The IMF and the World Bank are in Washington this week for their 6 monthly…

Taxation is an indispensable anti-inflation policy tool in Modern Monetary Theory

There was an unedifying and fairly undignified war on Twitter recently about whether Modern Monetary Theory (MMT) economics advocate using taxes to deal with inflation. Like all these Twitter ‘debates’, the opening proposition was a ‘gotcha’ attempt that was correct from one angle but then missed the point when it was applied to whether MMT is a valid framework or not. The responses from the MMT ‘activists’ were also overly defensive and reflected the fact that they had fallen for the framing trap presented by the antagonist. In this blog post, I want to clarify the MMT position on the use of taxes and inflation policy. What you will learn is that both positions presented in that Twitter war were largely erroneous, and, conflated concepts, either knowingly (probably not) or unknowingly, to leave a muddy mess. As the cloud became thicker, the ‘debate’ descended, as all these Twitter exchanges seem to, into unhelpful accusations of racial insult, claims of ignorance and stupidity, and worse. Not very helpful.

These Twitter exchanges are incredibly unproductive.

Twitter is not the forum for having debates and using it for that purpose usually ends in grief as it did this week.

I think the MMT activists who get roped into these trifling exchanges, thinking they are defending some verity, usually end up undermining our educational mission.

The fact the exchanges also typically end up in name calling, personal accusations and worse, just reinforces that point and opens the MMT side up to accusations of arrogance and defensiveness.

Anyway, I wish those who were interested in our work avoided these sorts of interchanges.

The Twitter exchange started with an antagonist stating that using taxes to tame inflation would be politically unpopular.

Under most circumstances I would agree but then would implore the person to tease out whether they are referring to tax revenue or changes in tax rates.

That difference matters.

The problem was that the person transitioned from this mostly correct point (depending on how we understand those terms and associations) to accusing MMT economists of not understanding the inflation process and being bereft of credibility.

Enter a prominent MMT economist (not one of the original team) who sought to deny the allegation that MMT relies on “tax increases as a primary weapon against ex post inflation”.

That statement just muddied the waters because the antagonist and the MMT activists that were armed to the teeth with keyboard angst failed to comprehend the nuance.

Various antagonists (who are seemingly on standby to wade into these asinine disputes) then produced textual evidence, they thought, proving that MMT economists (they used writing from Warren Mosler and Randy Wray as exhibits) did advocate using tax increases to tame inflation.

And if they had have consulted my work they would have found several passages where I would have argued the same proposition.

Taxes in MMT, in addition to their redistributive and allocative functions (dissauding people from smoking etc), are an essential tool in allowing governments to pursue a spending program without pushing nominal spending growth ahead of the real productive capacity of the economy.

Which means they serve a anti-inflation function.

The problem was that the antagonists didn’t really appreciate what the textual segments they produced were meaning.

They took the words literally and applied them to their purpose.

The problem is that they didn’t differentiate between tax revenue as a vehicle for setting the non-inflationary size of government and the manipulation of tax rates to modify total spending.

Both functions of the tax system are part of the anti-inflationary ‘weapons’ that government has at its disposal.

But unless you distinguish those functions, we end up in the mess that I saw unfold on Twitter this week, where both sides of the debate were really arguing about a meaningless set of propositions.

One of the other problems that lead to these Twitter misadventures is that there is a tendency for MMT activists to conflate their political agendas with the MMT framework of analysis.

They find that the framework may, at times, deliver conclusions that are incompatible with their political motives, and instead of recognising that openly, they seek to re-frame what they claim is MMT.

That is an additional source of opaqueness and leads to accusations that MMT economists just make it up on the run.

We don’t.

And among the original team there is no disagreement on what MMT is and isn’t.

But if people start getting loose with concepts to suit their own ends, then it can easily be said that MMT is not a consistent body of knowledge.

So let me explain how MMT constructs the issue of taxes as an anti-inflation weapon and leads to the conclusion that taxes are a primary weapon against inflation within the MMT body of knowledge.

