It's Wednesday and today I consider the current yen situation which is causing some hysteria…

Video of presentation for Wattle Partners – October 15, 2021

Last week, I did a seminar with a Melbourne financial market group (Wattle Partners), who I regularly help in their education programs. It took the form of an informal (somewhat structured) conversation about Modern Monetary Theory (MMT) and more practical applications of the MMT understanding. There were several questions from the audience that we didn’t get time to answer in the allotted time so today I am honouring my agreement to provide answers, which might be of interest to the broader readership, if only to reinforce knowledge. The video of the interaction is also available now and you can watch it here.

Video – Market Thinkers Season Three, #2 – Professor William Mitchell from MMTed, October 15, 2021

Here is the video of that briefing.

It runs for just over an hour.

Thanks to Drew and Jamie for the questions and the on-going interest in MMT.

There were some questions posed by the audience which we didn’t have time to deal with in the hour allotted.

So here are some brief answers.

Q1: If MMT is implemented, what to stop politicians, who are already corrupted, from a spending binge for their own self interests? How should we hold governments responsible?

First, Modern Monetary Theory (MMT) is not implemented, it is.

We should think of MMT as a lens, which allows us to better understand the functions of the fiat monetary system and the capacities of the currency-issuing government within that system and the consequences of using that capacity in one way or another.

This is not the same thing as saying that MMT is purely descriptive, which I sometimes read and hear people saying.

When I introduced the notion of MMT being a superior lens to allow people to achieve a better understanding of the way the monetary system work, the operative word is ‘understanding’.

That goes beyond description. Understanding requires an appreciation of causal processes, which, in turn, requires theorising.

Thus, it is important to note that MMT should not been seen as a regime that you ‘apply’ or ‘switch to’ or ‘introduce’.

I say it is a lens which allows us to see the true (intrinsic) workings of the fiat monetary system.

The lens helps us better understand the choices available to a currency-issuing government and the consequences of surrendering that currency-issuing capacity (as in the Eurozone).

And the lens lifts the veil imposed by different ideological positions and forces the real questions and political choices out in the open.

An MMT understanding means that statements such as the ‘government cannot provide better services because it will run out of money’ are immediately known to be false.

Such an understanding will change the questions we ask of our politicians and the range of acceptable answers that they will be able to give. In this sense, an MMT understanding enhances the quality of our democracies.

Second, there is nothing stopping our elected politicians doing anything except they have to face us every three years.

They already go on spending binges to suit their political interests – sports rorts, Gladys and Daryl, the car parks scandal, and all the rest of it.

We can only hold them responsible under our system through the ballot box and making sure the alternative government (in our case, the Labor Party) is fit for purpose.

Q2: Does all this mean there is no problem in the Chinese property market, (apart from individual debt) (see Evergrande). i.e the Govt can bail them out.

The Chinese government can certainly bail out Evergrande if it chooses to do so.

It issues its own currency and could guarantee the liabilities of any entity that has debts in that currency.

The same goes for the Australian government. It has the same capacity for any liabilities outstanding in Australian dollars.

Whether a currency-issuing government should ever bail out private companies is another question though.

There is no question they can in financial terms.

But the efficasy to society of doing that requires much more detailed assessment as to who benefits.

My guess is that the Chinese government will not allow the Evergrande situation become a major problem for them.

Q3: How should retirees use the MMT lens to help then create wealth?

Investment decisions require knowledge.

As I said at the outset of the presentation, my role is not to provide advice to people on how they can increase their wealth.

But if you invest using mainstream monetary theory then I believe you are going to achieve worse outcomes than if you take the time to really understand how the monetary system works.

You might like to read these blog posts, which explain basis principles that can help you achieve better outcomes:

1. Investors lose out following the advice of New Keynesian (mainstream) macroeconomics (July 12, 2021).

2. Making better investment decisions using MMT as a knowledge base (long) (July 13, 2020).

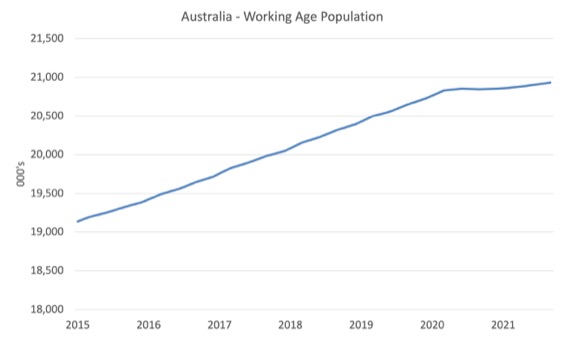

Q4: What effect will the huge drop in migration have on the economy?

