It's Wednesday, and as usual I scout around various issues that I have been thinking…

RBA tom foolery continues while spending continues unabated

It’s Wednesday where I examine in short a few items that came to my attention in the last week and then retreat into the music segment. Yesterday, the Reserve Bank of Australia raised interest rates for the sixth time since May 2022. This time the increase was 0.25 per cent and the current cash rate target is 2.6 per cent. The below-expected increment has been hailed as the first central bank to ‘turn’. It tells me the RBA is now scared it has gone too far in its ridiculous show of power. It is also obvious that spending is not really responding yet to the RBA move which means that they have no real idea of what the impact of their shift in rates has been. That is the problem with relying on monetary policy as a counter-stabilising tool – it works (if at all) with long lags and by the time you see any impact it might be too late.

What does the RBA think it is doing?

In the – Statement by Philip Lowe, Governor: Monetary Policy Decision (October 4, 2022) – the RBA claims that it will continue to increase interest rates in order to stifle inflationary pressures.

Unlike previous statements, the RBA was short on explaining why there are inflationary pressures at present in Australia.

All we got this month was:

Global factors explain much of this high inflation, but strong domestic demand relative to the ability of the economy to meet that demand is also playing a role.

In previous statements, they had listed “the war in Ukraine”, high energy prices as a result of the uncompetitive OPEC cartel exercising monopoly power, and “floods” in Australia as the causes in addition to Covid-sourced supply constraints.

None of those factors are sensitive to interest rate changes.

So I guess they wanted to avoid that obvious glitch in their logic that their policy instrument is not exactly capable of doing what they claim is their objective.

So all we get this time is ‘global factors’ (not sensitive to domestic interest rate changes) and domestic demand.

Which means they are trying to reduce domestic spending.

The fact they don’t attempt to break down the split between the global factors and domestic demand is problematic.

But it is clear they want to bring spending growth down to align with the temporary disruptions in supply.

That isn’t a very sensible strategy because when those temporary disruptions ease what we will be left with is excess productive capacity, unsold inventories, and elevated unemployment.

Then what?

The problem with the RBA’s decisions is that the evidence suggests the interest rate rises are not very effective anyway in attenuating demand.

Which means the RBA will just pushing until rates are so high that borrowers become insolvent.

We have seen them do that in the late 1980s and a major recession eventually was the result aided by fiscal contractions.

The other problem is that the RBA thinks that they will not create a recession because:

Many households have also built up large financial buffers and the saving rate still remains higher than it was before the pandemic.

I examined this point in more detail in this blog post – The RBA has lost the plot – monetary policy is now incomprehensible in Australia (July 6, 2022).

Many is the ‘top-end-of-town’ rather than the low income earners who are carrying record levels of debt.

We want the household saving ratio to remain high because the pre-pandemic levels were too low, given the debt exposure.

But there is also a logic problem for the RBA.

It is clear the RBA thinks that the buildup of saving by households provides a buffer to allow them to keep spending.

Yet, on the other hand, they are claiming that they are raising interest rates to address strong domestic demand (spending).

They obviously know the interest rate rises will do nothing to attenuate the global factors mentioned above.

So it is all about reducing domestic spending.

Thus, if the saving buffers maintain spending capacity, all the RBA is really doing is destroying the financial wealth of households by forcing them to liquidate past saving buffers.

If households maintain nominal spending growth (which isn’t particularly strong anyway) then the interest rate rises will only succeed in destroying household wealth (running down savings) and the so-called domestic inflationary pressures remain.

This is the twisted logic of the RBA.

In the past week, we have had a raft of data which shows that spending and lending is not really falling yet.

First, what about retail sales, which is a monthly measure of demand in the economy.

The most recent data was published last week (September 28. 2022) by the Australian Bureau of Statistics – Retail Trade, Australia (August 2022).

There are two ways of looking at this:

1. The ABS report that “Australian retail turnover rose 0.6 per cent in August 2022 … The August increase was the eighth consecutive rise and follows a 1.3 per cent rise in July 2022, and a 0.2 per cent rise in June 2022.”

The rise in expenditure was particularly noticed in “cafes, restaurants and takeaway food services up 1.3 per cent and food retailing up 1.1 per cent.”

So the interest rate rises are doing very little so far, it seems to quell sales and demand.

2. Is the expenditure growth high and accelerating?

The graph shows monthly growth in turnover and as you can see has been declining since the beginning of the year – before the RBA started its current hiking phase.

There were some sectoral differences (Department stores and Cafes, restaurants and takeaway services were both above the aggregate) but total spending on retail goods and services has been in decline anyway and is growing modestly.