Tax revenue sets the non-inflationary size of government

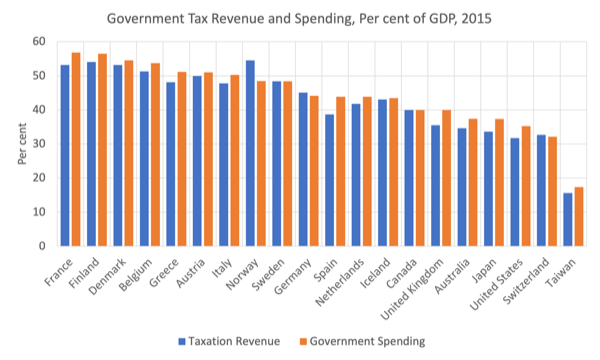

Consider the following graph, which shows government tax revenue and spending for a range of nations as at 2015.

I chose 2015 because it was after the GFC and before the pandemic – so representative of more normal behaviour.

While most nations run small fiscal deficits, the point of the graph is that large spending governments require large volumes of tax revenue.

The revenue is not to fund the spending but to create the real resource space that can absorb government spending in a non-inflationary manner.

Let’s dig into that a bit deeper.

Initially, with a worth fiat currency (digital or physical tokens), there must be a motive created in the non-government sector to ensure they use the government’s currency.

The imposition of the tax liability does the trick because it forces the non-government sector to supply productive resources to the government sector, which in turn allows the government to fulfill its spending program.

That is step one.

Another way of seeing that is to understand that given that the non-government sector requires the government’s fiat currency to pay its taxation liabilities, the imposition of a tax liability (without a concomitant injection of spending) by design creates unemployment (people seeking paid work) in the non-government sector.

The tax liability thus frees up real resources that would otherwise have been utilised through non-government spending.

The unemployed or idle non-government resources can then be brought back into productive use via government spending which amounts to a transfer of real goods and services from the non-government to the government sector.

In turn, this transfer facilitates the government’s socio-economic program.

While real resources are transferred from the non-government sector in the form of goods and services that are purchased by government, the motivation to supply these resources is sourced back to the need to acquire fiat currency to extinguish the tax liabilities.

Further, while real resources are transferred, the taxation provides no additional financial capacity to the government of issue.

Conceptualising the relationship between the government and non-government sectors in this way makes it clear that it is government spending that provides the paid work which eliminates the unemployment created by the taxes.

And the scale of this relationship – or, in other words, the size of government – then dictates the scale of the (initial) unemployment created by the tax liability.

Relatively large governments require large tax revenues, while smaller footprint governments require smaller tax takes.

But note that scaling relationship is not about ‘funding’.

It is about creating the non-inflationary real resource space to absorb the scale of government spending desired.

The policy design must ensure that the tax revenue is sufficient – and depriving the non-government sector of resource usage – to accommodate the scale of spending desired.

While the orthodox conception is that taxation provides revenue to the government which it requires in order to spend, the MMT conception is that the tax revenue is an indispensable policy requirement in order to ensure the government can operate at its desired scale, without pushing the economy into an inflationary episode.

This insight then has implications for shifts in government policy (scale).

For example, consider a Green Transition, which will almost certainly require an increased scale of government activity in the economy – resource demand – at least in the first stages of the decarbonisation.

It is inconceivable that the increased demand for public resource use will be achievable without increased tax revenue given that an open competition for resources would set off a major inflationary episode (driven by excess nominal demand).

Again, this is about setting scale and that is a crucial role that taxes play.

So when critics produce textual segments from MMT economists that say that taxes are an important anti-inflationary tool, they should understand these starting points as a context, rather than concluding that tax rate changes are always going to be the preferred tool for dealing with cyclical fluctuations in nominal spending.

We turn to this second ‘tax perspective’ now.

Tax rate changes can be used to manipulate spending

The other perspective on taxation is that it is a policy tool that can be varied to deal with cyclical shifts in spending.

It is here that the politics of tax policy are most relevant.

Generally, it is true that a government would become very unpopular if it varied its tax rate structures regularly to deal with cyclical fluctuations.

There are times, when the adjusting tax rates in the short-term or on a once-off basis (say a special hypothecated levy) is political easy to accomplish.

