Yesterday (April 24, 2024), the Australian Bureau of Statistics (ABS) released the latest - Consumer…

IMF continue to demonstrate their neoliberal biases

The IMF published a new blog the other day (November 21, 2022) – How Fiscal Restraint Can Help Fight Inflation – which demonstrates that the organisation is still stuck in a New Keynesian world and despite all the empirical dissonance that has been building over the last decades to militate against that economic approach, little evolution in thinking is apparent. The battle to dispense with the mainstream approach is going to be harder and longer than many thought.

Background

The IMF base their analysis on a – Dynamic stochastic general equilibrium – model, which is the main quantitative framework for analysing policy options.

Central banks and other forecasting agencies deploy to make statements about the effectiveness of fiscal and monetary policy.

The framework is totally unsuited for the task at hand, but, embodies the ideological biases of the mainstream approach, which is why it persists.

I considered this type of model in several blog posts, including:

1. Mainstream macroeconomic fads – just a waste of time (September 18, 2009).

2. The myth of rational expectations (July 21, 2010).

3. Fiscal austerity damages real growth and prolongs the financial downturn (June 21, 2012).

4. Mainstream macroeconomics in a state of ‘intellectual regress’ (January 3, 2017).

5. Austerity is the problem for Britain not Brexit (January 9, 2017).

6. The divide between mainstream macro and MMT is irreconcilable – Part 1 (September 10, 2018).

7. The divide between mainstream macro and MMT is irreconcilable – Part 2 (September 11, 2018).

8. The divide between mainstream macro and MMT is irreconcilable – Part 3 (September 12, 2018).

These models, for example, were the basis of all the dire predictions in the aftermath of Brexit that the UK economy would collapse.

They also were the basis of a massive number of papers prior to the GFC, which indicated that financial market deregulation would deliver optimal outcomes.

The IMF used these models in their quest to convince us that there was such a thing as “growth-friendly austerity” and they informed the disastrous Greek bailouts.

So any analysis that is predicated on numbers flowing from DSGE models is bound to be defective.

As I explained in the first of the cited blog posts above, these models are not even macroeconomic in nature.

They are built on the assumption that individual optimising behaviour can be simply assumed to apply at the macroeconomic level and the only way that can be formalised in a mathematically tractable manner is to assume the so-called infinitively-lived representative agent – a single household, firm etc.

That agent is assumed to have rational expectations – which means they can predict the future with an average error of zero.

They always maximise their outcomes – now and across time (‘intertemporal optimisation’).

All markets clear – instantaneously (in some approaches) or relatively quickly (in the sticky price approaches) and involuntary unemployment is assumed away.

The models are thus totally unrealistic in construction but rely on Milton Friedman’s claim in his 1953 book ‘Essays in Positive Economics’ that it is only the predictive accuracy of models that matter not their structure.

The problem is that they are not very accurate anyway.

Their appeal to authority is that they are micro-founded in human behaviour even though not sociologist, psychologist or other social scientist that studies such behaviour would ever identify the ‘human’ that is assumed to drive economic outcomes.

The problem though is that to ‘solve’ the models for an optimal outcome, the structure has to be very simple.

That structure fails to capture the movements in the data.

To overcome that problem in empirical research the model is augmented with all sorts of additional variables which help the equation ‘fit’ the data.

But the final ‘fitting’ structure can never be derived from the micro foundations, which means that any result that is produced (policy forecast, for example) is not capable of saying anything about the underlying theoretical beginnings.

Thus, the authority is lost and we are caught in the world of ad hoc making stuff up!

GIGO.

There are many other criticisms – including that DSGE models are typically ‘real’ rather than depictions of a monetary economy that is constrained by fundamental uncertainty about the future.

In terms of monetary policy, the major way that the transmission mechanisms hypothesised in mainstream monetary theory can work is via distributional impacts – the differential interest rate impact on borrowers and creditors.

These impacts are less than understood by central bank policy makers but they assume the gains to the creditors of interest rate increases are smaller than the losses to the borrowers (mediated by different spending propensities) and so aggregate spending falls when interest rates rise.

However, in DSGE models that employ the representative agent there are no redistributive effects.

In most of these models there wasn’t even a financial sector until the GFC taught us the importance of financial sector chaos and the invalid nature of the ‘efficient markets theorem’ (which remains a core aspect of New Keynesian economics and amounts to a denial of the proposition that financial markets can be anything but optimal in outcome).

They typically have a crude loanable funds market which brings saving (positively related to interest rates) and investment (inversely related to interest rates) together via interest rate changes to ensure that spending always equals supply.

