relativity).

While there is month-to-month variability, the data shows that, in fact, through to mid-2019, the position of Black and African Americans had improved in relative terms (to Whites), although that just reflected the fact that the White unemployment was so low that employers were forced to take on other ‘less preferred’ workers if they wanted to maintain growth.

In April 2019, the ratio was 2.1 (meaning the Black and African American unemployment rate was more than 2 times the White rate).

By April 2020, the ratio had fallen to its lowest level of 1.2, reflecting the improved relative Black and African American position.

As the pandemic hit, the ratio rose and peaked at 1.8 in October 2020.

In March 2021, the ratio was 1.78 rising from 1.61 in January.

Conclusion

The March 2021 US BLS labour market data release reveals that the recovery since the catastrophic labour market collapse in March and April 2020, which had stalled in recent months, has got back on track as States open up their economies.

Whether the opening is sensible given the trajectory of the virus is another question but perhaps the increasing vaccine coverage will prevent further closures.

The US labour market is still 8.4 million jobs short from where it was at the end of February 2020.

The employment bounce-back this month was impressive but not surprising given the nature of the employment loss in the first place.

What happens in the coming months will, I think be dictated by the battle between the speed and efficasy of the vaccination process and the speed of the virus infection.

That is enough for today!

(c) Copyright 2021 William Mitchell. All Rights Reserved.

“What happens in the coming months will, I think be dictated by the battle between the speed and efficacy of the vaccination process and the speed of the virus infection.” Surely so. But what happens in the coming years, on the other hand, not only in the U.S. but across the world, will be dictated by the battle between those who view the pandemic as something to be put behind us ASAP so that we might return to the oppressive, imperialist, ecocidal neoliberal world order, and those who view the pandemic as a warning, perhaps our last opportunity before impending civilizational collapse, to reassess and alter our way of life so as to move in a better direction socially, economically, and environmentally. Given the global stranglehold of neoliberalism and imperialism, radiating from it maximized position in the U.S., such reassessment and alteration, if they occur, will of necessity be a gradual, incremental process, beginning with baby steps. Thus, I have become increasingly turned off by voices, especially on the radical left, who malign any small step taken in the right direction as a cowardly betrayal of the larger vision of a better, more beautiful world. The eating of our own, a specialty of the left from its beginning, has never been more counterproductive than it is right now.

In California, our cases are way down. What i am concerned with is a potential variant that is resistant to the vaccine.

People need to keep wearing their masks.

@Newton Finn

Who are these radical left? Can you name some names?

Well. If they call themselves radical then the least they can read something if they can’t think themselves.

Tom, naming names would simply add to the “eating.” All you need to do is go on YouTube, for example, and search for AOC’s recent comments on the border situation or her position on whether “withholding the vote” would have been the best strategy to move America closer to M4A. She may well be wrong on both issues, and that needs to be debated, but just look at what’s been said about her by some prominent voices in the progressive left. Similar examples abound concerning other Democrat officials and proposals, from Joe Biden on down. I agree with the substance of most of these criticisms, by the way, but the tone is lethal IMHO when it comes to uniting the left and broadening its base.

Maybe I am missing something but isn’t the standard of living in America at record highs? Isn’t the stock market, one measure of wealth, hitting record highs? Isn’t both fiscal and monetary policy responding to the impact of the virus? And with all this stimulus, inflation remains remarkably low. The new president has welcomed the impoverished people from Central America into the U.S. and is attempting to spend billions of dollars to help central American governments to encourage their citizens to remain in their countries. Isn’t this one level up from offering everyone a job? Given all of the innovations that are making life easier and more beautiful around the world, I don’t see the writing all the wall that says: “Armageddon.”

Tom Nugent, I’m sorry but I can’t tell if you are perhaps being sarcastic or are actually very optimistic.

I mean the US is still clearly in a health crisis and has economic problems due to that, and many that pre-date the pandemic. There are reasons to be optimistic for sure, but the standard of living of Americans is not at the moment at an all time high. And that the US has suddenly begun welcoming impoverished Central Americans would be news to me. I mean possibly we are not putting so many in cages may be true but I am not even sure of that. What source do you base this observation on?

The stock market may have been doing well, which is great for people who own stocks, but the vast majority of the benefit of that goes to the already wealthy rather than the average American worker.

I would admit that US fiscal policy has responded to the pandemic a lot better than what I would have expected from our government previously. And while I am optimistic that the US is not a complete failure as a nation, there are still many serious problems here that need to be recognized and addressed.

@Newton Finn,

Okay. Thanks!

Nugent’s comment is good one.