For example, in 1997, the then British Labour government introduced a new ‘windfall’ tax on “the excess profits of the privatised utilities” as a once-off measure to redress the ridiculously low sale price that the Tory government had allowed (Source).

More recently, the current Tory government has proposed a windfall tax on energy companies, who through no good work of their own are experiencing booming profits as a result of the Ukraine war.

The purpose of the tax is to put pressure on the companies to reduce energy prices by reducing their excess profits and redistributing the funds to those in need as a result of the energy price gouging from the companies.

Other governments are being encouraged to use these ‘windfall’ tax initiatives to reduce inflationary pressures arising from profit gouging.

So it is not always true that governments are politically unable to vary tax liabilities on a cyclical basis rather than as a structural means to change the scale of government (as above).

But I accept the point that using tax rate manipulation to deal with temporary demand excesses, for example, is not politically easy, even if it would be a very effective way to alter spending levels.

Further, as is clear in all the MMT literature the government has a range of policy tools that can be implemented in the short-run to modify inflationary pressures and do not attract the same political damage as tax variations might.

And, which tool is suitable depends on the source of the price pressure.

It is a complex process disentangling the primary reason for the price impulses from the derivative impacts.

For example, at present, central bankers are claiming that the inflationary pressures are generalising and that means interest rates have to rise.

But an initial supply shock (example, oil shock) increases unit costs through the vertically-integrates supply chain.

All energy using operations which have price setting power to defend real profit margins then push the cost increase onto the next level in the chain, and ultimately, onto final consumers.

The inflation is then general.

But that state still might not have a further propagating mechanism – like workers seeking to engage in real wage resistance and push up (and gain) nominal wage increases.

In which case, the inflation will dissipate quickly once the initial cause – the oil price rise – is reversed.

The point is that in some cases, tax rate changes might be required – for example, the reduction of excise taxes on petrol might be entertained in the short-run.

In other cases, other policies would be more effective.

I have previously advocated, for example, making public transport free to alleviate the oil problem.

Governments could make child care free (in Australia it is mostly a privatised, fee-for-service sector).

They could scrap indexation agreements with medical funds and cap energy prices.

And more.

So in a cyclical event, there are many policy tools that can be introduced to reduce inflationary pressures – tax rate changes being one of an assortment.

Conclusion

I hope that clarifies the matter.

It is wrong to state that MMT does not advocate the use of taxation as a primary policy tool against inflation.

But agreeing with that proposition does not then lead to the conclusion that tax rate changes will always be the preferred cyclical variable to offset price pressures.

That is enough for today!

(c) Copyright 2022 William Mitchell. All Rights Reserved.

“The policy design must ensure that the tax revenue is sufficient – and depriving the non-government sector of resource usage – to accommodate the scale of spending desired.”

That’s unfortunately where the current crop of so-called MMT activists struggle.

They struggle to come to terms with the simple reality that the amount of taxation that can be imposed on a population has a political limit, and that won’t be sufficient to fund the excessive spending programmes the activists want to undertake.

The reality of having to cut coat to cloth doesn’t appeal, and so they end up off down the usual avenue where economists go to die – trying to find the perfect Control Theory to manipulate the quantity of private credit in order to avoid having to face up to the voting public, and yes the taxpaying, public.

In this they become no different to the belief put forward by the likes of Simon Wren Lewis

MMT is falling back into the captive beliefs put forward by Post Keynesians due to its perceived political alignment in the USA and the restrictions that puts on discussions.

Hence the “Modern Donkey Theory” jibes.

A move back to talking about buffer stocks and allowing the horizontal circuit to float within a new control regime is way overdue.

What if western countries have a dual tax-system?

That is, one set of taxpayers paying taxes and another set of “taxpayers” beeing paid “taxes”.

We all been watching how our governments built corporate wellfare.

There are bilionaires out here getting richer and richer, because of “taxes” they keep “colecting” from governments (as an example, the US government just paid 51 bilion dollars to the US guns industry on the Ukrainian account).

Dual tax-systems are a major source of market distortion.

What business can survive, competing with some (private) behemoth, fed on public money?