I analyse population and labour force trends on a monthly basis the day the Australian Bureau of Statistics publishes the labour force data (typically the third Thursday of each month).

My most recent commentary was – Australian labour market continues to contract (October 14, 2021).

The following graph shows Australia’s working age population (Over 15 year olds) from January 2015 to September 2021.

With the external border closed, immigration has shrunk to virtually zero and the impact is very clear.

This flattening out has forced employers to work harder to get workers and is one of the reasons unemployment is falling quite quickly, given the circumstances.

It will also provide the conditions for workers to gain some wages growth after some years of stagnant nominal wages growth, which has often translated into real wage cuts.

Q5: What is the relationship between quantitative easing and inflation?

Quantitative easing merely involves the central bank buying bonds (or other bank assets) in exchange for deposits made by the central bank in the commercial banking system – that is, crediting their reserve accounts. In Australia, these accounts are called exchange settlement accounts.

The mainstream economists think that by creating excess reserves, the commercial banks will increase their loans to customers and stimulate the economy.

Proponents of quantitative easing claim it adds liquidity to a system where lending by commercial banks is seemingly frozen because of a lack of reserves in the banking system overall. It is commonly claimed that it involves “printing money” to ease a “cash-starved” system. That is an unfortunate and misleading representation.

They also believe that the extra ‘money’ in the system will cause inflation – the ‘too much money chasing too few goods’ narrative.

It is inappropriate to call this process – “printing money”. Commentators who use this nomenclature do so because they know it sounds bad! The mainstream economics approach uses the “printing money” term as equivalent to “inflationary expansion”.

However, this conception is based on the erroneous belief that the commercial banks need reserves before they can lend and that quantititative easing provides those reserves.

The illusion is that a bank is an institution that accepts deposits to build up reserves and then on-lends them at a margin to make money. The conceptualisation suggests that if it doesn’t have adequate reserves then it cannot lend. So the presupposition is that by adding to bank reserves, quantitative easing will help lending.

But this is a completely incorrect depiction of how banks operate.

Bank lending is not “reserve constrained”. Banks lend to any credit worthy customer they can find and then worry about their reserve positions afterwards. If they are short of reserves (their reserve accounts have to be in positive balance each day and in some countries central banks require certain ratios to be maintained) then they borrow from each other in the interbank market or, ultimately, they will borrow from the central bank through the so-called discount window. They are reluctant to use the latter facility because it carries a penalty (higher interest cost).

The point is that building bank reserves will not increase the bank’s capacity to lend.

In the real world, loans create deposits which generate reserves.

It is the reverse causality to that conceived by the mainstream textbooks.

There is no obvious relationship between QE and the inflation trajectory.

QE is really just an accounting adjustment in the various accounts to reflect the asset exchange. The commercial banks get a new deposit (central bank funds) and they reduce their holdings of the asset they sell.

That does suppress yields (and related lending rates) in the maturity range of the bonds being purchased.

And the lower investment rates might stimulate borrowing for capital formation, which, in turn, might push the nominal spending in the economy beyond the capacity of the economy to absorb it (in terms of available productive capacity).

But in a major recession, when QE has been most practiced, there is no real likelihood of the spending growth outpacing available capacity.

I wrote about the recent QE program in Australia in this blog post – Australian government issues debt, buys most of it itself, and then pays itself interest into the bargain (October 7, 2021).

Also, you might like to read the following blog posts, which bear on the subject:

1. Quantitative easing 101 (March 13, 2009).

2. British House of Lords having conniptions about QE – a sedative and a lie down is indicated (July 20, 2021).

3. The cat is progressively getting out of the bag – Part 1 (April 12, 2021).

4. The cat is progressively getting out of the bag – Part 2 (April 13, 2021).

5. Bond investors see through central bank lies and expose the fallacies of mainstream macroeconomics (January 6, 2021).

Q6: Speaking of Evergrande crisis, do you think that it might cause any contagion effect on the Australian economy, GDP growth and the Australian Property Market?

Evergrande would normally be poised to be a very large corporate default, given that it has failed to make a very large offshore bond payment, which comes due in deferral in the coming week.

It has substantial debts and it seems to be restructuring its business as quickly as it can (selling assets, providing inducements for sales, etc).

In ordinary times, the company would default given the scale of its liabilities.

But this is China and the times are not ordinary.