The underlying assumption is that if households stop consuming and increase saving, firms take advantage of the extra saving to increase investment and changes in interest rates mediate that change.

The problem is that saving is driven by income shifts and firms won’t investment if the economy is plunging into a recession via a drop in consumption spending.

There is no ‘automatic’ mechanism that ensures demand and supply are always equal at full employment, as is the assumption of the New Keynesian approach.

The IMF’s latest salvo

The proposition they advance is simple:

1. Central banks are hiking interest rates to combat inflation – the IMF simply assume this is an effective strategy and the DSGE models consider inflation occurs when the ‘real interest rate’ is too low (an imbalance between nominal interest rates and the inflation rate) and so increasing the nominal interest rates corrects that balance and stifles aggregate spending, which, in turn, reduces inflation.

They assume that “monetary policy has the tools to subdue inflation” even though the evidence suggests that these ‘tools’ (principally interest rate adjustments) are an ineffective way to attenuate total spending.

In fact, there is a solid body of evidence that interest rate increases are themselves inflationary especially if debt levels in the economy are high and creditors get a large income boost when rates rise, while borrowers resort to increased use of credit to maintain their spending, at least in the short-term.

Interest rate rises, after all, also add to business costs and if corporations have market power, they will push those increased costs onto consumers through price rises.

There is strong evidence that profit gouging is going on and the inflationary persistence at present is being driven by corporations taking advantage of the supply constraints to redistribute income to themselves away from workers.

2. Governments expanded fiscal policy to deal with the pandemic and this supported total spending in the economy.

That is clearly the case and without that support the global economy would have been plunged into recession.

The fact that unemployment rates are relatively low at present is the result of a combination of a contracted labour supply (lots of people who previously worked are now sick with long Covid and border restrictions) and fiscal support.

The IMF implicitly is assuming that demand is well above the supply potential of economies – that is, output gaps are positive – and the only way to redress that is to cut demand.

They thus assume that the unemployment rate is too low – relative to their benchmark stable inflation rate of unemployment (NAIRU).

Output gaps are notoriously hard to measure and the IMF measurements are always biased towards producing gaps that understate the extent of excess capacity in the economy.

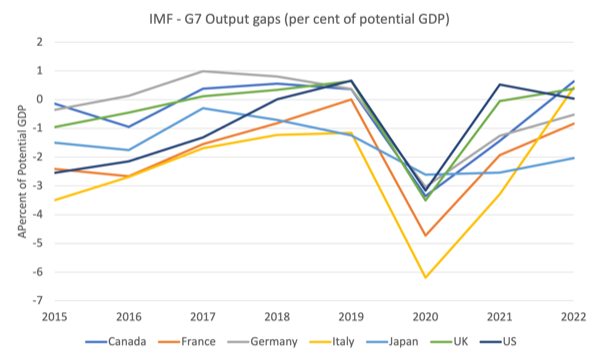

Given that bias, if we examine the latest output gap estimates from the IMF’s October World Economic Indicators – even for the G7 nations only 3 out of the 7 nations have positive gaps (another, the US is close to zero), while 3 have negative gaps, which means they are not yet at full capacity and the DSGE models should not trigger a demand-side inflationary episode.

The following graph shows the G7 output gaps since 2015 (and bear in mind they are biased toward producing positive gaps).

If you relate the knowledge of these countries to these IMF estimates you will immediately encounter anomalies, that go to the flaws in the framework.

Japan has the lowest unemployment rate yet the IMF measures its output gap to be the largest of the G7.

A cursory examination of several other nations suggests that many IMF output gaps are still negative.

In fact, the average output gaps for the following ‘blocs’ – Advanced economies, Euro area and Major advanced economies (G7) – are all still estimated to be negative.

Which means that, on their own logic, that demand pressures are not pushing the economies beyond full capacity.

Which, in turn, leads one to conclude that the current inflationary pressures are not demand-sourced.

And this policy shifts that attempt to deal with excess demand are unlikely to solve the inflationary pressures.

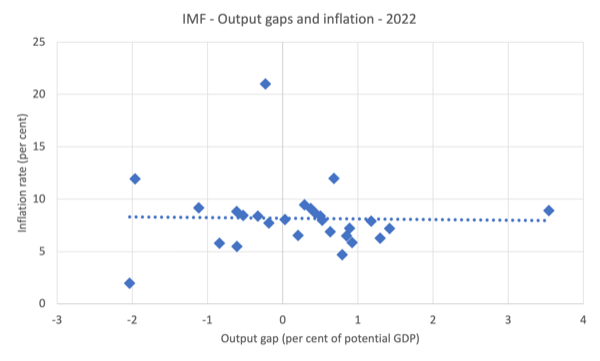

Moreover, the following graph shows the cross-plot of the estimated output gaps (horizontal axis) – that is, a synthetic data series derived from the IMF model) and the actual inflation rate (vertical axis).