So, the small business can’t grow and probably will die or bought by the behemoth.

Crisis after crisis, and the behemoth turns into monopoly.

And then, he can price the goods/services he sells as he finds fit.

That’s inflation.

Hi Bill,

From this perspective of taxes as a tool to reduce demand (thus creating unemployment to facilitate the transfer of these resources towards the government), is it correct to say that not all revenue / tax dollars are equal?

Let’s say we want to “pay for” an expensive resource-intensive initiative, such as a Green Transition, though higher taxation. One approach is to raise sales taxes, which would be both unpopular and bad from an equality perspective as it would hit the poor hardest. A more popular alternative is to tax the rich. Let’s take the extreme upper end of that – a billionaire’s tax.

Even if such a wealth tax raises sufficient revenue to pay for the dollar cost of such a program, it will be much less effective than an equal-revenue sales tax at relieving resource constraints, as billionaires have a very low propensity to spend. Such a tax policy could conceivably make things worse, as it may encourage a “use it or lose it” mentality.

Does this make sense? Have you written about this problem anywhere (particular from an equality perspective)?

Thanks,

Tim

Tax “revenue” as a term seems problematic as it implies taxes fund spending. Tax “imposition” or tax “charges” maybe?

Dear Barri Mundee

Revenue is a French-sourced word for returning back.

It returns the government spending that created the capacity for the non- government sector to pay the taxes.

Best wishes

Bill

“One approach is to raise sales taxes, which would be both unpopular and bad from an equality perspective as it would hit the poor hardest. A more popular alternative is to tax the rich. Let’s take the extreme upper end of that – a billionaire’s tax.”

A better approach would be to tax employment – since reducing private employment is what we are trying to do by imposing taxes. That way you don’t favour hoarding income over spending it. If effort is expended and income earned, it is taxed regardless of what you do with it afterwards.

Incidentally this is why the rich favour consumption taxes over income taxes. It means they can hoard more money.

You can only really tax spending flows to effect resource transfer. Savings are essentially voluntary taxation and are already largely inert in terms of their command of resources.

If you ‘tax the rich’, then you’ll just have to tax again somewhere else to cut the spending flows by the necessary amounts.

“Pay fors” don’t necessarily stop inflation until those ‘pay fors’ are in real terms.

Is it helpful at all to be always repeating that taxation “extinguishes” money rather than “collects” it? I guess the original French word (as Bill points out) “returning back” implies this concept, but I fear that the general public’s experience of money as an object rather than a ledger system results in images in their mind of tax revenue as a pile from which subsequent government spending comes – as long as this image holds sway I see difficulties in getting further penetration of the correct description that all sovereign government spending is “new” money emitted into circulation while all taxes, fees and fines received by that government is destroyed at the moment of return.

Now you know how Marx felt when the ‘Marxists’ started all their carry-on. Once a theory is put into the public sphere any old Tom, Dick and Harry becomes a purveyor and expert.

something worth adding is this idea of taxes “freeing up” resources applies more to a fully employed economy than as a general rule. Increasing the level of taxation in an economy where there are already idle resources seems more like “encouraging deflation” than “reducing inflation”.

Seems also that paying down private debt is similar to taxation in its accounting effects….both result in money that was created (either by govt spending or by a loan) being destroyed….makes me wonder why there isn’t similar terms for this in standard macroeconomic accounting…we have (G-T) as net amount “govt spending/taxation”, but not something like (B-R) for the net amount “borrowed(B) / repayed(R)”

Paying off private debt is done voluntarily, randomly and often just transferring credit to other (private) hands, it doesn’t ‘destroy’ the money necessarily if at all. Taxation is different, it is a large-scale tool of government policy

@Neil Wilson: “Savings are essentially voluntary taxation and are already largely inert in terms of their command of resources.”

Not necessarily because they haven’t been frozen, in e.g. the way a bond sale is designed to do that. Savings can easily be be put into action competing for resources on sale.

If the expenditure is made to compensate for diminished demand, let’s say a compensatory income for those not able to get a full wage through imposed unemployment during a lockdown, I suppose the fiscal spending in that case is done to counter deflation, therefore taxation to offset it is not required? And “financing” through “debt” is better?