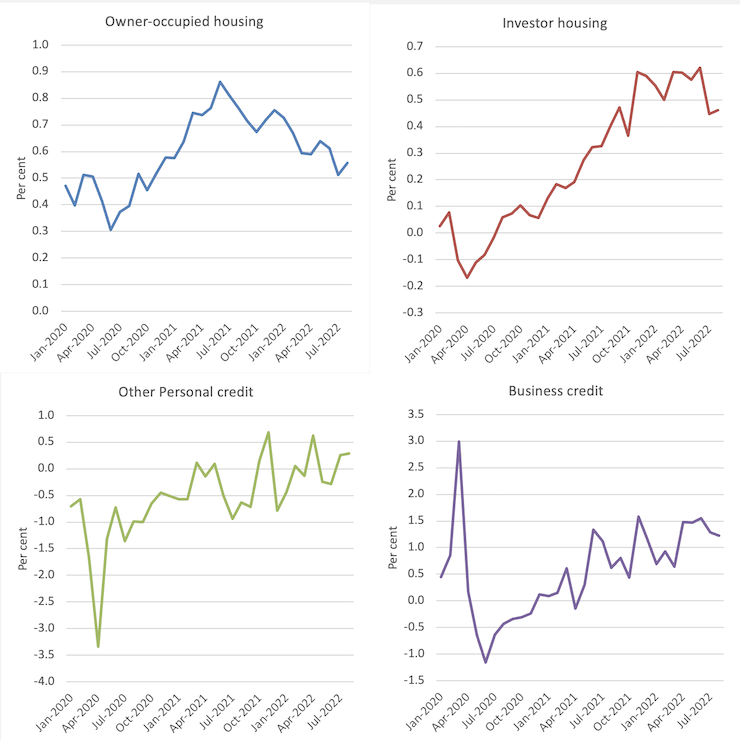

The following graph shows the monthly growth in the major credit aggregates since January 2020 up to August 2022.

These are the so-called interest-rate sensitive aggregates that the RBA might influence through interest rate rises.

Apart from the on-going speculative binge on investment properties, which has turned down since the rate hikes began in May 2022, the other aggregates are not accelerating and growth in owner-occupied housing credit has been in decline since May 2021, long before the RBA moved.

The investment housing binge is due to distortions in the tax system that rewards high income earners with massive tax breaks for accumulating multiple properties.

It should be addressed through tax reform.

It is also true that while the rate of change might be levelling off in most categories, the absolute level might be excessive. There is some evidence that the current growth in overall credit is higher than the pre-pandemic.

Dampening housing credit will do little to address the overall inflation rate which is being driven by energy and food prices mostly.

And if one nets out housing then the credit growth picture is more subdued.

If the RBA further dampens non-housing credit growth that will impact on the already weakening retail sales and push Australia towards recession.

Monthly growth in credit aggregates

I am currently working in Kyoto, Japan for some months.

The Bank of Japan has not shifted its still negative policy interest rate.

The Ministry of Finance is providing fiscal assistance to households to ease the cost of living pressures.

The inflation rate is just 3 per cent.

Go figure.

The rest of the world has gone ‘neoliberal’ mad again and its central bankers are out of control.

Trickle down

With all the talk in Britain at present about the new PM/Chancellor’s revival of the discredited ‘trickle down’ theories – you know the line that ‘cutting taxes for the rich and making them richer ends up making the poor richer’ – and as part of my research for my new book, I was interested to trace the origin of the idea.

The idea of ‘trickle down’ seems to have been first articulated in 1896 by the Democratic presidential hopeful William Jennings Bryan who criticised Republicans at the time for believing that government should make the wealthy even more prosperous so that some of the largesse would ‘leak through on those below’.

Go here – Bryan’s ‘Cross of Gold’ Speech: Mesmerizing the Masses – to read the full speech which was delivered on July 9, 1896.

Later, on November 26, 1932, The St. Louis Star and Times published its regular syndicated column from American columnist Will Rogers – Will Rogers Explains That Money, Unlike Water, Always Trickles Up, which included a commentary about the 1932 US Presidential Election, which Franklin D. Roosevelt won in a landslide over Herbert Hoover.

Will Rogers jested that the:

… election was lost four and five and six years ago, not this year. They didn’t start thinking of the old common fellow till just as they started out on the election tour. The money was all appropriated for the top in the hopes that it would trickle down to the needy. Mr. Hoover was an engineer. He knew that water trickled down … But he didn’t know that money trickled up. Give it to the people at the bottom and the people at the top will have it before night anyhow. But it will at least have passed through the poor fellow’s hands.

So well before the likes of Dave Stockman (Reagan’s ‘budget’ director) started implementing the idea which has become a religion for whacky conservatives, the concept was held in contempt for what it was – a ploy to enrich the already rich at the expense of everyone else.

Chess scandals

The only game I really play is chess.

There is an excellent and powerful chess machine available for iPhones (Stockfish) and while it runs down the phone’s batteries quickly it is a great learning and playing tool.

So I use it regularly and over the years it has allowed me to significantly improve my knowledge of the great strategies deployed historically by the best players and the way that these strategies have shifted over time.

Chess engines, though, in the hands of scoundrels are a curse.

I read the just read the – Hans Niemann Report – published by Chess.com yesterday, which documents (and speculates) on how Mr Niemann has been “cheating in chess” competitions.