A recent – Speech and Q&A by Governor YI Gang at the 2021 G30 International Banking Seminar (he is the governor of the People’s Bank of China, its central bank) – made it clear that the Chinese government would not allow Evergrande to formally default.

He said:

Evergrande is a real estate developer. Right now, it probably cannot pay its debt, and some construction projects have been suspended. And there are uncertainties to delivering its pre-sold apartments on time. Those are the kind of risks we are facing. I think overall the Evergrande risk is an isolated case. And first we try to prevent the contagion to other real estate companies. Second, we try to prevent the contagion to other parts of the financial sector. Total liabilities of Evergrande are about 300 billion US dollars. Only one third of them are to the financial sector. In terms of liabilities to financial institutions, they spread across hundreds of institutions and are backed by collaterals. In general, the spillover of Evergrande’s risk to the financial sector is under control. The principle we try deal with this case is that the right and interest of creditors and property owners will be fully respected in strict accordance with the law. And also law has clearly indicated the seniority of those liabilities. And we try to protect consumers and home buyers rights. In the overall consideration, we will treat this case in strict accordance with law, put consumers’ right, home buyers’ rights pretty much at a higher priority, and treat all the creditors and related parties equally under the law. On the whole, we are confident that we can prevent the risk from spreading and avoid systemic risk.

If there is some form of managed default, then we might expect a fall in property prices, given the size of its portfolio, but I would need more detailed data before I would be prepared to comment further on that.

In general, I suspect Evergrande is too big to fail and the Chinese government will see it that way.

That doesn’t mean there will not be losses though.

Q7: Japan has very high household saving ratio. The Govt debt is mostly internal debt. The end is simply a redistribution of wealth.

There is no question that the Japanese government has mostly internal debt.

But that is not very relevant.

All the debt is issued in yen and so any foreign holders must transact in that currency, which the Japanese government issues as a monopolist.

In other words, the fact that most of the debt is held by Japanese resident interests is not something to dwell on.

The point is that the Japanese government can always meet their liabilities in yen.

Further, the bid-to-cover ratios are typically high in the bond auctions, so there is no shortage of demand for JGBs.

The central bank also has purchased all of the debt issued since 2012 (about) through secondary market transactions.

Interest rates remain close to zero and some long-term bond yields have been negative in recent periods.

The People’s Bank of China can always control yields by its secondary market transactions.

So there is no relationship that can be predicted between the bond yields and the scale of the debt, or interest rates in the broader financial markets.

In effect, the Japanese government runs a deficit, which puts more yen into the economy than the government takes out in the form of taxes.

That net yen injection increases net yen financial assets held by the non-government sector, that is, wealth increases.

The Government then offers a portfolio choice to wealth holders by issuing risk-free debt.

The funds to buy that debt came from the spending injection that was not taxed away by government (the deficit).

That is enough for today!

(c) Copyright 2021 William Mitchell. All Rights Reserved.

Thanks, Bill. Some useful confirmatory reading for an amateur like me.

Just one comment. I understood that QE has caused asset inflation in some developing countries, particularly in real estate. Could you please explain, if it is true, how that works.

It’s also not uncommon to see large swings in PPI that doesn’t materialize into CPI.

In fact, this happened from 2001-2008 during the big run up in oil and commodity prices and the producer prices didn’t get passed on in large part because aggregate demand was weak. Producers don’t make all of their products all at once. It’s a rolling process.

The discussion on debt reminds me of the matrix quote “don’t try to bend the spoon. Instead try to realise the truth….there is no spoon”

Seems like an analogous phrase about government debt….”don’t think about the government’s ability to repay their debt. Instead try to realise the truth…there is no debt”

I think the international private banking system is probably worth its own “box” in macroeconomics. That is basically a system that can create US dollar denominated financial assets in a similar way to a currency issuing government…..but there is very little public data about it which makes it hard to study…private bank lending/money creation from this “eurodollar” system has stopped accelerating since the gfc….its hard to tell if this is a cause of government deficits and stagnation or an effect…

I would like to rise here the question of description and understanding. Bill explains how understanding “goes beyond description”: “understanding requires an appreciation of causal processes, which, in turn, requires theorising”.

Firstly, how is it possible to theorise without description? Description is this part of scientific theory that can be verified. The generalising, sometimes philosophical part of scientific theory is that can be falsified. Only when a theory can be both verified and falsified it can be considered a scientific theory. Otherwise it will remain a speculation, an unproved hypothesis.