I find a lot of these explanations of the use of taxes very confusing. What i do is try and make it simple. SITO is an acronym meaning Spend in, Tax out. I can understand the ability of government to spend into existence new money to pay a bill. I can also understand the ability of government to tax in order to destroy existing money. As a consequence I can conceptualize the phrase ‘fiscal space.’ Asking the average citizen to go any further is a waste of time. Getting just this simplified, brief explanation across is tough enough.

“Not necessarily because they haven’t been frozen, in e.g. the way a bond sale is designed to do that. ”

Yes necessarily. Government Bond sales don’t ‘freeze’ anything either. Because they are ‘negotiable’ and there is a buyer of last resort (unlike in the FX market where there isn’t).

There is no magic in bonds. It’s a neoliberal myth. “Sterilisation” is up there with the “money multiplier” in fantasy land.

@Neil Wilson: “Yes necessarily. Government Bond sales don’t ‘freeze’ anything either. Because they are ‘negotiable’ and there is a buyer of last resort (unlike in the FX market where there isn’t). ”

They are a (indeed neoliberal now) method of letting rich people freeze some money rather than having it taxed away. That is what a bond does, it’s an agreement to not spend an amount in exchange for an interest payment. So they (or whomever ends up with the bond) can redeem it later.

Randy Wray was very clear about this. Listen to him saying practically this very thing on his first or second interview of the MMT podcast.

The national government’s tax system creates the vast majority of the non-inflationary fiscal space available to the national government. Tax payments are a spending drain out of the domestic economy – they reduce the amount of currency that households and firms can spend on real resources (goods, services, labour).

Is it true to say that there are two other spending drains out of the domestic economy that add to the fiscal space available to the national government? These would be non-government sector saving, and non-government sector spending on imported products.

When households and firms save some of their income instead of spending it on goods, services, and labour they are freeing up some goods, services, and labour that the government could then choose to purchase in a non-inflationary manner.

When households and firms spend some of their income on imported resources instead of domestic resources they are freeing up some domestic resources that the national government could then choose to mobilize in a non-inflationary manner.

The three spending drains differ in size: national tax receipts are a much bigger spending drain than non-government savings and non-government spending on imports. But non-government savings and non-government spending on imports can still be valuable contributions to the national government’s non-inflationary spending space.

I think that MMT economists have made it abundantly clear that the national tax system is ultimately what makes it possible for the national government to command real resources in a non-inflationary manner. Without the national tax system there would be no widespread demand for the government’s currency, and without that demand it isn’t possible to find large numbers of households and firms willing to sell goods, services, and labour in exchange for payments in the government’s currency.

I think that MMT economists highlight a variety of price stabilization measures.

1/ Enacting a nationally funded, community-administered Job Guarantee that acts as a buffer stock price stabilization scheme for labour – as a public option for jobs – that maintains non-inflationary full employment at all times.

2/ Providing a wide range of public services and public infrastructure with no user fees – this can be done for all forms of health care, all forms of education (including early childhood education), mass transit, banking services, information and communications technology (free Fibre-To-The-Premises broadband Internet connections for every household and business; free national phone calls and text messages; free quotas of mobile data and broadband Internet data), energy (free quotas of renewably generated electricity for every household and business), community arts and culture, community recreation and entertainment and sport.

3/ Having large amounts of publicly funded, high quality housing for first home buyers to purchase at regulated prices, along with large amounts of high quality public rental housing.

4/ Lifting all income support payments, including the age pension, the disability support pension, carer’s payments, student payments, job seeker payments, and illness and injury payments so that they are above the 60 percent of median income definition of the poverty line. Making the wasteful private superannuation sector obsolete by lifting the age pension to an adequate level and by lowering the pension age to 60 so that people can retire earlier if they want.

5/ Having the national government invest in upgrading the resilience and self-sufficiency of the nation with regard to essential goods – especially food, fuel, energy, construction materials, medical supplies, pharmaceuticals, medical equipment, transport systems, information and communications systems.

6/ Making aggressive use of anti-trust law to make private markets as competitive as possible.