The dotted line is a simple linear trend.

You will see that there is no close correspondence between the two data series. More sophisticated econometric models would also struggle using this data to find a statistically significant relationship.

That should tell you something about the veracity of the IMF approach.

3. Central banks will hike rates more than otherwise, unless fiscal policy contracts – which means reduces total spending in the economy.

This is the central tenet of the IMF argument.

That if we want less damaging interest rate hikes, then we have to have more damaging fiscal austerity.

It is a sort of blackmail argument.

4. Therefore, with some concession that fiscal support should “continue to prioritize helping the most vulnerable to cope with soaring food and energy bills and cover other costs”, the IMF recommends a bout of fiscal austerity.

They don’t articulate this specifically – but they are recommending rising unemployment to stifle aggregate spending.

They also claim that:

Moreover, with global financial conditions constraining budgets, and public debt ratios above pre-pandemic levels, reducing deficits also addresses debt vulnerabilities.

This is their real agenda.

There are no “global financial conditions constraining” fiscal policy in most nations – those that issue-their own currency.

And, the corollary of that observation is that there are no “debt vulnerabilities” in those nations.

The IMF is just repeating fictions that serve their ideological interests.

No currency-issuing government is financially constrained in their spending capacity. That is categorical.

The IMF add the usual additional fictional claims to buffer their argument:

… looming pressures on debt sustainability. These include aging populations in most advanced and several emerging economies, and the need to rebuild buffers that can be deployed in future crises or economic downturns.

1. The ageing populations are not a threat to the solvency of currency-issuing governments.

They challenge the capacity of nations to innovate and invest heavily in education and skill development of the smaller productive segment of the population.

Attempting to ‘save up’ money to deal with the higher claims on public spending by the ageing population usually involves undermining the quality of the education and training systems, which exacerbates the productivity problem.

2. There is no relevant concept of ‘fiscal buffers’ that can be applied to a currency-issuing government.

It is nonsensical to claim that these nations increase their fiscal capacity in the future by running surpluses now.

The concept of saving is inapplicable to such a government.

They issue the currency and can spend it into existence in any quantity whenever they choose, irrespective of what they spent last period.

Conclusion

At present, the overwhelming drivers of the inflationary pressures are not excessive net spending by government.

Governments should continue to support aggregate spending and low unemployment while providing targetted extra fiscal support to low-income earners who are beset with major cost-of-living pressures.

The inflationary pressures are already subsiding as the supply constraints ease and the world economy adjusts to the disruption caused by the Ukraine situation.

Add more pain to those pressures by deliberately increasing unemployment is not the sensible option.

Japan demonstrates the sensible approach.

That is enough for today!

(c) Copyright 2022 William Mitchell. All Rights Reserved.

I’ve seen a different type of GE model used to analyse the Obama package during the GFC where it was hardwired such that markets didn’t clear (or did clear well below productive capacity). The results showed that the Obama package should have been much larger. In general, GE models are as good as it gets if you are trying to analyse detailed industry and sector results. But not so good for projecting broader macro outcomes (and often input forecasts from macro experts – no not the IMF!). The key weakness of these models is the financial side of the economy, where MMT experts could genuinely make groundbreaking contributions.

“It is nonsensical to claim that these nations increase their fiscal capacity in the future by running surpluses now.”

There’s an important adjunct to this belief that time shifting is magically available. By excluding notional capital expenditure from their calculations they tend to overbid the productive economy and cause further inflation.

There is no such thing as capital and current expenditure in aggregate. All forms of spending use up labour hours in the current period of which there is a finite supply. There is a reason government used to account in cash terms rather than accrual terms. Switching to accrual terms is another neoliberal mistake that arises out of the loanable funds belief.

Accounting in accrual terms is invalid at national level. We can’t bring labour hours from the future to today.

Maybe we should look at inflation as something that didn’t happened by accident – but by design.

We’re importing inflation from the US, that has accrued this huge debt, of about 30 trillions dollars, in the government sector alone.

High inflation will slowly erase that debt, but they need to keep “printing” dollars to feed their collosal deficit, needed to sustain about 800 military bases around the world.

They are exporting the inflation abroad, but the “exports” are limited to the FIRE sector, which has its limitations.

Without goods and services to export, you have only a casino to gamble and there are other gamblers keen to learn from the masters.