Secondly, what is theory? For me, theory is a model of a thing, of a phenomenon in reality. The method that we apply to create a model of a thing we study is itself a theory of how scientists theorise, how it is possible to theorise. These methods change and evolve in history of science, theoretical thinking is creative thinking. A theory, a model is always different from the thing that is modelled, and what this difference would exactly be is open until the theory is finally formulated.

I know many cases both in natural sciences and humanities where the method of creating a good and working, verifiable and falsifiable theory is a straightforward description. For example: the shape of Earth is not a regular sphere (and then the more precise description follows).

I completely agree that science should not be reduced to description. But I see that in contemporary social sciences the descriptive part is largely underrated.

Economy is a stochastic phenomenon like weather. In order to model a weather in a certain location we need systematic description of weather in that location and around it over a long time period. The same in economy. In many countries, now, all economic research is project based. Which research project gets funding and which not is itself a stochastic process. This is where this fictional world comes in that Bill talks about, to fill the void coming from the lack of description.

I have some issues with causality. Yes, there exists the definition of causality by David Hume but even scientist do not hold strictly to it. The old meme of causality indicating the direction of time, for example, is still there in spite of the fact that for more than century physicists have aligned the direction of time with the direction of entropy, not causality. And even following the definition by David Hume consistently, one should take seriously the warning by David Hume: a causal relation cannot be proved as a scientific theory, it would always remain, at best, a working hypothesis. It is a researcher’s mental exercise which of the two events is a cause and which an effect. Are enfants born because kings copulate or do kings copulate to produce enfants? How would historians set the causality here?

Another issue with causality is that when scientists define some kind of ’cause’ then it can start to live its own life and other scientists start to think whether the same ’cause’ has an effect on their object of research too. And when a ’cause’ is defined that explains successfully many phenomena, then researchers can become too lazy to look for other processes that effect their object of research. This kind of ’causes’ are especially dodgy in humanities because in our Christian tradition people have the analogy of god and devil who ’cause’ beneficial or malevolent processes just being a god and a devil. This is where the axes of evil and good come from in history. A ’cause’ is usually a simplified explanation.

I see the history of nature and society as process where all processes intertwine like in a cable. Some processes create other processes, some cancel other processes. Some processes interact, some not. After having described this kind of ‘cable’ of processes where the particular process that the scientist studies is part of, he can start to think which way to proceed to generalise his notes of observations and calculations into a theory, into a model of the process he or she studies.

I agree that ‘understanding’ is more than ‘describing’. What makes this difference, how to achieve this improvement from description to understanding is a matter of epistemology that does not give a set of fixed recipes. Epistemology, although largely neglected in contemporary philosophy, is itself a creative discipline.

One of the big moves in markets especially currency markets is with interest rate hikes and cuts.

The mainstream has the effects of interest policy backwards as well. The “herd ” following the mainstream view in general move currencies in the wrong direction. The fundamentals win through in the end.

When the FED started hiking interest rates in 2016 inflation was nothing barely registered on the graphs. 7 or 8 hikes later inflation touched 3%. By hiking they were causing inflation at the margins. Because the increased cost of borrowing got passed onto the consumer via higher prices. Via the interest income channels.

Warren explained it in the Huffington post – There Is No Right Time for the Fed to Raise Rates!

Via forward guidance by the FED the “herd” following the mainstream view sold gold all the way down from $1300 to $1050 because they thought the FED was going to fight inflation.

As soon as the FED started hiking gold went from $1050 to nearly $1500. The complete opposite to what the mainstream predicted. MMT’rs told everybody this would happen using the MMT lens.

At the same time when the FED started to hike. The ” herd” following the mainstream view shorted the GBP/ USD currency pair all the way down to around 1.2 due to Brexit. A frenzy of nonsense.

MMT’rs were saying because the FED was in rate hike mode and causing inflation at the margins the £ would get stronger. Early 2018 it was back up to 1.45.

All the central banks are about to make the same mistake again. New Zealand has already hiked which is a HUGE mistake. Somebody should have a chat with their central bank.

Will the ” Herd” following the mainstream view go the wrong way again like they did after 2008. Watch this space. My guess is the will the mainstream view has them hypnotised.

Russia, Argentina, Turkey, Mexico all made the same mistake. Noises come out of Turkey is they have learned from that mistake. Have other central banks who learned the hard way learned anything ?

Erdogan talked about to Bloomberg. You can find the links.

The interest rate debate is a debate worth having with Drew and Jamie. So many markets move in the wrong direction when central banks start talking about increasing interest rates.