7/ Designing intellectual property law to prioritize the development of knowledge and technology and the dissemination of knowledge and technology across and between societies. Prevent intellectual property from being used to slow down or limit the development and spread of knowledge and technology. Make all nationally funded research publications and technical innovation public domain so that everybody can use it for free.

(Wray 2015; Lane and Wray 2020; Mitchell, Wray, and Watts 2019). ‘Macroeconomics’ states:

“Ideally, it is best if tax revenue moves countercyclically, increasing in an expansion and falling in a recession. That helps to make the government’s net contribution to the economy countercyclical, which helps to stabilise aggregate demand. In this case the fiscal outcome operates as an automatic stabiliser.”

Once again the history books have the answers on how to do that.

Planning public works – history has a lot to say if we listen properly

https://billmitchell.org/blog/?p=37930

“The Japanese government has a well-designed infrastructure plan in place that allows it to expand and contract government spending to extend the highway and related infrastructure (bridges, waterways etc) to suit cyclical conditions.”

“The decision by Norwegian authorities to fast-track the construction of Oslo Airport at Gardermoen was a highly effective fiscal intervention. The intervention was effective and finite. It also carried scale such that components could be expanded or restricted at fairly short notice to meet with the changing cyclical conditions.”

Planning- Having organised plans ready to go that fits in with the cyclical conditions. This type of spending can be highly responsive with minimal lags.

” The National Resources Planning Board released another major report in January 1941 which encapsulated the way that governments were working on the implications of the theoretical ideas from Keynes and others.

The 432-page Report – Development of resources and stabilization of employment in the United States – has many beautiful pieces of analysis and reasoning, which buttress the core MMT propositions with respect to the primacy of fiscal policy.

A reading of that Report will leave you in no doubt as to how a national currency-issuing government can implement effective fiscal policy to meet both longer-term needs of its people but also counter-cyclical responses in a time when recession threated as non-government spending was in retreat.

Exactly an answer to the concerns that people have that fiscal policy cannot be implemented in a timely manner. ”

Chapter C. Public Works for Employment Stabilisation’ commenting on Page 14, which outlines how government spending can be planned over time to meet longer-term objectives and ensure cyclical stabilisation functions are served.

History once again gives the answers and history also shows these battles are very rarely won in a class room. Or waiting on a paradigm shift one death at a time.

Thatcher never waited – Real power is the key and the backing of the establishment. If you don’t have those then it is normally fought in the streets. It just the way Empires roll I’m afraid, you have to get permission or fight to try and get a little bit of real power.

They know that of course. Why they invented fiscal rules and created treaties and charters so that the rule based order remains and nothing changes. The rules of free trade have been written they way they have been. Free movement of capital, free movement of extortion. Colonial economics from which to steal real resources from the weak from which to extract rent.

Do you actually believe the Empire is just going to allow you to introduce what you want ?

If only we could have a little chat with the Empire they will adopt our ideas ?

Once again history explains in great detail what it takes. Cracked on the head with big clubs, with a long walk to sea to make salt and spin your own cloth. That’s just the “hors d’oeuvres”.

“Randy Wray was very clear about this. Listen to him saying practically this very thing on his first or second interview of the MMT podcast.”

I doubt Randy was saying what you have interpreted it as. A bond doesn’t do anything in terms of preventing spending – because it is guaranteed to be liquid.

There is no difference in spending capacity if you hold £100 in a savings account, or £100 in Gilts. In fact if the savings account is a 90 day notice account there is less capacity to spend with the savings account.

Bonds do nothing to prevent spending. They just represent free money to rich people.

Nicholas Haines, I applaud both your contributions above, but especially the first in the present context termed ‘inflation’ where the present *price increases* agitating the air waves as ‘inflation’ are near entirely concerning big price hikes on inelastic demand essential goods like oil & gas.

Effectively, what we are seeing is a significant increase in the net savings desires of the foreign non-Gov sector, leading inevitably to a ‘spending drain’ in the domestic non-Gov sector. Which also means recessionary bias absent any compensatory actions. (But one which JG would be very useful in mitigating of course.)