If panic, somehow, settles in, inflation could turn into hyperinflation.

We’ve seen the hyperinflation movie before.

In Brasil, not so long ago.

The Brasilians changed the currency several times in the last century (before the Chicago boys got into government), to tackle high inflation.

And the US is just doing a similar move: they are already testing a digital currency, the so called CBDC (central bank digital currency), to replace old bills and coins.

With brand new features, as a complete record of what you pay, to whom, where and when.

But, really great is the expiration date.

If you don’t spend the tokens, you loose them.

Goodbye retirement, goodbye savings.

Orwellian?

Orwell couldn’ have thought of this.

This is dystopian.

@Neil Wilson I think you’re mixing up capital and revenue spending with cash/accruals accounting. But you’re right that neither distinction makes sense for a non-profit making government that can’t go bankrupt or tax dodge.

The biggest trick they pulled. Was to convince millions of voters to think they are capital when they have been Labour all along.

Read any right wing conservative website and the comment sections. Working and middle class conservatives talk as if they are capital and not workers. They achieved this trick by convincing millions of voters to believe the household budget analogy and the tax payer money myth. That is what this narrative and framing was all about.

For example:

If you raised taxes on private healthcare to release both skills and real resources for the NHS. MMT’rs know the increased taxes would occur on the targeted private healthcare companies and essentially a transfer of jobs would happen from the private to public sector. Yet, to listen to an everyday conservative voter. They believe taxes would increase on everybody and create job losses. In essence, the everyday conservative voter talks as if they are the private healthcare companies that will be affected.

Which Ultimately led to millions voting against their own interests. Refusing to accept any responsibility for their actions of voting in Conservatives for decades. Whilst unable to connect the dots of the Mankiw false framing and narratives. That was obviously created for geopolitical purposes.

How MMT’rs can help Conservative voters connect the dots for themselves. Is create a MMT city from scratch from the bottom up and explain how both skills and real resources are distributed and what choices there are when doing it. How it is funded and what are the choices to be funded.

From car park charges and hospital parking to bin collections and how councils pay for things and charge what they do for certain services. Strip the whole city to its nuts and bolts and laid bare.

I’m thinking along the lines of a book. Each chapter in the book concentrates on a different part of the MMT City. Show clearly the difference between bank lending funding and government funding and how taxes interplay and are paid regardless of which funding you choose. As your spending is someone else’s income and vice versa. Taxation quantity is a geometric series, not a simple sum. It behaves like a stone skipping across a pond. Lowering taxes just means more hops before the stone sinks. The total collected, however, will be much the same as before unless there is a material change in the amount of saving by households and businesses. Deal with the non sensical mantra “more government spending means taxes must go up”.

At the same time you could expose the central bank. The mainstream belief is that money can only be treated as static if it is exchanged for bonds paying a different interest rate. Until then all of it is permanently in motion – as though saving in a bank never happens. It’s a ridiculous notion at odds with the real world.

What we have here is the ‘loanable funds’ belief creeping in by the back door. The crazy idea that some magical interest rate will arise that will balance savings and borrowings – such that all ‘money’ things will flow in a perfectly offset manner. That doesn’t happen in the real world where money is created and destroyed constantly via the actions of the financial system. By creating a MMT city will expose this myth once and for all.

By creating a MMT city from the bottom up it will be easier for the average voter to connect the dots for themselves. A working model that comes alive as each layer/ chapter is added. Comparing it with a city built on the back of bank lending. So what the reader ends up looking at is the difference between a city created by Hayek and Mises and a city created using the MMT lens. That uses the chapters to expose the IMF , neoliberal, right wing framing and narratives for what they are. Pure propaganda for geopolitical purposes that convinced Labour they were Capital.

Derek is entirely correct when he says “The biggest trick they pulled. Was to convince millions of voters to think they are capital when they have been Labour all along.”

Here in Oz, Keating co-opted and cemented the middle classes into the neoliberal project with the introduction of an at private risk compulsory superannuation guarantee scheme on top of dividend imputation. Turning labour into share owners has been instrumental in deluding the people into seeing themselves as doing a good thing in becoming rentier capitalists. The Australian obsession with the asset price economics of real estate rental investments via negative gearing (that is restricted to relatively wealthy electors) expanded the labour as capitalists cohort to the max by the introduction of compulsory superannuation.

I suspect, through ignorance, that Keating did not fully appreciate what he was unleashing. If he can be given the benefit of the doubt, he was effectively a useful idiot and well within the neoliberal fold by that time. What a gift the ALP has been to the capitalist financialisation of the common wealth of Australia.