I too am a bit confused by the assertion that MMT is an understanding not a description. An understanding is a relationship between a person and a subject. A description is a statement about a subject. Is MMT not a statement about money?

Hi Bill

In your text you say that “loans create deposits which generate reserves”.

may I humbly suggest to you that bank lending cannot create its own reserves. Bank reserves are only made up of government high powered money.

This is what I have come to understand from the Bank of England’s bulletin ‘Money Creation In The modern Economy’. As only a student of MMT I may be totally wrong of course and I do find it hard to find a definitive answer to this question.

“may I humbly suggest to you that bank lending cannot create its own reserves. ”

It creates its own reserves because the Bank of England is forced to ensure there are ample reserves in the clearing system to keep its interest rate setting powers.

It works like this. If Bank A decides to try and hoard all the reserves in the hope that they can lend them out to other banks at a rate higher than Bank Rate, then the Bank of England is forced to purchase assets from other banks to stop that attempt at cornering the market. Otherwise the interbank rate will rapidly diverge from the Bank Rate and the Bank of England loses control of its interest rate setting powers.

You can’t set a fixed quantity and a fixed interest rate. One has to be elastic in some way to allow the other.

@Neil Wilson

I think that you are completely missing my point that commercial bank reserves are ultimately always created by the central bank and not by the commercial banks themselves making loans.

They are created by the government spending and crediting bank accounts or by the central bank lending these reserves into the banking system if it is short or by returning reserves by the use of QE.

If bank lending created its own reserves then they would never run short of them as reserves would always be equal to lending. If you read the BoEs bulletin it shows clearly that bank lending never adds to reserves or that banks ever lend out these reserves.

I’m not the one missing the point.

Ruru

You are right of course

Only central banks and govts can create new money.

A new loan if from reserves with the central bank is new money creation.

But the loan must be spent on a non fin asset for eco activity to generate

Otherwise reserves just circulate in the fin system.

@Andri – interesting read, it shows that you are a well read person in philosophy of science, but not in semantics. Descriptive in Bill’s sense means prescribing something to someone to do or to act, like let us have a job guarantee program.

But you are talking about the other definition of descriptive, which is description – like describing a phenomenon… the rest you know.

@Ruru

Neil is talking about the “mechanism”, in particular, the credit creation process, but Ruru, I think you are talking about the reserve creation process.

They are 2 different processes. This should help in the dialogue.

Well I think Ruru and Neil are both right depending on how you view the situation. And technically, Ruru is always right that reserve creation can only happen through the central bank or the government. But generally, the central bank is concerned about having the banking and payment systems operating and that concern would force their hand about providing reserves when needed. So Neil is also right.

One of these days I will also be right about something.

@Ruru,

You wrote:

“Hi Bill

In your text you say that “loans create deposits which generate reserves”.

may I humbly suggest to you that bank lending cannot create its own reserves. Bank reserves are only made up of government high powered money.

This is what I have come to understand from the Bank of England’s bulletin ‘Money Creation In The modern Economy’. As only a student of MMT I may be totally wrong of course and I do find it hard to find a definitive answer to this question.”

I’m not an expert, like Bill, but this is my understanding.

. . . When a bank makes a loan, 99.9% of the time it is spent immediately or soon.

When it is spent, 99.9% of the time it is with a check.

And 97% of the time the check is deposited into a different bank.

What this means is that the Fed. Res. check clearing system is involved in the process. So, as part of this process, the money becomes “high powered money”. That is, how can anyone tell the difference between a check drawn on an account that is full of dollars created by a loan, and an account full of money from a US Gov. check to pay a Soc. Sec. payment? They can’t. So, this means that 95% of the time the 1st check deposited will convert the loan’s thin-air dollars into high-powered dollars. And, the 2nd and 3rd check of that 1st checks money as it is re-spent, converts the remaining 5%.

. . . But, I’m no expert.

Jerry Brown writes: “Well I think Ruru and Neil (Wilson) on are both right depending on how you view the situation”

Private banks create deposits; whereas central banks create reserves?

But stuff it, I want central banks to fund renewables (solar/wind + pumped hydro storage + grid upgrade) *ex nihilo*, because profit seeking private investors in ‘invisible hand’ free-market economies won’t do the job without financially extorting the rest of us.

So to simplify…..

Banks issue loans; loans create deposits. Where central banks have a reserve requirement, Increased bank deposits derived from those loans, create increased reserves at the central bank derived from those deposits. Those reserves remain a Bank asset and a central bank liability. So what`s the story here???? loans create reserves…..forget the “whys what else and wherefore”