This dovetails nicely to a point that Bill makes which is absent from near every discourse on ‘inflation’, & totally absent from the MSM propaganda & ignorance propagating machine that controls political outcomes… this:

“… which tool is suitable depends on the source of the price pressure.

It is a complex process disentangling the primary reason for the price impulses from the derivative impacts.

For example, at present, central bankers are claiming that the inflationary pressures are generalising and that means interest rates have to rise…. ”

In public discourse, the term inflation is used routinely used for both ‘price impulses’ (aka price increases of significant inelastic effect – or they’d just be a ‘relative prices’ story) & the ‘derivative impacts’, ‘generalising’ (aka wage-price spiral in continuous phenomenon that is actually the agreed defn. of term inflation).

Then disingenuously (quelle surprise!), the mainstream macro frauds & propaganda machine immediately ignore the ‘price impulses’ part & jump to hyperventilating about the spiral part, low & behold with all their usual guff about needing to reduce general consumer spending & wages etc.

But this is hardly surprising, is it, when the same term – inflation’ – is used for both phenomena, when as Bill points out, the first, price increases part, may not inevitably lead to the second, generalising spiral?

Indeed, one might consider the ‘price impulses’ to be a micro economic phenomena (& Warren Mosler liked my own minor tweet on this point), where the ‘generalising’ spiral would clearly be a macro phenomena. Another egregious error in mainstream economics in conflating the two.

How any supposed ‘academic’ field can still be using a term, inflation, utterly ambiguously, leading to gross confusion & policy failures* for, well, ever, totally escapes me. (And it’s not the only example – ambiguity of terms is rife in economics. More like astrology than what Wren-Lewis types laughably consider ‘science’.)

(*policy failures for the ~90% labour class that is, sterling outcomes for the capital owner ~10%, hardly an accident)

So, imo, what economics discourse needs to get back to is dealing with the issue at hand & doing so without using ambiguous terminology.

Right now, developed economies are experiencing a spending drain from increased net savings desires of the foreign sector specifically (ie with their lower propensity to spend), together with a bit of domestic/corporate price gouging, to similar effect.

Well, my starting position, from MMT, is ‘Gov must accommodate the net savings desires of the non-Gov sector, in order to maintain potential output’. But needs to do this in a way that doesn’t ‘generalise’ the (micro) ‘impulses’ into (macro) wage-price spiral.

My suggestion is that eg. for oil imports, Gov steps in, upstream, to subsidise/control pricing of imports. Making it clear to the price hiking foreign exporters that it won’t tolerate the prices indefinitely, & will take action to substitute such essential goods, on permanent basis, as necessary.

But what do MMT academics & professional prescribe for the present situation – if I’ve framed the problem it correctly? IMO, we really do need to move the theorising on, useful as it is, & talk about the specifics facing our economies.

[quote] vote for pedro

Friday, June 24, 2022 at 0:39

…snip…

Seems also that paying down private debt is similar to taxation in its accounting effects….both result in money that was created (either by govt spending or by a loan) being destroyed….makes me wonder why there isn’t similar terms for this in standard macroeconomic accounting…we have (G-T) as net amount “govt spending/taxation”, but not something like (B-R) for the net amount “borrowed(B) / repayed(R)”[/quote]

This is a very good point.

I had to thin about it to see how the money is destroyed.

AFAIK, it is applied on the banks book to off set the decline in the value of the asset of the bank that is to repayment contract.

IMO, the main reason that this isn’t in MainStream econ. text books is that part of the project of neo-liberalism is/was to hide certain facts from the public. This works best if it is hidden from econ. students too. I’ve been told by an MMTer that banks were totally factored out of the theory by assuming that they must lend the savings of their depositors. MS econ-ists wanted to hide this fact, so they said they could ignore banking totally.

. . . So they assert (falsely), that private debt is great, but public debt to terrible. Never mind that private debt is the cause of many recessions. For example the GC/2008. And, pubic debt causes no recessions, but trying to have a surplus to reduce the public debt has caused many recessions. For example the 2000 dot com bubble recession, and IIRC the Great Depression.

.

Hi Mike, I value your lucid writing style. You use language in ways that illuminate rather than obscure the concepts being discussed.