While the Report estimated that cheating occurs in “fewer than 0.14% of players” on the Chess.com platform, it finds that “Hans likely cheated online much more than his public statements suggest.”

If you follow chess news and study the international competitions (like me) then you will be aware that the current World Champion, Magnus Carlsen essentially accused Niemann of cheating in a major tournament, which led to Carlsen withdrawing from the competition.

Niemann has made a very fast (too fast?) rise in the world rankings given his age and has confessed to cheating in the past.

Chess.com compared the moves that Niemann has made in previous competitions with the moves that a supercomputer would make and concluded that “Hans has likely cheated in more than 100 online chess games, including several prize money events. He was already 17 when he likely cheated in some of these matches and games. He was also streaming in 25 of these games.”

It turns out that – Cheating in chess – is common, especially in the digital age with chess engines and on-line games.

Very sad really that such a fine game is open to such aspiration.

Music – Chet Baker in Tokyo

Given that I am currently working in Japan, I thought this was a good album to drag out.

This song Broken Wing is from the June 1987 album – Chet Baker in Tokyo< (King Records) – by the great trumpet player – Chet Baker.

It is a fine album for sure.

The song was written by American jazz pianist – Richie Beirach.

This song was taken from the concert, which was just 11 months before he died at the age of 58, lying on the street in Amsterdam after falling from his hotel room. He was a lifetime heroin addict.

Sombre and flowing. He was a physical wreck by the time this concert was held but could still play exquisitely.

The musicians in the quartet other than Chet Baker were:

Harold Danko – piano

Hein Van Der Geyn – bass

John Engels – drums

You can hear the whole live concert – HERE.

The songs in order on the album with times:

00:00 Stella By Starlight

10:50 For Minors Only

18:31 Almost Blue

26:26 Portrait In Black And White

42:13 My Funny Valentine

55:26 Four

01:02:56 Arborway

01:16:57 I’m A Fool To Want You

01:28:22 Seven Steps To Heaven

01:36:19 For All We Know

01:45:17 Broken Wing

That is enough for today!

(c) Copyright 2022 William Mitchell. All Rights Reserved.

Dear Bill,

Now that you are in Japan, if you want to take a break from chess, you should try Go. It is a fascinating game whose principles are very simple to learn but at least as difficult as chess to master. You are sure to find devotees among the people you meet in Kyoto.

“I was interested to trace the origin of the idea.”

The ‘trickle down’ term is a pejorative. It’s the equivalent of the ‘printing money’ slur that is targeted at MMT, and is dismissed by the other side in the same way we dismiss people who accuse MMT of ‘printing money’.

Sowell makes the case in his book

https://www.aei.org/carpe-diem/thomas-sowell-on-the-trickle-down-myth-workers-are-always-paid-first-and-then-profits-flow-upward-later-if-at-all/

There are enough holes in the ‘monetary policy controls aggregate demand, tax policy and slashing regulations will nudge people into investment rather than consumption’ argument to hit it where it hurts.

Already the supply siders are confused. Ryan Bourne (Chair in Public Understanding of Economics (!) at the Cato Institute) said today:

Yet an MMT view explains it all perfectly simply. There is no One Interest Rate to Rule Them All. That’s a Tolkienesque fictional fantasy, not a guide to public policy.

re: “There is no One Interest Rate to Rule Them All.”

Right. Interest is the price of credit. The price of money is the reciprocal of the price level. The money stock can never be properly managed by any attempt to control the cost of credit.

We should have learned the falsity of that assumption in the Dec. 1941-Mar. 1951 period. That was what the Treas. – Fed. Res. Accord of Mar. 1951 was all about.

On retail sales growth – is there a reliable measure that shows changes in total volumes of goods and services turnover rather than just changes in the level of spending? Otherwise, how do we know that people are not demanding more of everything but are simply being forced to pay more in an environment where inflation in the most fundamental of factors (energy) flows through to everything else?

I prefer the term “Horse and sparrow theory” over “trickle down”.

The horse eating all the oats and leaving the multitude of sparrows sifting through shit to find in it enough to survive truly depicts the actual workings of the neoclassical economic paradime.

Trickle down economics is in fact “a thing”… when you realize the idle rich, the exploiters and rentiers are the scum of the Earth. Money does indeed trickle down to their base level of social depravity.

As for Thomas Sowell – he always strikes me as a weasel. He uses Warren Mosler’s argument that cutting corporate taxes is good for consumers, lowering costs. Which almost all MMT’ers agree with. The way to penalize polluting or cheating or exploiting companies is to fine them out of existence, taxing them legitimizes them.

But Sowell is disgustingly disingenuous, because in popular culture “trickle down” does in fact widely get used to mean the rich are the wealth creators. It is what the average Normie is thinking when voting for a libertarian conservative who claims they want to lower the tax burden for the wealth creators. It is not a straw man. MMT cannnot agree with this, because workers are the only true creators of real goods and services, real wealth.