I like what you said about the differences between inflation, which is defined as a continuous or ongoing increase in the general price level of the economy, and one-off price adjustments. I think the tendency of journalists, politicians, public servants, and public policy researchers is to use the term inflation indiscriminately, including in situations where it would be more accurate to speak of one-off price adjustments.

I think there is a general lack of literacy and rigour among politicians, journalists, and professional economists about the causes of inflationary episodes and of instances of major one-off price adjustments. There is a near total failure to acknowledge that in historical practice the phenomena of inflation episodes and one-off price adjustments are overwhelmingly supply-side phenomena, involving major disruption or loss of productive capacity and distribution mechanisms. Pandemics, wars, revolutions, political crises – these are nearly always involved in the most severe cases. In the past forty years there has been the additional factor of pro-corporate neoliberal economic policies that have increased the degree of monopoly and oligopoly power in the economy, resulting in corporations having too much price-setting power. Neoliberal economic policies have also reduced national resilience and self-sufficiency in the production of essential goods, increased societies’ vulnerability to supply chain disruptions in other nations, and reduced the provision of free or cheap services.

The impression I’ve formed from reading about economic history is that isn’t even true to say that some inflationary crises are predominantly demand-driven and others are predominantly supply-side. Is there even a single major inflationary crisis from history where it would be fair to say that it was caused primarily by too much government and / or consumer spending and there weren’t any major issues with supply, with productive capacity, with price-setting power? The political bias of the past four decades has been towards wage stagnation and fiscal austerity. It suits the purveyors of a neoliberal agenda to portray problematic inflation episodes and one-off price adjustments as stemming potentially from workers getting paid too much and / or from the national government doing too much spending on public goods, even if it never actually happens in that manner.

@ Nicholas Haines, you wrote:

“The impression I’ve formed from reading about economic history is that isn’t even true to say that some inflationary crises are predominantly demand-driven and others are predominantly supply-side. Is there even a single major inflationary crisis from history where it would be fair to say that it was caused primarily by too much government and / or consumer spending and there weren’t any major issues with supply, with productive capacity, with price-setting power? The political bias of the past four decades has been towards wage stagnation and fiscal austerity. It suits the purveyors of a neoliberal agenda to portray problematic inflation episodes and one-off price adjustments as stemming potentially from workers getting paid too much and / or from the national government doing too much spending on public goods, even if it never actually happens in that manner.”

Please let me reply about hyperinflation, which is generally the boogeyman.

I saw a report by the Cato Inst. (a Koch brothers thinktank) about hyperinflation in *all* of history. I can’t see it on google now. However, it found 56 or 57 cases, all since 1900. It asserted that in every case it was caused by shortages.

I did find this more recent study by the Cato Inst.

“HYPERINFLATION: HOW THE WRONG LESSONS WERE LEARNED FROM WEIMAR AND ZIMBABWE (A HISTORY OF PUBLIC MONEY CREATION PART 2 OF 8)”

There it says it again. All cases of hyperinflation were caused by shortages of something. They mention Weimar and Zimbabwe.

People, I reply to other people, why don’t you reply to me?

.

This statement, of yours below, sure sounds like tax and spend, that US Republicans have always labeled Democrats but especially Democratic Socialists

“The imposition of the tax liability does the trick because it forces the non-government sector to supply productive resources to the government sector, which in turn allows the government to fulfill its spending program.

That is step one.

Another way of seeing that is to understand that given that the non-government sector requires the government’s fiat currency to pay its taxation liabilities, the imposition of a tax liability (without a concomitant injection of spending) by design creates unemployment (people seeking paid work) in the non-government sector.

The tax liability thus frees up real resources that would otherwise have been utilised through non-government spending.

I have your Macroeconomics textbook and understand that you first spend into the economy before you tax, but some will not nite your sequence.

Does your above discussion look like crowding out? I have your Macroeconomics textbook and understand that you first spend into the economy before you tax, but some will not note your sequence.

I don’t understand how taxing windfall profits from energy companies would cause them to lower prices.

I’d have thought it would have the opposite effect to maintain profits.